July 2018 – Economic and Market Update

AN ECONOMIC AND MARKET UPDATE

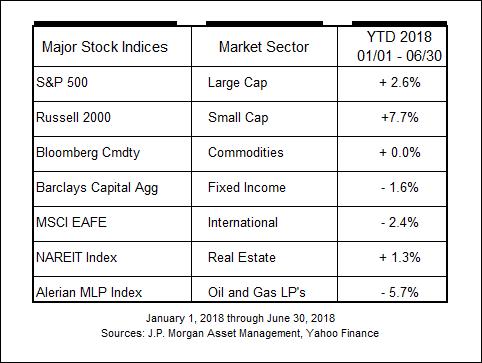

Quarterly Market Update – July 2018

EXECUTIVE SUMMARY

• An increasing interest rate environment is forcing us to remember why we invest in bonds in the first place.

• Monetary and fiscal policy are at odds with one another as higher rates mute the GDP multiplier of the Trump tax cuts.

• The Yield Curve is flattening and moving perilously close to a reliable indicator of a coming recession: an inverted yield curve.

LOOKING BACK

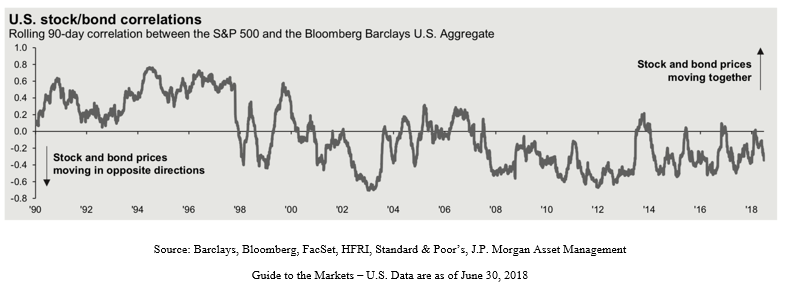

The story this year has, so far, been one of consistent pressure on fixed income securities with interest rates rising and the economy performing well. Other than that, it has been a rather unexceptional year to date throughout the various asset markets. A rising interest rate environment does not change the importance of holding bonds inside of a diverse portfolio, but it does require shifting our expectations of future bond market performance. For decades falling interest rates have pushed returns in debt instruments. It appears that paradigm has shifted for an indefinite duration.

We need to remember the other reasons why we hold bonds inside of our investment portfolios:

1. Selling into a down market to finance distributions is painful. Bonds help dampen that experience by serving as a source of distributions when markets are volatile. Bond correlations to stocks are often and currently negative, which is a good thing. This is stabilizing for portfolios in times of equity market distress as bonds zig and stocks zag. This is true regardless of the direction of interest rates as you can see below with correlations all over the board.

2. Bonds provide flexibility in re-balancing and maintaining risk allocations over time. This benefit is akin to flossing your teeth, you don’t necessarily see the benefits day-to-day but you believe the dentist (kind of) when they tell you it is best for you in the long run. Thankfully there is a wealth of information out there detailing the value rebalancing holds for risk-adjusted returns.

A FREE MARKET YOU SAY

There are two primary types of economic policies manipulating and steering the economy on an ongoing basis: these are broadly known as Monetary and Fiscal policy. We are in the midst of a tug-of-war between the two, which we will come back to after laying some basic groundwork.

Monetary Policy is the process of manipulating interest rates and the money supply to affect inflation, unemployment and moderate long-term interest rates. The Federal Reserve is at the controls and is respected for being outside of the normal sphere of partisan politics.

Fiscal Policy is guided by Congress and the President. As such, party politics have a lot of say in the type of fiscal stimulus employed. There are several methods of implementing fiscal policy: tax cuts, direct Federal spending, Federal transfers to States, Welfare Aid Transfers (Medicaid, Food Stamps, EITC), and Project Aid Transfers. Your political persuasion and world view have a lot to do with which you prefer.

The method of measuring the impact of fiscal policy is challenging. It is not as easily viewable as measuring current inflation and unemployment rates. There is a lot of noise to contend with in measuring the data. In fact, even after the results are in, economists are left with such confidence building questions as:

“How can we know whether the economy surpassed the growth it would have attained in the absence of the stimulus?”

“And even if it did, would it have grown even more with a different type of stimulus?”

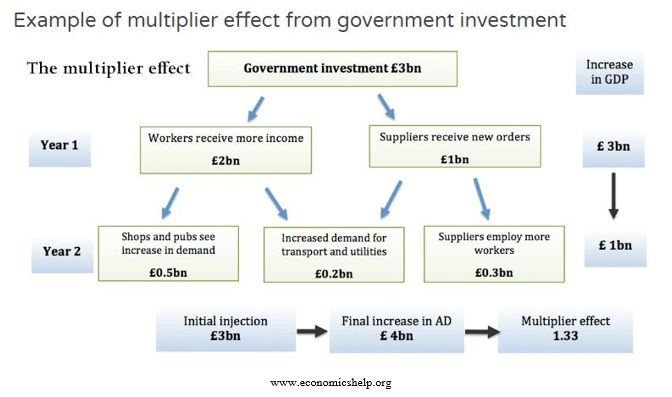

MULTIPLICATION?

