July 2020 – An Economic and Market Update

Executive Summary

- Markets have rebounded significantly though there remains a great deal of uncertainty in the economic environment.

- Recovery expectations are tempered as reopening policies are being paused and reversed by a number of state and local governments.

- The good, the bad, and the Fed as it pertains to current economic conditions.

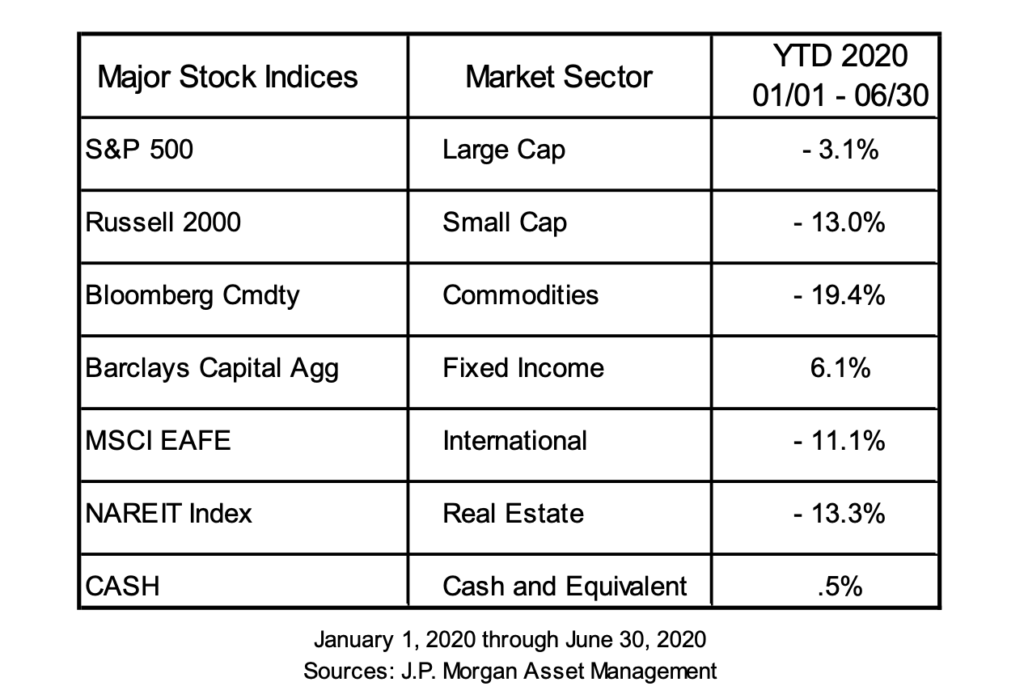

Looking Back

The markets have rebounded from the bottom in March with many of the early losses being recovered. As you would expect in a downturn, the best performing asset class year-to-date has been core bonds (investment grade corporate debt and government debt). The ongoing debate of whether the recovery will be a V (most desirable), a W (least desirable), or something in between is irrelevant so far as performance has been concerned. Stock prices suggest a V-shaped recovery is underway if we believe that prices are forward looking. Comments made in the last FOMC (Federal Open Market Committee) meeting in June remind us that we should be prepared for a W-shaped recovery. It was noted that a more “pessimistic projection was no less plausible than the baseline forecast”. Meaning, of all the projections made for the economic trajectory out of the virus-induced recession, the likelihood of a strong recovery is equally matched by the possibility of a very painful one.

