Special Report – A Third Update

We have now seen significant responses from both the Federal Reserve and the Federal Government to the threat that the Coronavirus pandemic represents to the economy. The monetary policy came first with a .5% cut to the Fed Funds rate, followed quickly by an additional 1% cut on Sunday evening to bring us to 0% interest rates again. Monetary policy tools were implemented to provide liquidity in the financial markets and ensure that the financial system continues to work as expected. The Federal Government has revealed the extent of fiscal stimulus we can expect, and the numbers are significant. In addition, a 90-day extension to file and pay federal tax returns and liabilities has been announced.

The seriousness with which much of the public is taking this incredible set of circumstances has escalated since last weekend. Along with school closures we are now seeing temporary store closures (Macy’s and Dick’s Sporting Goods), bars and restaurants closed to in-store patrons, California state parks shutdown, Costco implementing strong social distancing measures, and the list goes on.

The end goal of social distancing policies and financial policies are the same: flatten the curve. For social distancing and shutdowns, it is to flatten the growth curve of the virus. For fiscal and monetary policy, it is to flatten the curve of the steep economic slowdown.

“I’LL RESIST THE IMPULSE TO GUESS” – the financial markets

“I’ll resist the impulse to guess,” was the response by Fed Chairman Jerome Powell when asked in the most recent Federal Reserve Press Conference, performed via teleconference, as to the length of time we are looking at to work this shock out of the system. This was preceded by a comment that “it’s in fact unknowable”.

The good news from his press conference came from his description of the financial system. “We’ve built a very resilient financial system. The banks are highly capitalized, lots of liquidity, much better at understanding and managing their risks, their resilience to stress. So, our financial stability focus, our focus on events like this over the last 10 years will pay dividends in the sense that you have a much more resilient financial system than you’ve had before”.

A key concern for us has been the response of the bond markets to what is happening. The last time we faced a large crisis, bonds moved in tandem with stocks until the differences between good and bad debt were figured out. It can be hard to remember, but we would walk into the office each day wondering what major company or institution would be declaring bankruptcy next. A key component of managing risk inside of our portfolios is to offset stocks with bonds and cash, so any dislocation in this area is problematic.

In order to provide a higher level of security in our bond portfolios, we have shifted our bond allocations to 50% short-term U.S. treasuries. This is a proactive move in case the downturn lasts longer than anticipated and the current health of the financial system changes. This is also in anticipation of a low-interest rate environment presenting challenges to long-duration bond funds once rates begin rising again.

THE BOTTOM ALWAYS FEELS THE WORST

A little over a decade ago the markets bottomed out on March 2, 2009. They then proceeded to move upwards quickly, nearly doubling over the course of a year. During this time we still faced challenging news, including Swine Flu (H1N1) which infected nearly 60 million Americans, the potential bankruptcy of multiple countries (Greece, Italy, Spain), and a municipal bond crisis in the U.S. which some were calling a return of the financial crisis. The broader economy continued to improve despite all this, leading to the historic run-up of the last decade.

It is impossible to call the bottom, but it will be here, and it will only be visible once it is in the rearview mirror.

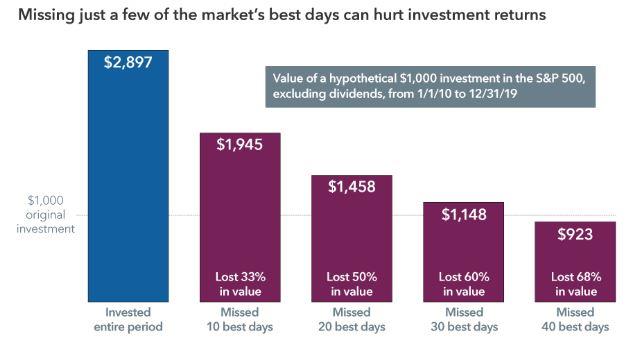

This is a great time to remember that it is time in the market that matters, not market timing. The graph below illustrates the impact of missing the good days, despite accepting the bad days. It is a reminder that persistence and disciplined investment strategies win the day. Psychologically this is hard to do. Economists like to believe we are rational actors. Behavioral psychologists like to prove that we are not.

Sources: RIMES, Standard & Poor’s. As of 12/31/19. Values in USD[/caption]

We are taking consistent action to rebalance all portfolios as frequently as possible during this time to maintain both risk tolerance and asset allocation. This will put us in a good position to participate in the market recovery when it begins.

THE GOOD NEWS

A Reuters report out of China late yesterday indicates China has reported no new local coronavirus transmissions for the first time. This is incredible news and should be encouraging to every other country that is in the earlier stages of the fight against the virus. Wuhan, the early epicenter of the virus, is now on a 14-day watch to see whether containment of the virus has been successful. To a large extent, this is an indicator that China is back online.

We are still here, healthy, and working on making sure your financial and tax needs are met. We have moved most staff to a work-from-home situation. We are doing our best to limit in-office interactions. Thank you for your understanding and your assistance as we do our best to protect the most vulnerable parts of the population.

We are here to help you make rational, informed and well-reasoned decisions, and we thank you for your continued trust and support. Your input is always welcome, and we ask that you contact us with any questions or concerns.

