2nd Quarter 2025 – Economic and Market Update

AN ECONOMIC AND MARKET UPDATE

May 2025

EXECUTIVE SUMMARY

- GDP turns negative for the first time in three years driven largely by higher imports in Q1 2025 in anticipation of President Trump’s tariff policy.

- A “big, beautiful bill” giving us clarity on future tax policy is in the works.

- There is no better time than the present to do some spring cleaning in regard to your estate planning.

Tariffs have taken over all other financial discussions since the close of the quarter. We knew something was coming but we did not know the substance until April 2nd, branded “Liberation Day” by the administration. After the announcement of the tariffs there was a broad market sell-off. Markets expected lower tariffs and the higher tariff figures spooked everyone. Since the announcement there has been a tit for tat response by China, backtracking on a variety of industries and imports, and pausing of tariffs on most countries for 90 days. A tariff is a tax, a tax highly likely to be passed through to the consumer. Domestic alternatives will be winners, and to the extent there are no alternatives there will be losers.[i]

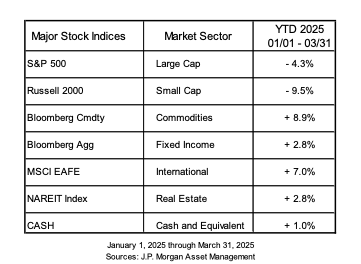

The big losers year-to-date have been domestic stocks with both the S&P 500 and the Russell 2000 down significantly. Commodities and developed market international stocks have performed the best. Some recovery in international stocks was to be expected with historic valuation differences between international and U.S. stock valuations.

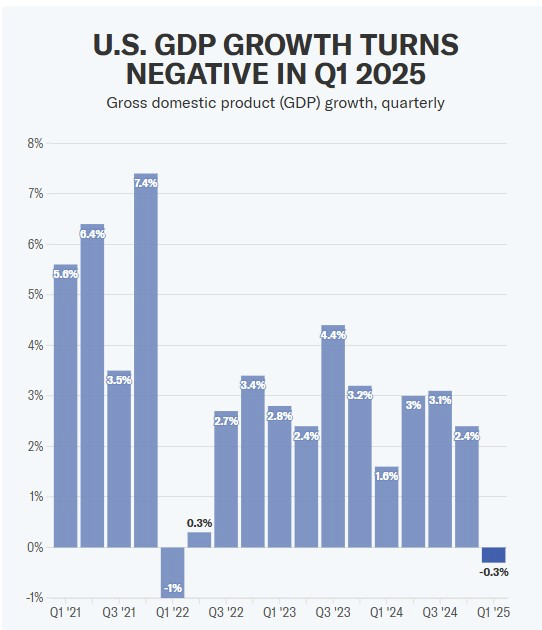

Source: Bureau of Economic Analysis, yahoo!finance

The first quarter of 2025 is estimated to have contracted by .3%. This is a sharp departure from the prior two years where the economy maintained solid growth despite a variety of concerns. At this point the explanation for the decline is being attributed to a surge in imports in expectation of the announcement by President Trump of forward tariff policy. A negative trade balance reduces GDP. Excessive inventory buildup in anticipation of higher future costs drove Q1 imports higher than expected. On the plus side, the contraction of .3% is less than the 1.4% downturn that the Atlanta Fed GDPNow tracker was forecasting, although this figure is likely to be revised in the coming weeks.[ii]

ON TARIFFS and WHAT TO DO

We have been told specifically by Treasury Secretary Bessent that the strategy, “it’s really a three-legged stool on the economic policy. It’s trade, it’s tax, and it’s de-regulation.” Howard Lutnick, Commerce Secretary, and Scott Bessent, Treasury Secretary, are both highly respected individuals with a lot of experience navigating markets. It is easy to take a partisan approach when looking at members of the President’s Cabinet if you do not like the current White House occupant, but these two guys have been around for awhile and done some incredible things. We make this statement not as a confidence builder in the overall strategy, but as an indicator they are to be taken seriously.[iii]