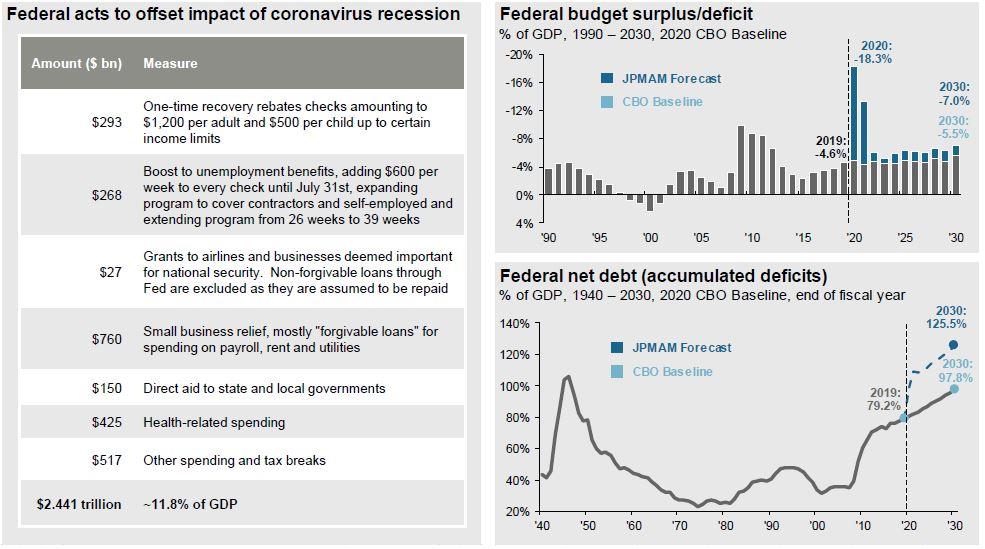

A significant part of the rebound has been the extensive fiscal and monetary stimulus which the Federal Government and the Federal Reserve have enacted. Fiscal stimulus measures enacted-to-date are listed below. Congress is currently debating additional spending as most of the programs are soon coming to an end, such as the additional $600/week Federal Unemployment Assistance.

The recovery will come at a cost in the form of looming budget deficits and massive increases to Federal Net Debt as illustrated above. The solution to our current crisis may be to throw money at the problem. However, the solution(s) to the problem(s) created by massive debt expansions are unlikely to be quite so simple and are unlikely to be felt until we all forget how we got there in the first place. A recent Brookings institution article by David Wessel illustrates the problem we have with debt saying, “No one really knows at what level a government’s debt begins to hurt an economy; there’s a heated debate among economists on that question”. Someday that debate will get settled.

The Consumer

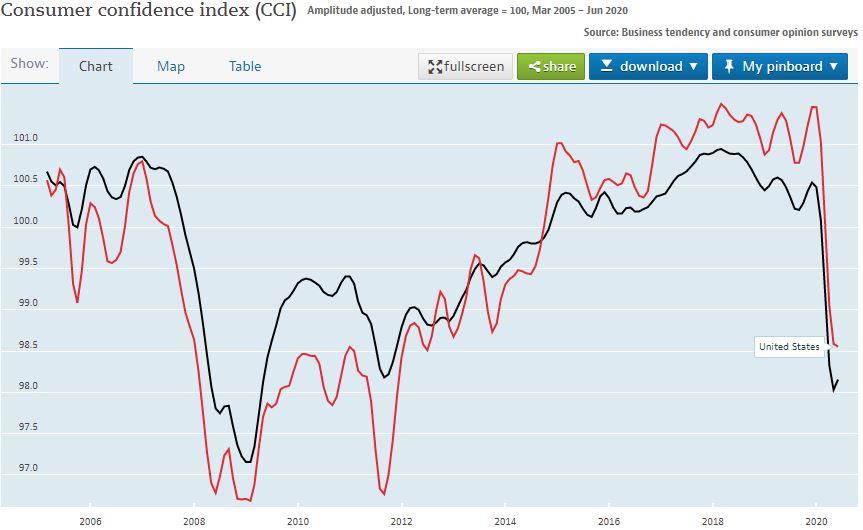

In our last update we discussed the power of the U.S. consumer in moving the needle on economic revival. As expected, consumer confidence took a significant hit since the March measurements. It appears we have turned a corner as evidenced by the slight uptick in the OECD countries (the black line) and the slow-down in negative trajectory in the U.S. (the red line) – that is the good news.

