1st Quarter 2026 – Economic and Market Update

AN ECONOMIC AND MARKET UPDATE

February 2026

EXECUTIVE SUMMARY

- 2025 ended a third straight of positive domestic equity returns.

- Introducing our Chief Investment Officer Brian Andrew.

- Trump Accounts are around the corner. Check out https://trumpaccounts.gov/ for how to make an election to open an account.

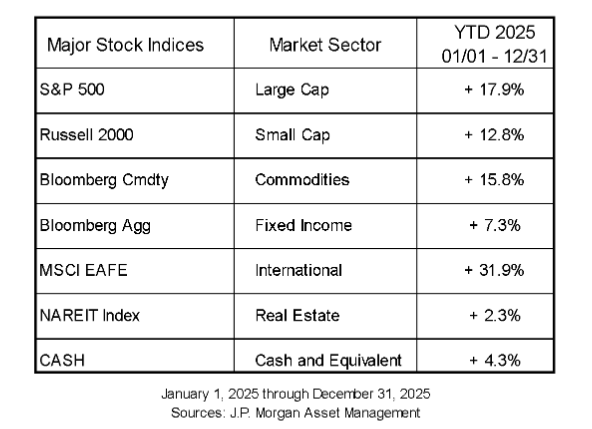

This was a year where the various moving parts all came together better than expected. Federal Reserve interest rate policy, tariffs, geopolitical tensions, and the new administration combined to provide an exciting and profitable year on the stock market. The best performing asset class was international. The last time this happened was in 2017. Domestic equities held their own and continued an impressive run since 2023. The sell-off caused by the tariff rollout was shortlived as markets digested the mechanical application of tariff policy beyond the original announcement by President Trump on “Liberation Day”. Commodities posted an impressive run, led primarily by gold and silver, although their run has hit a rough patch in the new year.

Aside from implementation of the OBBBA (One Big Beautiful Bill Act) this tax season, the eventual successor to Fed Chair Jerome Powell, whose term ends in May 2026, is the most exciting scheduled event of the next few months. The administration has nominated Kevin Warsh as the next successor. Mr. Warsh is a well-known commodity having served as a Federal Reserve Governor during the Bush and Obama administrations.

INTRODUCTION TO BRIAN ANDREW, CHIEF INVESTMENT OFFICER

This year we will be focused on putting out more, and more timely, content. In order to do so we are beginning to leverage other individuals within our RIA (Registered Investment Advisor) firm, Merit Financial Advisors.

Our Chief Investment Officer, Brian Andrew, formerly the EVP of Johnson Financial Group, is responsible for overseeing and managing the investment department and asset allocation decision-making process for us. As such, his insights into the market and the economy are the most relevant observations we can provide as they relate to how we manage client assets through market cycles.

Our Q1 market update, provided by Mr. Andrew, is available along with a market update video at the following link: https://meritfinancialadvisors.com/blog/2026-market-outlook/

TRUMP ACCOUNTS

Trump Accounts are about 5 months out from being a reality according to current guidance from the administration. However, the first significant wave of information is here regarding how to start the process. For those who are not yet aware, Trump Accounts (Jumpstarting the American Dream accounts) are tax-advantaged savings and investment accounts for children under the age of 18. While you cannot yet open and fund one, we do know what the first step in the process is, making an election on IRS Form 4547.

If you are considering opening one of these accounts for your children or grandchildren, the first place to go is https://trumpaccounts.gov/

As of right now, the link above is the only location we know where you can file the necessary IRS form to make the election. Guidance is still pending on the integration of the tax form into the various tax preparation software solutions. If you file your tax return early and are planning on opening a Trump Account, you will need to separately file the necessary form.

Should you open one for your children/granchildren? It is hard to find a reason you would not. In an interview with David Rubenstein in 2016, Warren Buffett stated “my life has been a product of compound interest”. The earlier you start compounding the better off you will be in the long run. If properly executed, these accounts could serve as the future backbone of retirement savings for the current crop of youngsters.

One of the hardest mental hurdles to overcome in saving is seeing that it is worth it in the long term, put differently, avoiding the danger of present bias. It is hard to envision the first $1,000 you save becoming anything significant over time. When the need for immediate gratification rears its head in the form of consumption such as travel, or in my case fancy rims for my car when I was 18, it is hard to see the benefit of investing $1,000. Theoretically this hurdle could be overcome by starting savings at birth and allowing time to do the heavy lifting by the time a baby becomes an adult. Falling prey to short-termism could be mitigated as the value of compounding will be self-evident.