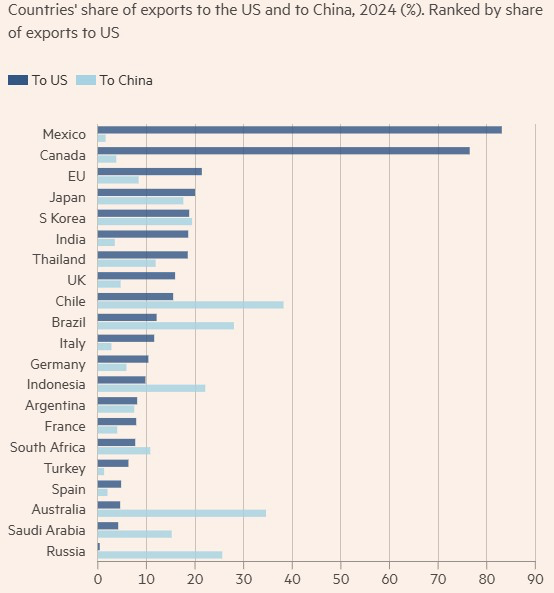

Source: IMF DOTS, EU excludes intra-EU trade

In the positive column the fight between the U.S. and China got a little less serious with China easing tariffs on a variety of imports from the U.S. The President has also extended the date at which most countries will be impacted by the tariffs. Call it a flip-flop, call it a negotiation, but the sharp edge of the tariff announcement which caused so much consternation to the markets at the start of the 2nd quarter has been filed down a bit. How hard will trade negotiations be? That likely has a lot to do with who the dominant trading partners are. As you can see above, the US has dominant trade relationships, relative to China, with Mexico, Canada and the European Union. If this trade war is really about China, the data above is as good an indicator as any to the ease at which we will see some sort of long term strategy take shape. U.S. companies are very adaptible, but there has to be certainty on what they are adapting to. The sooner the trade battles can be resolved the better.[iv]

“We must expect volatility to remain high as this tariff picture begins to clear itself.” Brian Andrew, Chief Investment Officer of Merit Financial[v]

Quality and diversification are our keys to investing in the current environment. For us quality means tiliting towards companies with free-cash flow and low-leverage on the equity side of portfolios.

TAXES and THE BIG BEAUTIFUL BILL

There is a “big, beautiful bill” coming around the corner if you had not heard. It is going to, hopefully, address the expiring tax provisions of the Tax Cuts and Jobs Act of 2017. This is important as it will create certainty around tax policy at a time when we need certainty about something. There is no reason at this time to think it will fail to pass, but if negotiations drag out and the bill is delayed, tax rates will go up substantially on January 1, 2026. This will be an additional item for markets to price in if it does not pass, not a good thing. Broad strokes have already been painted but there is a significant gap in what House Republicans are looking for versus what Senate Republicans are looking for. The House wants to see $1.5 trillion in budget cuts and the Senate wants to see $4 billion in cuts. There will be a lot more to fight over than budget cuts, and we expect to see some political fireworks as the bill is worked out. They are currently targeting passage of the bill by July 4th. We sense some potential branding in the works similar to the “Liberation Day” announcement for the tariffs.[vi]

From a tax and financial planning standpoint the most significant item is the statement from President Trump that he wants to remove Federal taxation of Social Security income. If this occurs it will dramatically change the tax liability of many current retirees. As it stands a simple extension will keep current tax rates as they are.

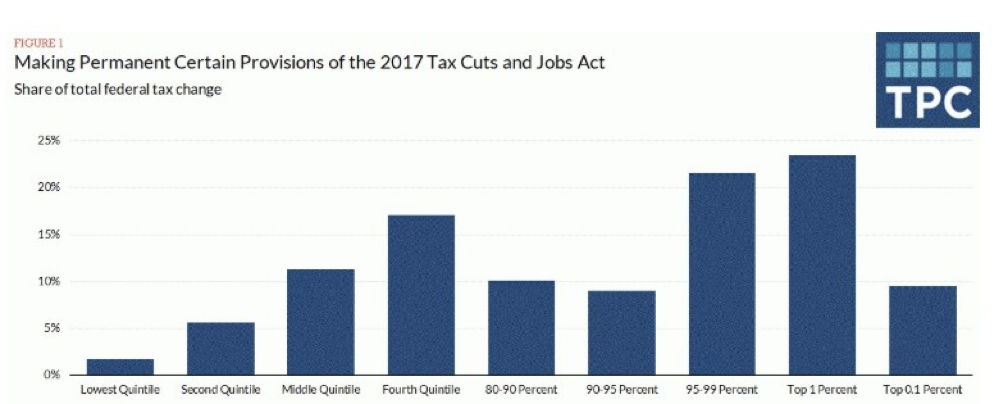

Source: Urban-Brookings Tax Policy Center Microsimulation Model (version 0324-1)[vii]