Whether or not this shift in expectations continues is likely tied to the virus trajectory (which has gotten far worse as of late) and whether states and other countries begin to lockdown again (which they have). As of July 14th, twenty-two states have either paused or reversed reopening the economy according to the New York Times. Anecdotal evidence in the form of aborted travel attempts by members of Reason Financial support this reality. Some of the largest state economies in the country are a part of the reversed reopening group including California, Texas, and Florida. This is not reflected in the Consumer Confidence Index since the data is as of June and the reversals began occurring either after the data was compiled or towards the tail end of the period covered. It is not unrealistic for us to assume we will see a downward trend once again – that is the bad news.

The Federal Reserve and Economic Projections

To shed more light on the FOMC comment regarding a “pessimistic projection” being no less plausible than the baseline forecast we should put the comment into time, June 10, 2020, and in broader context:

“In light of the significant uncertainty and downside risks associated with the pandemic, including how much the economy would weaken and how long it would take to recover, the staff judged that a more pessimistic projection was no less plausible than the baseline forecast. In this scenario, a second wave of the coronavirus outbreak, with another round of strict limitations on social interactions and business operations, was assumed to begin later this year, leading to a decrease in real GDP, a jump in the unemployment rate, and renewed downward pressure on inflation next year. Compared with the baseline, the disruption to economic activity was more severe and protracted in this scenario, with real GDP and inflation lower and the unemployment rate higher by the end of the medium-term projection.”

Several weeks before paused and reversed reopenings began to happen, the Fed stated that there was a similar likelihood of a strong recovery vs. a protracted recovery due to the possibility of a second virus wave bringing additional shutdowns. Their prognostications have come to pass.

Source: NY Times, data as of July 25, 2020

The second wave is here and it brings with it a risk that the positive strides made towards economic recovery may begin to unwind a bit. As the data above indicates we are currently in the middle of a virus peak worse than when the lockdowns began.

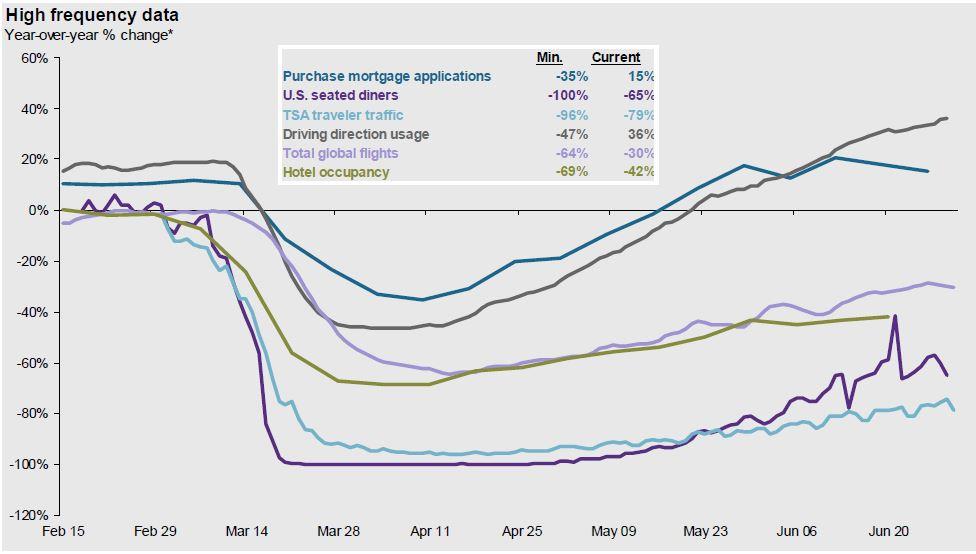

Improvement from the bottom of the March and April shutdowns in a variety of metrics can be seen in the following graph.

