4th Quarter 2025 – Economic and Market Update

AN ECONOMIC AND MARKET UPDATE

October 2025

EXECUTIVE SUMMARY

- The Federal Reserve announced another 25 basis point rate cut, but cautioned against expecting a further cut in December.

- The First Brands implosion was another reminder that we have a debt problem in this country.

- Trump Accounts are coming for the kids and that is a good thing.

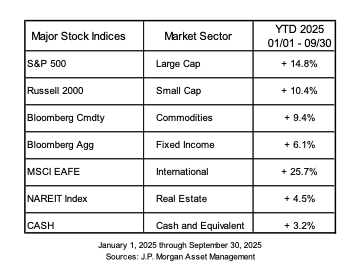

International markets have been the best performers of the year as we move into the fourth quarter. They have done so amongst a backdrop of increased government spending, improved geopolitical outlook, and a weaker dollar. The U.S. domestic markets have done quite well, with market breadth, meaning the percentage of companies doing well, is getting better. Market gains are now not solely being driven by the Magnificent 7. The more participation in a stock market rally the better as it is a better overall indicator of a healthy economy versus the very top heavy returns that we saw in 2024. The Federal Reserve has now made two interest rate cuts of 25 basis points (bps) each putting the Federal Funds Rate in the 3.75% to 4% target range. Chair Powell cautioned against markets expecting an additional cut later in the year specifying that it would be data driven and is not a foregone conclusion.

THE FED’S RECENT RATE CUT

The most recent rate cut in October was delivered with a warning that “risks to inflation are tilted to the upside and risks to employment to the downside – a challenging situation. There is no risk-free path for policy as we navigate this tension between our employment and inflation goals.” Chair Powell issued these remarks in his most recent press conference. Further rate cuts were assumed coming out of the September meeting. This is perhaps his way of shooting down the idea that another is a given. The Federal Reserve seems very concerned that we can end up in a mild stagflation period with inflation rising while the job market weakens.[i]

Polymarket is an online gambling forum where you can bet on just about anything. We don’t advocate gambling, but it is telling to see which direction money is going.

Source: polymarket.com, data as of 10/29/25

Chair Powell may be telling us he is not looking at a rate cut in December, but the money is betting there will be one. He also announced they would end their balance sheet runoff. In general, expansion of the Fed balance sheet is expansionary monetary policy and is related to strategies the Federal Reserve came up with to fight back against the Financial Crisis of 2008/09 and the Covid Pandemic. They have been reducing their balance sheet holdings in the last few years which has been a form of quantitative tightening. In short, the Fed announced another rate cut which is expansionary, and they stopped reducing their balance sheet which is also expansionary. We will see if they end up cutting again in December, but we are not confident enough to join in with those placing bets on Polymarket.

