3rd Quarter 2025 – Economic and Market Update

AN ECONOMIC AND MARKET UPDATE

July 2025

EXECUTIVE SUMMARY

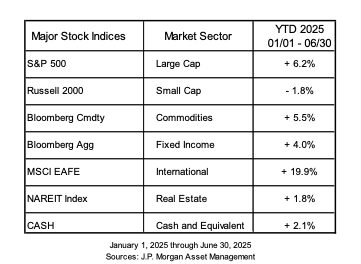

- It is an up year almost all the way around, with nearly all major indices in positive territory.

- Tariffs and talk of replacing Fed Chair Powell have driven volatility without any major negative consequences, yet.

- The One Big Beautiful Bill Act (OBBBA) is here, and there are lots of winners.

The year has been quite volatile. In the 2nd Quarter, markets shrugged off the impact of tariffs and recovered from what had been a very broad and dramatic sell-off during the 1st Quarter. During that time other quick drops have occurred, usually stemming from headlines related to the state of tariff negotiations, talk of firing Federal Reserve Chair Jerome Powell, or bombs being dropped to stop nuclear programs. Despite continued geopolitical tensions, international markets, both developed and emerging, have been the best performers. All other major asset classes are in positive territory with the exception of U.S. small cap stocks. Growth has continued to push forward in the U.S., somewhat unexpectedly, with a recent headline by the Financial Times titled, “How Long Can the U.S. Economy Defy Expectations?”.[i]

If you are looking for a canary in the coal mine, it does not appear to be there. Negative takes are out there, but the economy just keeps clicking along.

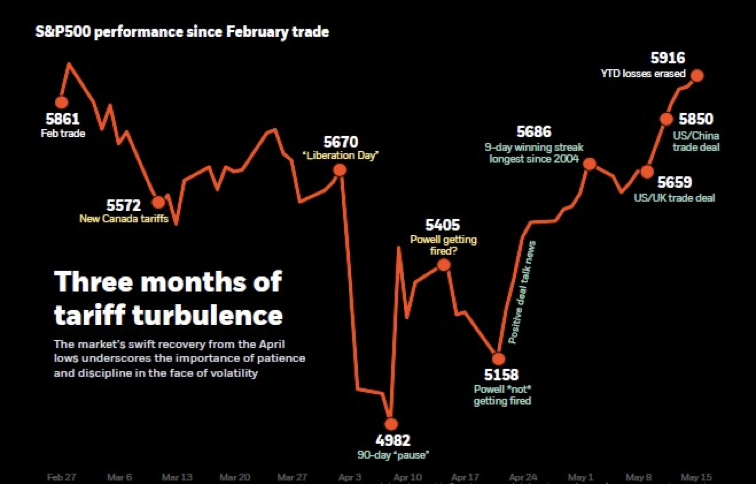

VOLATILITY

The markets have been all over the place this year as you can see below. The big drops were caused more by headlines creating uncertainty than anything else. “Liberation Day” was the first big hammer. As of yet, there have been no major negatives to report. The U.S. has secured new trade deals, or the substantial framework of new trade deals, with the European Union, UK, and Japan to name a few. We are currently in another extension of a truce with China while a trade deal is worked out. Deals with two significant partners remain out of reach, Canada and Mexico.[ii]

Sources: Blackrock, Bloomberg, as of 05/15/2025. MPS trade in February was 02/27/2025. S&P 500 total return index. Index performance is for illustrative purposes only. Index performance does not reflect any manageement fees, transaction costs or expenses. Indexes are unmanaged and one cannot invest directly in an index. Past performance does not guarantee future results.