Guide to the Markets – U.S. Data are as of June 30, 2020

Steady improvement in flights, hotels and dining have been made. Dramatic improvement in mortgage applications and driving direction usage (a measure of people leaving their homes and traveling) have also occurred. All of this is directly related to the consumer having the confidence to get out and engage in life to some degree or another. The second wave of the virus puts these improvements at risk. Federal Reserve Chair Jerome Powell addressed this in a recent speech, “We all want to get back to normal, but a full recovery is unlikely to occur until people are confident that it is safe to reengage in a broad range of activities”. Confidence is a powerful motivator.

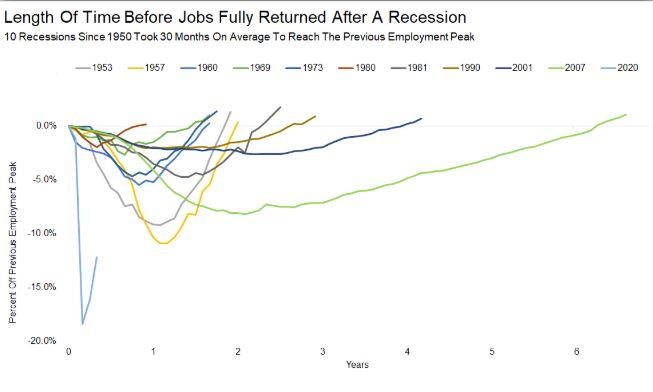

Extrapolating this activity out to the job market makes apparent that there are a lot of jobs which will not be coming back anytime soon. Calculating the length of time necessary to get everyone back to work who were laid off in a downturn is tricky business. Businesses slim down and get more efficient during crises and take time to get back to the point where they are running at full capacity again.

The last recession started in 2007 and took more than 6 years to replace all of the jobs lost. Granted, the foundation of the economy prior to the financial crisis was in shambles. We did not know we were built on shaky ground until it was too late. Economically speaking we were in a good place pre-COVID. We should expect to return to full-employment faster than 6 years, but it is still going to take time to get there. This is a recession like no other and it certainly appears as if service related jobs, particularly in the dining, entertainment, and travel sectors, will take the longest time to fully recover. The renewed closures of state and local economies is making this a reality.

To tie this all together: the consumer is necessary to drive demand which drives employment which pushes the economic engine forward. We artificially stopped demand from occurring with shutdowns and then began the process of slowly bringing demand back online with reopenings. The resurgence of the virus will likely cause an additional decrease in demand as reopenings are paused or reversed, lengthening the time of recovery and keeping people out of work longer than originally hoped for.

Closing Thoughts

The potential for renewed volatilty and a protracted recovery scenario are at the top of our minds. Our focus is on discerning the best path forward and we continue to carefully monitor the actions necessary to preserve the wealth and financial well-being of all our clients. Wealth is often built through concentration, such as in the building of a business or reinvesting in the stock of the company you work for. However, once wealth is built it is best preserved through diversification and spreading risk as broadly as possible. This belief is a guiding principle of Reason Financial.

From a planning perspective, now is a great time to look at a refinance of your mortgage debt, particularly if you are underneath the Fannie Mae conforming limit of $510,000 and are not attempting a cash-out refinance. It is very possible to obtain a sub-3% 30-year fixed-rate loan, particularly if you have good credit. If you are in a high-balance situation, the rates are in the low to mid 3% range with good credit. As evidenced earlier, mortgage application activity has rebounded in a powerful way, driven mostly by the incredibly low rates in the current market environment.

As always, our desire is to help you make rational, informed and well-reasoned decisions, and we thank you for your continued trust and support. Your input is always welcome, and we ask that you contact us with any questions or concerns.

1 Wessel, David. “How Worried Should You Be about the Federal Deficit and Debt?” Brookings, Brookings, 9 July 2020, www.brookings.edu/policy2020/votervital/how-worried-should-you-be-about-the-federal-deficit-and-debt/.

2 Lee, Jasmine C., et al. “See How All 50 States Are Reopening (and Closing Again).” The New York Times, The New York Times, 25 Apr. 2020, www.nytimes.com/interactive/2020/us/states-reopen-map-coronavirus.html.