The graph above is the estimate for where the tax savings for the tax paying citizenry will show up. The expectation is for tax savings to be spread across all income quintiles with the top 5% of taxpayers experiencing roughly 45% of total tax savings. It is top heavy, but about 75% of households pay less tax under an extended TCJA. This analysis is based on the extension of the TCJA and does not take into consideration any of the campaign promises made by President Trump involving taxes on Social Security, tips, and overtime.[viii]

Referencing back to the three-legged stool comment by Secretary Bessent, lower taxes are key to their overall strategy to stimulate growth. Cutting taxes stimulates growth. Cutting Federal spending decreases growth. Whiff on an extension of the TCJA and that three-legged stool has a pretty wobbly leg.

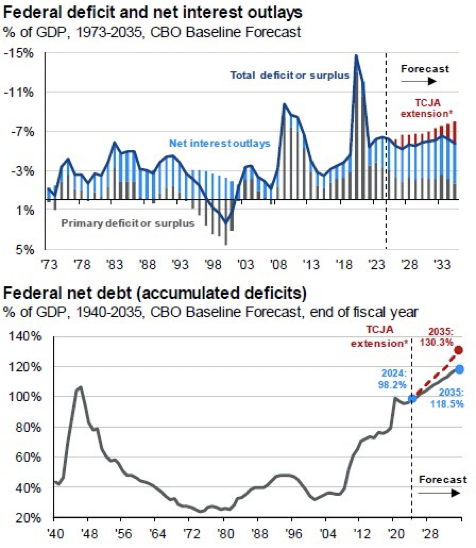

The extension of the TCJA does create problems which the infamously named DOGE crew is attempting to resolve. Current CBO estimates reflect increased deficit spending with an extension of current tax law as you can see below. Increased deficit spending will only exacerbate the cost to service the debt, further worsening the deficit until something in the financial system finally breaks. The red you see represents projected deficit spending and projected Federal net debt due to extending current tax laws.

The pace and breadth of the Trump administration in advancing a wide variety of financial strategies at once is due to the competing impacts of all the different actions. A lot of things have to go right for the strategy of higher tariffs, lower taxes, lower Federal spending, less regulations, etc. to work. Secretary Bessent calls it a three-legged stool. To us it feels more like pulling a bunch of gears and pushing a bunch of buttons in an airliner and expecting it to get off the ground because you hit the right combination. Although many metrics of the economy are still solid, recession risks have risen.[ix]

Source: CBO, J.P. Morgan Asset Management, Guide to the Markets – U.S. Data are as of March 31, 2025

THE FINANCIAL PLANNING CORNER – DO SOME SPRING CLEANING

A not really fun part of our financial lives is maintenance. By maintenance we mean looking at the status of decisions we made in the past, and making sure they are still appropriate and relevant for where we are today. In the vein of doing some spring cleaning after a long winter, now is a great time to do some spring cleaning on your estate plans. Or just look at what you did and decide all is still well with the world.

- Are your beneficiary choices and allocations still appropriate?

- Have you checked to make sure the language in your trust is up to date?

- Is your home titled to your trust?

- Are your successor trustee choices still appropriate?

- Are your beneficiaries old enough and mature enough to inherit outright? Or should parameters be established to protect them from themselves?

- Do you want to do anything specific for your grandchildren?

- Are there any charities you want to add to the list of beneficiaries?

- Have you consolidated your finances and made the execution of your wishes as easy as possible for your successor trustee?

- Is your appointed healthcare power-of-attorney still the person you want making decisions regarding your health if you are incapacitated?

We are happy to discuss and think through any of these items with you. However, remember that many of these items are in the legal realm and will require engaging with an estate planning attorney.

Our commitment to guiding you through these evolving economic conditions remains unwavering. We encourage you to reach out with any questions or concerns as we continue to move forward in an uncertain world.

DISCLOSURE

This material is for general information only and is not intended to provide specific advice or recommendations for any individual. There is no assurance the views or strategies discussed are suitable for all investors or will yield positive outcomes. Investing involves risks including possible loss of principal. Any company names noted herein are for educational purposes only.

All information is believed to be from reliable sources; however we make no representation as to its completeness or accuracy. All economic and performance data is historical and not indicative of future results. Market indices discussed are unmanaged. Investors cannot invest in unmanaged indices. Additional risks are associated with international investing, such as currency fluctuations, political and economic instability and differences in accounting standards.