There have been no major impacts to inflation as initially forecast. However, tariffs have not been fully absorbed into the system. It is quite possible that sellers of goods impacted by tariffs have just eaten the cost to not land on the wrong side of where policy will ultimately settle. In other words, we still have a moving target, but nothing major to report yet.[iii]

The other major mover on the year is the ongoing debate as to whether Fed Chair Jerome Powell will be kept through the end of his term, May 2026. President Trump made the words, “You’re fired”, famous with his television show “The Apprentice”. His failure to terminate Chair Powell, despite many statements indicating that is his preference, suggests he either is doing his very best to intimidate Mr. Powell but does not want to fire him, or he has no legal path to do so.[iv]

Source: made using Grok

Prominent economist, and current president of Queen’s College, Cambridge, Mohamed El-Erian recently called for the Federal Reserve Chair to step down. Not for malfeasance or ineptitude however, but as a way to preserve Federal Reserve independence in the wake of significant verbal attacks by the Trump Administration. The Federal Reserve is in a bad spot. The market response to the potential firing of Chair Powell had a lot to do with concern over the independence of the institution. It is tasked with two important jobs which it manages in a non-partisan way, full employment and stable inflation. The Federal Reserve becoming a tool of the Executive Branch is a scary possibility, and the markets reacted accordingly. Any move by the Fed with Jerome Powell at the helm is going to be viewed as potentially triggered because of or at the behest of President Trump. Do they do nothing? Maybe that is them digging in and saying they cannot be cowed by the President, even if cutting rates makes sense. If they cut rates, is it because the President said so, or because it was the best thing for the economy?[v]

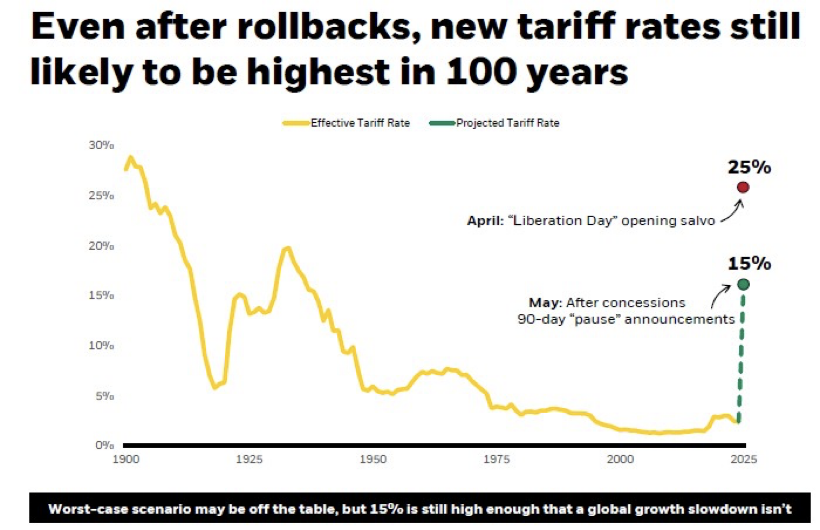

Source: Blackrock, Bloomberg, State of U.S. Tariffs, Yale University, as of 05/12/2025

At this point it looks like the two major volatility drivers for the year are working themselves out. Chairman Powell is running out of time in his tenure, and trade deals are being made. An important note regarding tariffs, the level at which tariffs finally land will be higher than they were before as you can see above. In June the effective tariff rate was 14.1% versus 2.3% in the prior year. It feels like concrete information on tariff policy is hard to suss out with all of the back and forth. Tariffs will land higher than they were in the past, significantly. You have to go back 100 years to see rates as high as what we are experiencing now, and will be moving forward. The long term impact of this increase is working its way in.[vi]

THE OBBBA (One Big Beautiful Bill Act) or OBBB (Omnibus Budget and Benefits Bill)

We really were hoping for a better name, one that did not make us start humming ABBA tunes, but alas Dancing Queen is the ear worm of the moment. Much of the OBBBA (One Big Beautiful Bill Act) was making permanent the rules from the TCJA (Tax Cuts and Jobs Act of 2017). Like it, love it, or whatever you feel about it, business likes certainty and we now know what the tax landscape will look like for quite some time. There are some temporary provisions, such as the extra $6,000 deduction for seniors, but, on the whole, where we have been is where we will continue to be. This is good for business as certainty in tax law creates a means by which to develop forward-looking strategies.