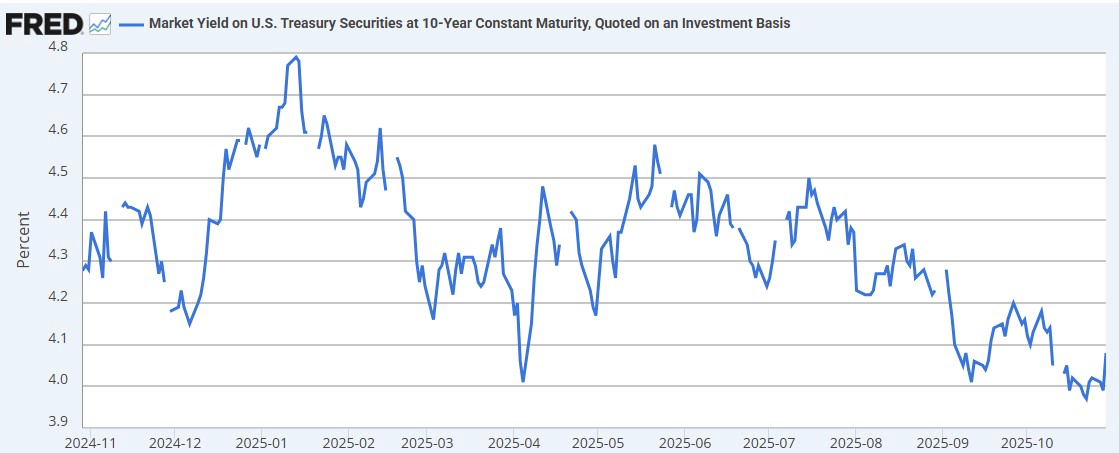

For those looking at how Federal Reserve rate cuts impact borrowing rates for home purchases, you should look to movement in the 10-year Treasury. 10-year Treasury rates have not changed much off of the rate cut news. The unfortunate conclusion is that rate cuts by the Federal Reserve are not likely to improve movement in the housing sector at this time. If you are hoping for a cheaper mortgage you are going to be hoping for awhile longer. Rates are lower than they were at the beginning of the year, but not by much.[ii]

Source: Board of Governors of the Federal Reserve System (US) via FRED, data as of 10/29/25

THE DEBT PROBLEM

Recent defaults by First Brands and Tricolor shined a light into an area of debt financing that many people are not aware of: the world of private credit and leveraged loans. Leveraged loans work a lot like the Collateralized Debt Obligations (CDOs) of the 2000’s that exacerbated the financial crisis turning it into a collapsing building more than just a burning building. Just like CDO’s were sliced and diced into a myriad of different investment products, so are Collateralized Loan Obligations (CLO’s).

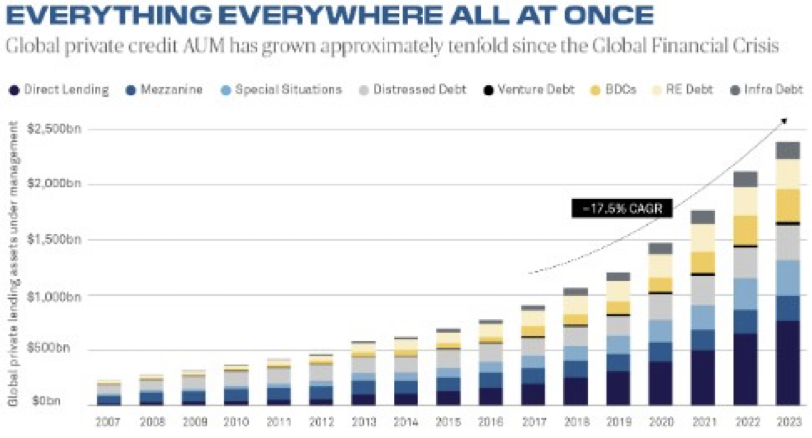

Leveraged loans and private credit are not the same thing, but they do both represent a concerning expansion in debt. Over the last 15 years a product called a BDC, or Business Development Company, became a much more popular means of accomplishing two goals. First, to provide credit to small and mid-sized companies in a very tough lending environment coming out of the financial crisis. Second, to provide a higher yielding debt instrument for investors in a very low yield world. The yield picture has changed some as developed economies reacted to inflation by raising interest rates. The addiction to credit, however, has not changed. BDC’s and other forms of private credit have ballooned as you can see below.[iii]

Source: Preqin, Goldman Sachs Global Investment Research, as of December 31, 2023

The failure of First Brands causes a bit of a jump in blood pressure for anyone what was in the financial space during ’08 and ’09. In recent remarks, Jamie Dimon, CEO of JP Morgan Chase, said, “I probably shouldn’t say this, but when you see one cockroach, there are probably more. And so we should – everyone should be forewarned on this one.”[iv]

Debt fueled expansion has been the primary driver for the United States economy this century. Relaxed lending standards for home acquisition in the early 2000’s. Private credit coming out of the financial crisis for businesses. Quantitative easing from the Federal Reserve to boost the economy post-financial crisis and during Covid. Easy access to credit and easy money monetary policy has created a boom in the stock markets but one that comes with a caveat. In the words of David Solomon, CEO of Goldman Sachs, “if we continue on the current course and we don’t take the growth level up, there will be a reckoning.”

The failure of First Brands and Tricolor in and of themselves are not very concerning to us. They do, however, serve to caution against being overly aggressive in the fixed income side of our investment strategies. High-quality and shorter duration debt remain the preferred strategy to protect against both stock market volatility and risky debt.