Measuring the effects of fiscal policy is done primarily by looking at how things turn out and applying a multiplier to the dollars spent by the government.

Fiscal Multiplier = 1/(1-MPC) where MPC is the Marginal Propensity to Consume.

The MPC is the proportion of an additional sum of income a person, household or society will spend rather than save (Investopedia). Therefore, the higher the MPC the greater the effects from a given level of government spending. Money saved, spent in taxes or spent importing goods from foreign countries, will depress the value of the multiplier. A graphical illustration may help in understanding:

READING BETWEEN THE LINES

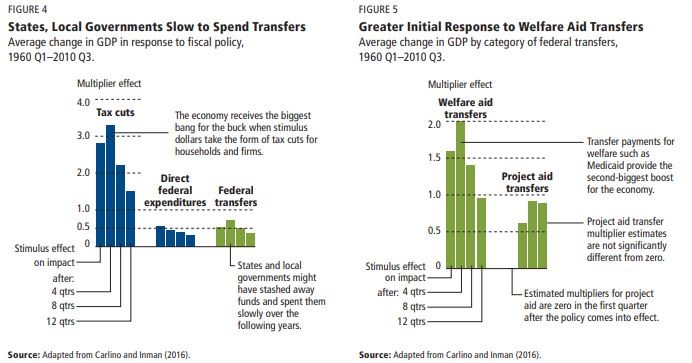

A round of fiscal stimulus enacted by President Trump and Congress in the form of tax cuts is under way, and we are coming out of a previous round of fiscal stimulus implemented under President’s Bush and Obama, the American Recovery and Reinvestment Act (ARRA). Estimates of the multiplier under the various courses of action under the ARRA program are below:

From the data, the strongest multipliers are tax cuts and welfare aid transfers. President Trump championed the most significant tax reform in a generation during his first year in office and he likely wants to see his reform continue to goose the economy. He is waging a very public battle on our current trade deficit via a trade war, money spent on imports reduces the fiscal multiplier as noted earlier by leaving the country. He also commented recently that he was not in support of the Federal Reserve raising interest rates, “I’m not thrilled. Because we go up and every time you go up they want to raise rates again. I don’t really – I am not happy about it. But at the same time I’m letting them do what they feel is best.”

Higher rates can lead to higher saving rates which reduces consumption thereby reducing the multiplier. Higher rates also increase the cost of financing which has a tendency to reduce consumption. It is no small deal for the President to comment on action taken by the Federal Reserve. The Fed is generally a non-partisan entity and one which the President does not comment on often. All of this is leading up to what we believe is a glaring issue.

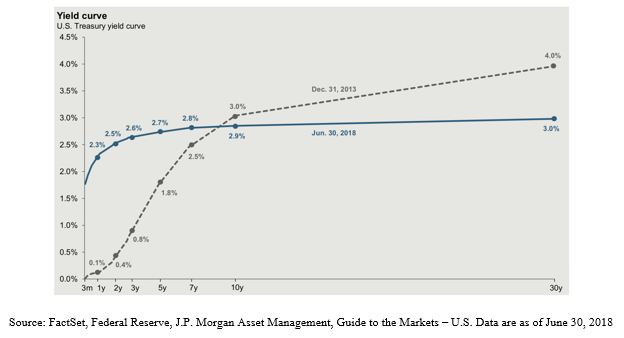

THE BIG SIGNAL

The Yield Curve is dangerously close to turning negative. This phenomenon occurs when the rates paid to hold money in the short term are higher than the rates to hold money for the long term. This is a signal of a heightened level of concern over the short-term. An inverted yield curve has been a consistently reliable indicator of a coming recession. Economists will debate whether or not this time is different and the reasons why. What we know is that fiscal stimulus eventually runs out, and when it does we will be further along in an already very long economic expansion than we are right now.

How much longer can the party last? This is our concern and question. It is also something that came up in the most recent Federal Reserve meeting held on June 13th. “In addition, the lower tax withholding resulting from the tax cuts enacted late last year still appeared likely to provide some additional impetus to spending in coming months.” If you replace “impetus” with “multiplier” the meaning of the Fed statement remains the same. The President knows he needs to protect the multiplicative effect of the stimulus he pushed so hard for. Unfortunately, he may be fighting against forces for which there is no response.

How much longer can the party last? This is our concern and question. It is also something that came up in the most recent Federal Reserve meeting held on June 13th. “In addition, the lower tax withholding resulting from the tax cuts enacted late last year still appeared likely to provide some additional impetus to spending in coming months.” If you replace “impetus” with “multiplier” the meaning of the Fed statement remains the same. The President knows he needs to protect the multiplicative effect of the stimulus he pushed so hard for. Unfortunately, he may be fighting against forces for which there is no response.