The big winners are businesses large and small. The 100% bonus depreciation deduction is here to stay. The Tax Foundation estimates that this provision will “raise GDP in the long run by 0.6 percent and increase the stock of capital by 1 percent.” The Qualified Business Income Deduction is also now permanent with all of the same phaseouts for service based businesses. These are all pro-business and pro-growth.[vii]

On the individual side the deductions for seniors, tips, overtime, and auto loan interest are a win for the average Jane. We have had a lot of questions come up regarding how these new deductions will help. To be honest, we are not sure yet. The senior deduction is easy to calculate as it is a direct add-on to the standard deduction. For other newcomers to the tax code, we will need to see how everything works out. There will be new forms. President Trump promised in his first term to simplify filing taxes. In some respects he did, fewer people itemize now than before. Technically, this is a simplification, but all the new deductions sure seem like a complication to us.[viii]

A very big boon for coastal high property value states is the increase to the SALT limitations, State and Local Tax. Under the TCJA this was capped at $10,000. It is now $40,000. However, this is only a temporary fix. We will be debating the SALT limitation in 2030 if there is no further legislation to solve this conundrum. The increase to the SALT deduction phases out for incomes over $500,000, my apologies to the top 5% of earners in the country.[ix]

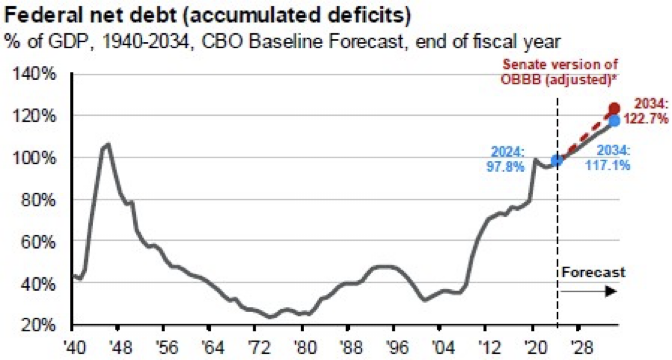

The OBBBA is currently forecast to increase the Federal debt $4.2 trillion by 2034. These forecasts are created in a vacuum so how it will play out in real time is something only time will tell. However, the debt issue which was talked about so much at the start of the year does not appear to be as big of a priority for the administration when taxes are the current talking point.[x]

Source: J.P. Morgan Asset Management, BEA, Treasury Department. Estimates are from the Congressional Budget Office (CBO) January 2025 An Update to the Budget Outlook: 2025 to 2035. Guide to the Markets – U.S. Data are as of June 30, 2025

Debt aside, this tax policy is growth oriented. Businesses get deductions and individuals get deductions. This policy will act as a significant fiscal stimulus driver of growth. Most people will pay less in taxes, and, likely, spend more on consumption stimulating the economy. If only we knew how it is going to be paid for.

BACK TO THE CANARY

As tax and tariff policy has worked itself out there are fewer significant areas of concern in the economy. However, we are looking forward to a variety of data points to inform our forward looking investment strategy. The Federal Reserve meeting is coming up at the end of July. This will give us additional insight into the future of interest rate policy. We are not anticipating a change at this time, but it will be interesting to see how Powell handles the forward guidance portion of his press release.

GDP estimates will be released giving us additional insight into the impacts of tariffs on the economic situation. Additionally, updated numbers on inflation will be an important data point addressing the same topic.

The housing market does not appear to be moving in the right direction. Existing home sales have fallen, as have building permits. Relatively high interest rates coupled with high entry prices are likely the culprit here.[xi]

Data on the current state of the labor market will also be released highlighting the health of the economy in continuing to provide opportunities for current participants, and new participants.

A raft of data is forthcoming as we continue to digest the impact of tariffs, but by and large everything looks fine for the most part.