If there are more cockroaches and if growth does not appear to support the lofty valuations in the stock market, we could be in for a rough patch. On balance, however, it is a time to rebalance portfolios, take gains and keep portfolios well-diversified.

THE FINANCIAL PLANNING CORNER

Trump Accounts are coming. We are still awaiting guidance on how they will be seeded by the government and where you will be able to open the account. However, this is a $1,000 leg up for any kid born between the period of January 1, 2025 and December 31, 2028. If you have a child or are the grandparent of a child born during this period, it is a good idea to keep an eye out for further legislative explanation on how to participate in this program.[v]

Built into the OBBBA (One Big Beautiful Bill Act of 2025) is language allowing the establishment of a savings account for a newborn that can be funded with up to $5,000/annually, with the first $1,000 being seeded by the Federal Government.[vi]

From what we can tell the first funding of a Trump account will be available in July 2026. Technically, anyone under the age of 18 is eligible for a Trump account, but only babies born within the 3-year window mentioned above will qualify for the $1,000 seed funding by the Federal Government.

This is an incredible usage of the time value of money and ideally would create a tradition of savings that will follow children into adulthood. Traditionally, there have been a couple routes people went in order to start saving for children. First, a college savings plan such as a 529 Plan. Second, some sort of transfer to minors account such as an UTMA or UGMA. The Trump Account’s are effectively a third rail with more flexibility than a 529 but with more tax efficiency than an UTMA or UGMA, as they will grow tax deferred and can be used for more than just college.

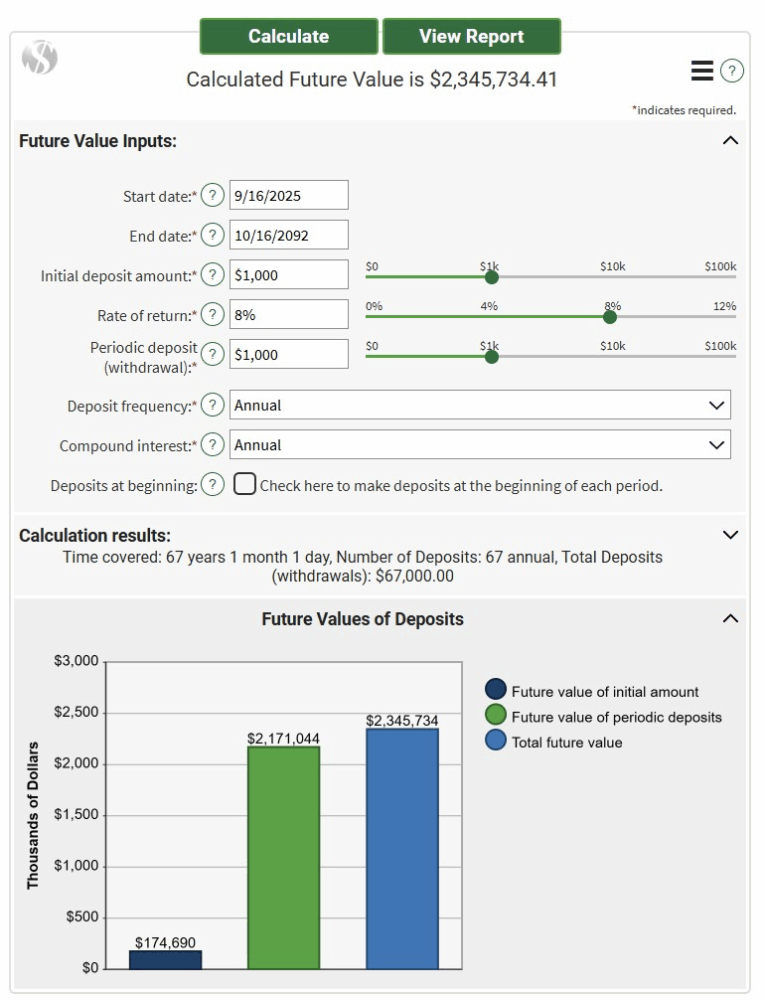

This is essentially an IRA for a child, without the hurdle of earned income to be able to contribute. There are a variety of financial calculators you can use. Below is an output from Dinkytown.net, our favorite financial calculator aggregator.[vii]

Again, more information will be coming out in the months ahead but please earmark this tidbit as something to take advantage of for your children or grandchildren. People always want to know how to fund savings for their children and doing so is about to get a lot easier.