ADDITIONAL RESOURCES

A variety of interesting resources we have found useful during this time are attached as links here:

COVID-19 Global Case Map

https://gisanddata.maps.arcgis.com/apps/opsdashboard/index.html#/bda7594740fd40299423467b48e9ecf6

Why Outbreaks Like Coronavirus Spread Exponentially, and How to “Flatten the Curve”

University of Minnesota – COVID-19 Maps and Visuals

http://www.cidrap.umn.edu/covid-19/maps-visuals

DISCLOSURE

All information is believed to be from reliable sources; however, we make no representation as to its completeness or accuracy. All economic and performance data is historical and not indicative of future results. Market indices discussed are unmanaged. Investors cannot invest in unmanaged indices. Additional risks are associated with international investing, such as currency fluctuations, political and economic instability and differences in accounting standards.

Investing in securities in emerging markets involves special risks due to specific factors such as increased volatility, currency fluctuations and differences in auditing and other financial standards. Securities in emerging markets are volatile and can decline significantly in response to adverse issuer, political, regulatory, market, or economic developments.

An index is a statistical measure of the change in an economy or a securities market. In the case of financial markets, an index is an imaginary portfolio of securities representing a particular market or a portion of it. Each index has its own calculation methodology and is usually expressed in terms of a change from a base value. Thus, the percentage change is more important than the actual numeric value. An investment cannot be made directly into an index.

Investing in fixed income securities involves credit and interest rate risk. When interest rates rise, bond prices generally fall. Investing in commodities may involve greater volatility and is not suitable for all investors. Investing in a non-diversified fund that concentrates holdings into fewer securities or industries involves greater risk than investing in a more diversified fund. The equity securities of small companies may not be traded as often as equity securities of large companies so they may be difficult or impossible to sell. Neither diversification nor asset allocation assures a profit or protect against a loss in declining markets. Past performance is not an indicator of future results.

The financial professionals at Reason Financial are registered representatives with and securities and Retirement Plan Consulting Program advisory services offered through LPL Financial, a Registered Investment Advisor. Member FINRA/SIPC. Financial Planning offered through Reason Financial, a state Registered Investment Advisor. Investment advice offered through Merit Financial Group, LLC an SEC Registered Investment Advisor. Merit Financial Group and Reason Financial are separate entities from LPL Financial. Tax related services offered through Reason Tax Group, LLC. Reason Tax Group is a separate legal entity and not affiliated with LPL Financial. LPL Financial does not offer tax advice or tax related services. Steven W. Pollock CA Insurance Lic# OE98073, Sean P. Storck CA Insurance Lic# OF25995.

Copyright © 2020 Reason Financial all rights reserved.

Disclosure

This material is for general information only and is not intended to provide specific advice or recommendations for any individual. There is no assurance the views or strategies discussed are suitable for all investors or will yield positive outcomes. Investing involves risks including possible loss of principal. Any company names noted herein are for educational purposes only.

All information is believed to be from reliable sources; however we make no representation as to its completeness or accuracy. All economic and performance data is historical and not indicative of future results. Market indices discussed are unmanaged. Investors cannot invest in unmanaged indices. Additional risks are associated with international investing, such as currency fluctuations, political and economic instability and differences in accounting standards.

Investing in securities in emerging markets involves special risks due to specific factors such as increased volatility, currency fluctuations and differences in auditing and other financial standards. Securities in emerging markets are volatile and can decline significantly in response to adverse issuer, political, regulatory, market, or economic developments.

An index is a statistical measure of change in an economy or a securities market. In the case of financial markets, an index is an imaginary portfolio of securities representing a particular market or a portion of it. Each index has its own calculation methodology and is usually expressed in terms of a change from a base value. Thus, the percentage change is more important than the actual numeric value. An investment cannot be made directly into an index.

Investing in fixed income securities involves credit and interest rate risk. When interest rates rise, bond prices generally fall. Investing in commodities may involve greater volatility and is not suitable for all investors. Investing in a non-diversified fund that concentrates holdings into fewer securities or industries involves greater risk than investing in a more diversified fund. The equity securities of small companies may not be traded as often as equity securities of large companies so they may be difficult or impossible to sell. Neither diversification nor asset allocation assure a profit or protect against a loss in declining markets. Past performance is not an indicator of future results.

Financial Planning offered through Reason Financial, a state Registered Investment Advisor. Investment advice offered through Merit Financial Group, LLC an SEC Registered Investment Advisor. Merit Financial Group and Reason Financial are separate entities. Tax related services offered through Reason Tax Group. Reason Tax Group is a separate legal entity and not affiliated with Merit Financial Group, LLC. Sean P. Storck CA Insurance Lic#OF25995 and Steven W. Pollock CA Insurance Lic#OE98073

Copyright © 2026 Reason Financial all rights reserved.

Continue Reading

2nd Quarter 2026 – Economic and Market Update

Q1 2026 in review: oil shock, S&P 500 down 4.3%, commodities up 24.4%, the cease-fire that became a blockade — and the planning moves that matter most coming out of a quarter like this one.

It’s Now More Common To Have A Baby In Your Thirties Than In Your Twenties

DisclosureThis material is for general information only and is not intended to provide specific advice or recommendations for any individual.…

When Does Refinancing Actually Make Sense? A 2026 Reality Check

If you locked in a mortgage at 7% or higher in 2023 or 2024, you’ve probably been watching rates with…