THE FINANCIAL PLANNING CORNER

Long term care is not a topic many people like to talk about. It is, however, a topic that will come up at some point in our lives. The vast majority of us will need to address how to care for an aging parent, family member, or spouse. In 2019, the Dept. of Health and Human Services released a study showing, “that 70 percent of adults who survive to age 65 develop severe LTSS (Long Term Support Service) needs before they die and 48 percent receive some paid LTSS over their lifetime.”[xii]

These statistics are jarring. Morbidity and mortality are not fun topics to discuss, but the conversations around these matters are necessary. A major source of uncertainty in the longevity of retirement funds are future medical costs, with many people citing long-term dementia as a nightmare scenario. A great time to begin planning for how you are going to address future needs is in your 50’s and 60’s when there is still, usually, ample time to prepare for such an outcome.

There are great options out there for contingency planning, the key point is to get the conversation started. It is a lot easier to handle trying circumstances when you have already had a conversation about how you will respond if scenario A, B, or C occurs.

Our goal is to generate positive discussions around a hard topic. We can also easily run illustrations on various long term care insurance solutions to assist in informing the conversation with solid data versus speculation. Don’t wait to have the conversation until you are considering selling a home or taking out a reverse mortgage as the only options. This is a situation we have seen play out in the past, and it is always a hard discussion to have.

Home healthcare is a very expensive option, but it is also the one we hear people cite as their preferred delivery system. If the default response to the question “how will we handle long term care?” is, “I want to stay at home”, then exploring a long term care insurance solution should be top of mind. Home healthcare is an expensive and complicated situation when the issue of household employees is brought into the fold. We would not recommend trying to go this route without exploring how to offset some of the costs.

Our commitment to guiding you through these evolving economic conditions remains unwavering. We encourage you to reach out with any questions or concerns as we continue to move forward in an uncertain world.

DISCLOSURE

This material is for general information only and is not intended to provide specific advice or recommendations for any individual. There is no assurance the views or strategies discussed are suitable for all investors or will yield positive outcomes. Investing involves risks including possible loss of principal. Any company names noted herein are for educational purposes only.

All information is believed to be from reliable sources; however we make no representation as to its completeness or accuracy. All economic and performance data is historical and not indicative of future results. Market indices discussed are unmanaged. Investors cannot invest in unmanaged indices. Additional risks are associated with international investing, such as currency fluctuations, political and economic instability and differences in accounting standards.

Investing in securities in emerging markets involves special risks due to specific factors such as increased volatility, currency fluctuations and differences in auditing and other financial standards. Securities in emerging markets are volatile and can decline significantly in response to adverse issuer, political, regulatory, market, or economic developments.

An index is a statistical measure of change in an economy or a securities market. In the case of financial markets, an index is an imaginary portfolio of securities representing a particular market or a portion of it. Each index has its own calculation methodology and is usually expressed in terms of a change from a base value. Thus, the percentage change is more important than the actual numeric value. An investment cannot be made directly into an index.

Investing in fixed income securities involves credit and interest rate risk. When interest rates rise, bond prices generally fall. Investing in commodities may involve greater volatility and is not suitable for all investors. Investing in a non-diversified fund that concentrates holdings into fewer securities or industries involves greater risk than investing in a more diversified fund. The equity securities of small companies may not be traded as often as equity securities of large companies so they may be difficult or impossible to sell. Neither diversification nor asset allocation assure a profit or protect against a loss in declining markets. Past performance is not an indicator of future results.

Financial Planning offered through Reason Financial, a state Registered Investment Advisor. Investment advice offered through Merit Financial Group, LLC an SEC Registered Investment Advisor. Merit Financial Group and Reason Financial are separate entities. Tax related services offered through Reason Tax Group. Reason Tax Group is a separate legal entity and not affiliated with Merit Financial Group, LLC. Sean P. Storck CA Insurance Lic#OF25995 and Steven W. Pollock CA Insurance Lic#OE98073

Copyright © 2024 Reason Financial all rights reserved.