Source: Dinkytown.net, assuming a starting deposit of $1,000 initially with $1,000 deposited annually for 67 years at an 8% annualized growth rate.

Our commitment to guiding you through these evolving economic conditions remains unwavering. We encourage you to reach out with any questions or concerns as we continue to move forward in an uncertain world.

DISCLOSURE

This material is for general information only and is not intended to provide specific advice or recommendations for any individual. There is no assurance the views or strategies discussed are suitable for all investors or will yield positive outcomes. Investing involves risks including possible loss of principal. Any company names noted herein are for educational purposes only.

All information is believed to be from reliable sources; however we make no representation as to its completeness or accuracy. All economic and performance data is historical and not indicative of future results. Market indices discussed are unmanaged. Investors cannot invest in unmanaged indices. Additional risks are associated with international investing, such as currency fluctuations, political and economic instability and differences in accounting standards.

Investing in securities in emerging markets involves special risks due to specific factors such as increased volatility, currency fluctuations and differences in auditing and other financial standards. Securities in emerging markets are volatile and can decline significantly in response to adverse issuer, political, regulatory, market, or economic developments.

An index is a statistical measure of change in an economy or a securities market. In the case of financial markets, an index is an imaginary portfolio of securities representing a particular market or a portion of it. Each index has its own calculation methodology and is usually expressed in terms of a change from a base value. Thus, the percentage change is more important than the actual numeric value. An investment cannot be made directly into an index.

Investing in fixed income securities involves credit and interest rate risk. When interest rates rise, bond prices generally fall. Investing in commodities may involve greater volatility and is not suitable for all investors. Investing in a non-diversified fund that concentrates holdings into fewer securities or industries involves greater risk than investing in a more diversified fund. The equity securities of small companies may not be traded as often as equity securities of large companies so they may be difficult or impossible to sell. Neither diversification nor asset allocation assure a profit or protect against a loss in declining markets. Past performance is not an indicator of future results.

Financial Planning offered through Reason Financial, a state Registered Investment Advisor. Investment advice offered through Merit Financial Group, LLC an SEC Registered Investment Advisor. Merit Financial Group and Reason Financial are separate entities. Tax related services offered through Reason Tax Group. Reason Tax Group is a separate legal entity and not affiliated with Merit Financial Group, LLC. Sean P. Storck CA Insurance Lic#OF25995 and Steven W. Pollock CA Insurance Lic#OE98073

Copyright © 2024 Reason Financial all rights reserved.

[i] “FOMC Press Conference, October 29, 2025.” Federal Reserve, YouTube, www.youtube.com/watch?v=gZsAKn1UtH4. Accessed 30 Oct. 2025.

[ii] “How Bonds Affect Mortgage Rates: Chase.” Credit Card, Mortgage, Banking, Auto, www.chase.com/personal/mortgage/education/financing-a-home/how-bonds-affect-mortgage-rates. Accessed 30 Oct. 2025.

[iii] “Business Development Company.” Wikipedia, Wikimedia Foundation, 29 Sept. 2025, en.wikipedia.org/wiki/Business_Development_Company.

[iv] Edwards, Jim. “Jamie Dimon Issues Private Credit Warning: ‘When You See One Cockroach, There Are Probably More.’” Fortune, Fortune, 15 Oct. 2025, fortune.com/2025/10/15/jamie-dimon-issues-private-credit-warning-when-you-see-one-cockroach-there-are-probably-more/.

[v] “Trump Accounts Give the next Generation a Jump Start on Saving.” The White House, The United States Government, 29 Aug. 2025, www.whitehouse.gov/research/2025/08/trump-accounts-give-the-next-generation-a-jump-start-on-saving/.

[vi] “What Are Trump Accounts?” Savings for Newborns, www.axosbank.com/personal/insights/finance/financial-planning/what-are-trump-accounts. Accessed 30 Oct. 2025.

[vii] https://www.dinkytown.net/java/future-value-calculator.html