THE FEDERAL RESERVE

So on to those pesky governors of the Federal reserve. The meeting minutes from June 13th are a wealth of information. We should expect to continue to see interest rate increases, despite President Trumps disapproval. The core mandates of low unemployment and manageable inflation have been met at this time. Interest rates will rise as they move to keep those mandates stable. Continuing a path of monetary tightening gives the Fed tools to combat a recession when one materializes. What we mean is there must be room to both decrease/increase interest rates and contract/expand the balance sheet for the Fed to handle economic potholes. We could be wrong, but it is our opinion they will pursue a path of continuing to expand their ability to act. This will likely work in direct contrast to the current bout of fiscal stimulus in the Tax Cuts and Jobs Act.

One statement stood out from the meeting above the rest and relates to the small, but escalating, trade war:

“However, many District contacts expressed concern about the possible adverse effects of tariffs and other proposed trade restrictions, both domestically and abroad, on future investment activity; contacts in some Districts indicated that plans for capital spending had been scaled back or postponed as a result of uncertainty over trade policy. Contacts in the steel and aluminum industries expected higher prices as a result of the tariffs on these products but had not planned any new investments to increase capacity. Conditions in the agricultural sector reportedly improved somewhat, but contacts were concerned about the effect of potentially higher tariffs on their exports.”

The current state of the trade war is minor, but it is creating uncertainty. Uncertainty can generate ripples through the economy as businesses either delay or revise the decision making process. This has real consequences.

LOOKING FORWARD

For the time being it appears as if there is enough sugar rush from the tax cuts to push the economy forward for another year or two. Hopefully the fiscal multiplier is enough to drive GDP growth in the face of a variety of headwinds, such as increasing interest rates and a widening trade war.

The following is our list of future concerns with outstanding items from previous Economic Updates and new items added:

- Indictment of President Trump.

- Still an issue hanging around.

- Impeachment of President Trump.

- Still an issue hanging around.

- NAFTA negotiations

- President Trump is pursuing a bi-lateral approach as of early June, having split discussions from three-way with Canada and Mexico, to separate discussions with each country.

- North Korea nuclear ambitions.

- Ongoing negotiations with no tangible updates as of yet.

- Middle East instability.

- Little changed.

- Expansion of Trade War

- Discussions are happening to expand tariffs to all Chinese imports.

- The Federal Reserve building monetary capacity by raising rates and decreasing their balance sheet.

We are here to help you make rational, informed and well-reasoned decisions. We thank you for your continued trust and support. Your input is always welcome and we ask that you contact us with any questions or concerns.

- I. Jaconetti, Colleen M, et al. “Bets Practices for Portfolio Rebalancing.” Www.vanguard.com, Vanguard, July 2010, www.vanguard.com/pdf/icrpr.pdf.

- II. “Board of Governors of the Federal Reserve System.” FRB: IFDP Notes: The Effects of Demographic Change on GDP Growth in OECD Economies, Board of Governors of the Federal Reserve System (U.S.), www.federalreserve.gov/monetarypolicy.htm.

- III. Carlino, Gerald A. “Did the Fiscal Stimulus Work.” Www.philadelphiafed.org, The Federal Reserve, 2017, www.philadelphiafed.org/-/media/research-and-data/publications/economic-insights/2017/q1/eiq117_did-the-fiscal-stimulus-work.pdf?la=en.

- IV. Carlino, Gerald A. “Did the Fiscal Stimulus Work.” Www.philadelphiafed.org, The Federal Reserve, 2017, www.philadelphiafed.org/-/media/research-and-data/publications/economic-insights/2017/q1/eiq117_did-the-fiscal-stimulus-work.pdf?la=en.

- V. Staff, Investopedia. “Fiscal Multiplier.” Investopedia, Investopedia, 4 Dec. 2017, www.investopedia.com/terms/f/fiscal-multiplier.asp.

- VI. Pettinger, Tejvan. “The Multiplier Effect.” Economics Help, 2 July 2017, www.economicshelp.org/blog/1948/economics/the-multiplier-effect/.

- VII. Carlino, Gerald A. “Did the Fiscal Stimulus Work.” Www.philadelphiafed.org, The Federal Reserve, 2017, www.philadelphiafed.org/-/media/research-and-data/publications/economic-insights/2017/q1/eiq117_did-the-fiscal-stimulus-work.pdf?la=en.

- VIII. Cox, Jeff. “Trump Lays into the Fed, Says He’s ‘Not Thrilled’ about Interest Rate Hikes.” CNBC, CNBC, 20 July 2018, www.cnbc.com/2018/07/19/trump-lays-into-the-fed-says-hes-not-thrilled-about-interest-rate-.html.

- IX. Paletta, Damian. “Trump Aims to Split up NAFTA Negotiations, Deal with Canada and Mexico Separately.” The Washington Post, WP Company, 5 June 2018, www.washingtonpost.com/news/business/wp/2018/06/05/trump-aims-to-split-up-nafta-negotiations-deal-with-canada-and-mexico-separately/?utm_term=.80fdce0e570f.