[i] McCormick, Myles, and Claire Jones. “How Long Can the US Economy Defy Expectations?” FT.Com, Financial Times, 26 July 2025, www.ft.com/content/b9f739a7-d515-4371-8f7f-5e19aa96e1a4.

[ii] Reklaitis, Victor. “Trump’s Trade Deals: Here Are the Countries That Have Made Agreements, and Those That Haven’t.” Marketwatch, Morningstar, 23 July 2025, www.morningstar.com/news/marketwatch/20250723162/trumps-trade-deals-here-are-the-countries-that-have-made-agreements-and-those-that-havent.

[iii] Goldman, David. “So, Has Anything Actually Gotten More Expensive Because of Trump’s Tariffs? | CNN Business.” CNN, Cable News Network, 20 June 2025, www.cnn.com/2025/06/20/business/tariff-price-increases-inflation-explained.

[iv] Palmer, Ewan. “Fed Chair Will Serve out Full Term to Spite Trump.” The Daily Beast, The Daily Beast Company, 25 July 2025, www.thedailybeast.com/fed-chair-jerome-powell-to-serve-out-full-term-to-spite-trump/.

[v] Lichtenberg, Nick. “Jerome Powell Should Resign, Top Economist Mohamed El-Erian Says, Citing a Scandal Trump Hasn’t Even Mentioned.” Fortune, Fortune, 22 July 2025, fortune.com/2025/07/22/jerome-powell-should-resign-top-economist-mohamed-el-erian-insider-trading-scandal/.

[vi] Goldman, David. “So, Has Anything Actually Gotten More Expensive Because of Trump’s Tariffs? | CNN Business.” CNN, Cable News Network, 20 June 2025, www.cnn.com/2025/06/20/business/tariff-price-increases-inflation-explained.

[vii] Higgs, Milly. “One US Tax Policy OECD Countries Should Copy.” Tax Foundation, Tax Foundation, 24 July 2025, taxfoundation.org/blog/us-bonus-depreciation-oecd-tax-policy/.

[viii] Kelleher, Mark. “OBBBA: Tax Deductions for Tips and Overtime Pay Explained.” Tax & Accounting Blog Posts by Thomson Reuters, Thomson Reuters, 28 July 2025, tax.thomsonreuters.com/blog/retroactive-tax-law-for-tips-and-overtime-demands-immediate-action-payroll-expert-cautions/.

[ix] Alaina.bergen@thomsonreuters.com. “How the ‘one Big Beautiful Bill’ Reshapes Salt Planning.” Tax & Accounting Blog Posts by Thomson Reuters, Thomson Reuters, 25 July 2025, tax.thomsonreuters.com/blog/how-the-one-big-beautiful-bill-reshapes-salt-planning/.

[x] Alaina.bergen@thomsonreuters.com. “How the ‘one Big Beautiful Bill’ Reshapes Salt Planning.” Tax & Accounting Blog Posts by Thomson Reuters, Thomson Reuters, 25 July 2025, tax.thomsonreuters.com/blog/how-the-one-big-beautiful-bill-reshapes-salt-planning/.

[xi] Alaina.bergen@thomsonreuters.com. “How the ‘one Big Beautiful Bill’ Reshapes Salt Planning.” Tax & Accounting Blog Posts by Thomson Reuters, Thomson Reuters, 25 July 2025, tax.thomsonreuters.com/blog/how-the-one-big-beautiful-bill-reshapes-salt-planning/.

[xii] Alaina.bergen@thomsonreuters.com. “How the ‘one Big Beautiful Bill’ Reshapes Salt Planning.” Tax & Accounting Blog Posts by Thomson Reuters, Thomson Reuters, 25 July 2025, tax.thomsonreuters.com/blog/how-the-one-big-beautiful-bill-reshapes-salt-planning/.