Investing in securities in emerging markets involves special risks due to specific factors such as increased volatility, currency fluctuations and differences in auditing and other financial standards. Securities in emerging markets are volatile and can decline significantly in response to adverse issuer, political, regulatory, market, or economic developments.

An index is a statistical measure of change in an economy or a securities market. In the case of financial markets, an index is an imaginary portfolio of securities representing a particular market or a portion of it. Each index has its own calculation methodology and is usually expressed in terms of a change from a base value. Thus, the percentage change is more important than the actual numeric value. An investment cannot be made directly into an index.

Investing in fixed income securities involves credit and interest rate risk. When interest rates rise, bond prices generally fall. Investing in commodities may involve greater volatility and is not suitable for all investors. Investing in a non-diversified fund that concentrates holdings into fewer securities or industries involves greater risk than investing in a more diversified fund. The equity securities of small companies may not be traded as often as equity securities of large companies so they may be difficult or impossible to sell. Neither diversification nor asset allocation assure a profit or protect against a loss in declining markets. Past performance is not an indicator of future results.

Financial Planning offered through Reason Financial, a state Registered Investment Advisor. Investment advice offered through Merit Financial Group, LLC an SEC Registered Investment Advisor. Merit Financial Group and Reason Financial are separate entities. Tax related services offered through Reason Tax Group. Reason Tax Group is a separate legal entity and not affiliated with Merit Financial Group, LLC. Sean P. Storck CA Insurance Lic#OF25995 and Steven W. Pollock CA Insurance Lic#OE98073

Copyright © 2024 Reason Financial all rights reserved.

[i] Durkee, Alison. “Trump Offers Automakers Tariff Reprieve-Latest Big Tariff Flip-Flop since ‘Liberation Day.’” Forbes, Forbes Magazine, 29 Apr. 2025, www.forbes.com/sites/alisondurkee/2025/04/29/trump-offers-automakers-tariff-reprieve-latest-big-tariff-flip-flop-since-liberation-day/.

[ii] Jones, Claire. US Economy Contracts at 0.3% Rate as Trump’s Tariffs Prompt Import Surge, Financial Times, 30 Apr. 2025, www.ft.com/content/104ece93-c362-4d78-aaf9-ace4e314ec0c.

[iii] “Treasury Secretary Speaks at Press Briefing.” Youtube, 29 Apr. 2025, https://www.youtube.com/watch?v=tX8cDK5ZDZs. Accessed 29 Apr. 2025.

[iv] “Trump Tariffs Live Updates: China Eases Tariffs on Select US Goods as Trump Says Beijing Will ‘eat’ the Costs.” Yahoo! Finance, Yahoo!, 30 Apr. 2025, finance.yahoo.com/news/live/trump-tariffs-live-updates-china-eases-tariffs-on-select-us-goods-as-trump-says-beijing-will-eat-the-costs-191201015.html.

[v] Andrew, Brian. “April 2025 Market Update.” Merit Financial Advisors, 29 Apr. 2025, www.meritfinancialadvisors.com/blog/april-2025-market-update/?tm_source=account%2Bengagement&utm_medium=email&utm_campaign=april%2B2025%2Bmarket%2Bupdate%2Bemail&utm_id=april%2B2025%2Bmarket%2Bupdate%2Bemail.

[vi] Beggin, Riley. “What to Know as Congress Starts Working on Donald Trump’s ‘Big Beautiful Bill.’” USA Today, Gannett Satellite Information Network, 29 Apr. 2025, www.usatoday.com/story/news/politics/2025/04/29/trump-priorities-legislation-congress/83326091007/.

[vii] Gleckman, Howard. “Those Making $450,000 and up Would Get Nearly Half the Benefit of Extending the TCJA.” Tax Policy Center, 8 July 2024, taxpolicycenter.org/taxvox/those-making-450000-and-would-get-nearly-half-benefit-extending-tcja.

[viii] “No Tax On Tips, Social Security, Overtime: Trump Teases ‘Biggest Bill Ever Passed.’” The Economic Times, YouTube, 29 Apr. 2025, www.youtube.com/watch?v=KOz0sVvkvYc.

[ix] “What Is the Probability of a Recession?: J.P. Morgan Research.” What Is the Probability of a Recession? | J.P. Morgan Research, J.P. Morgan, 15 Apr. 2025, www.jpmorgan.com/insights/global-research/economy/recession-probability.