We already do this with College Savings 529 Plans. Why not allow retirement planning to start at birth as well?

To make it better, the government along with a variety of private individuals and institutions have pledged to assist in seeding the accounts.

The tentative date accounts go live for opening and funding is July 4, 2026. Maybe President Trump is targeting the 4th of July so he can link financial independence via his namesake savings account to the 250th birthday of our country on Independence Day. He does seem to have a flair for the dramatic, such as calling the announcement of huge tariffs “Liberation Day’. Time will tell. In the meantime, keep an eye on updates to this program. Widespread adoption of these accounts is potentially a game changer for the future of retirement and Social Security.

Our commitment to guiding you through these evolving economic conditions remains unwavering. We encourage you to reach out with any questions or concerns as we continue to move forward in an uncertain world.

DISCLOSURE

This material is for general information only and is not intended to provide specific advice or recommendations for any individual. There is no assurance the views or strategies discussed are suitable for all investors or will yield positive outcomes. Investing involves risks including possible loss of principal. Any company names noted herein are for educational purposes only.

All information is believed to be from reliable sources; however we make no representation as to its completeness or accuracy. All economic and performance data is historical and not indicative of future results. Market indices discussed are unmanaged. Investors cannot invest in unmanaged indices. Additional risks are associated with international investing, such as currency fluctuations, political and economic instability and differences in accounting standards.

Investing in securities in emerging markets involves special risks due to specific factors such as increased volatility, currency fluctuations and differences in auditing and other financial standards. Securities in emerging markets are volatile and can decline significantly in response to adverse issuer, political, regulatory, market, or economic developments.

An index is a statistical measure of change in an economy or a securities market. In the case of financial markets, an index is an imaginary portfolio of securities representing a particular market or a portion of it. Each index has its own calculation methodology and is usually expressed in terms of a change from a base value. Thus, the percentage change is more important than the actual numeric value. An investment cannot be made directly into an index.

Investing in fixed income securities involves credit and interest rate risk. When interest rates rise, bond prices generally fall. Investing in commodities may involve greater volatility and is not suitable for all investors. Investing in a non-diversified fund that concentrates holdings into fewer securities or industries involves greater risk than investing in a more diversified fund. The equity securities of small companies may not be traded as often as equity securities of large companies so they may be difficult or impossible to sell. Neither diversification nor asset allocation assure a profit or protect against a loss in declining markets. Past performance is not an indicator of future results.

Financial Planning offered through Reason Financial, a state Registered Investment Advisor. Investment advice offered through Merit Financial Group, LLC an SEC Registered Investment Advisor. Merit Financial Group and Reason Financial are separate entities. Tax related services offered through Reason Tax Group. Reason Tax Group is a separate legal entity and not affiliated with Merit Financial Group, LLC. Sean P. Storck CA Insurance Lic#OF25995 and Steven W. Pollock CA Insurance Lic#OE98073

Copyright © 2026 Reason Financial all rights reserved.

[i] “FOMC Press Conference, October 29, 2025.” Federal Reserve, YouTube, www.youtube.com/watch?v=gZsAKn1UtH4. Accessed 30 Oct. 2025.

[ii] “How Bonds Affect Mortgage Rates: Chase.” Credit Card, Mortgage, Banking, Auto, www.chase.com/personal/mortgage/education/financing-a-home/how-bonds-affect-mortgage-rates. Accessed 30 Oct. 2025.

[iii] “Business Development Company.” Wikipedia, Wikimedia Foundation, 29 Sept. 2025, en.wikipedia.org/wiki/Business_Development_Company.

[iv] Edwards, Jim. “Jamie Dimon Issues Private Credit Warning: ‘When You See One Cockroach, There Are Probably More.’” Fortune, Fortune, 15 Oct. 2025, fortune.com/2025/10/15/jamie-dimon-issues-private-credit-warning-when-you-see-one-cockroach-there-are-probably-more/.

[v] “Trump Accounts Give the next Generation a Jump Start on Saving.” The White House, The United States Government, 29 Aug. 2025, www.whitehouse.gov/research/2025/08/trump-accounts-give-the-next-generation-a-jump-start-on-saving/.

[vi] “What Are Trump Accounts?” Savings for Newborns, www.axosbank.com/personal/insights/finance/financial-planning/what-are-trump-accounts. Accessed 30 Oct. 2025.

[vii] https://www.dinkytown.net/java/future-value-calculator.html