What is the yield curve and why does it matter?

What is the yield curve and why does it matter?

It’s hard to predict a recession—when to expect one, how severe it might be, and what a recovery could look like. And yet, for all of the variables around predicting a potential recession, there’s one indicator that has been largely accurate, predicting every U.S. recession since the 50s: the yield curve.

The yield curve is a basic function of how interest rates work, and changes to this curve can tell us quite a bit about the economy it reflects. In this article, we’ll dig into what the yield curve is, why it’s used as a recession indicator, and what it’s been telling us over the last few years.

Interest rates and yields

To understand the yield curve, you must understand how interest rates are determined. In the United States, it all starts with the Federal Funds Rate (often abbreviated Fed Funds Rate), which is set by the Federal Reserve. This is, at the most fundamental level, the rate that banks charge each other for overnight loans when they need to bolster their reserves. If banks must pay more to borrow, they in turn charge higher rates on the money they lend to businesses and consumers, and so on.

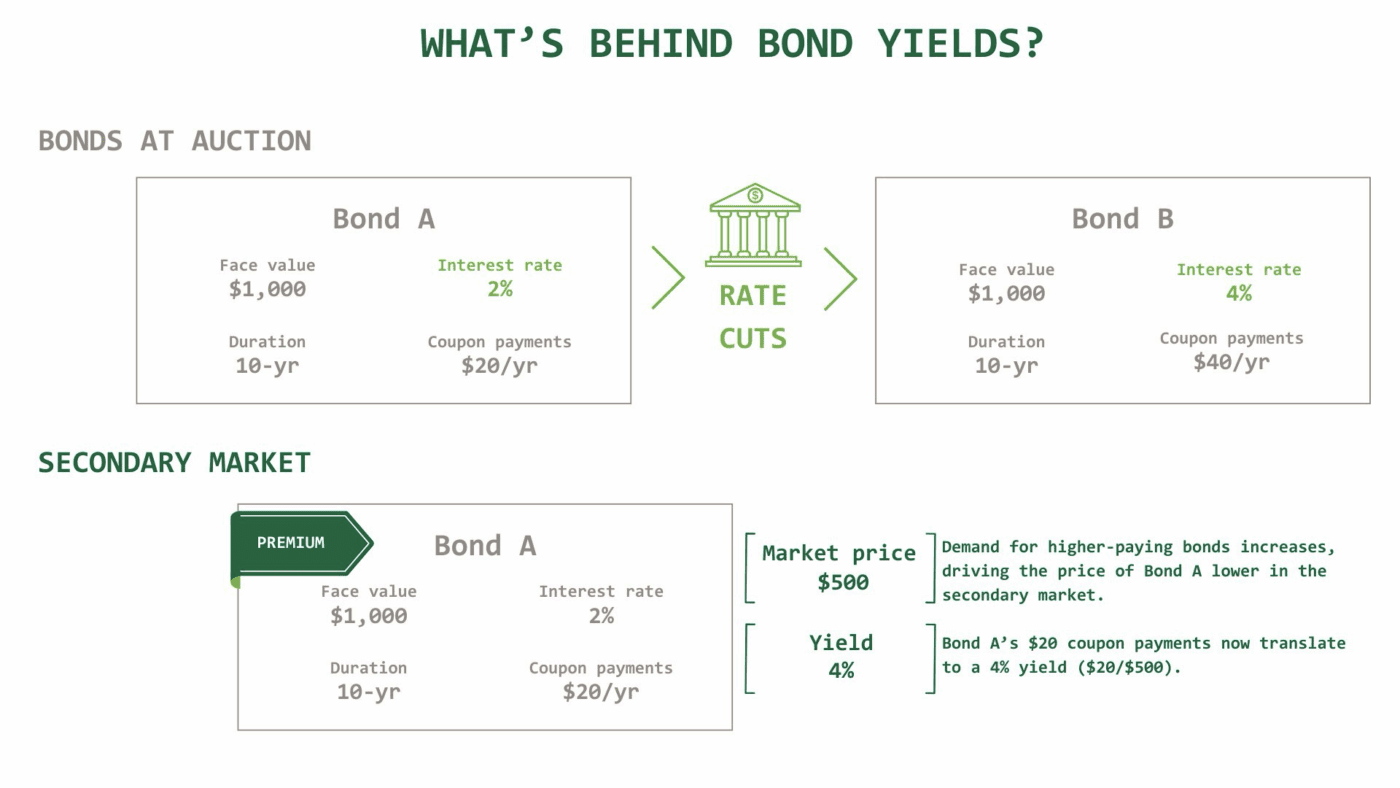

The Fed’s decision on rates also impacts the bond market. More specifically, the Fed influences the interest rate paid on short-term Treasury notes. When the Fed raises its target rate, yields tend to increase, particularly on short-term bonds.

When the Treasury starts to issue new bonds with higher interest rates, the price of existing bonds—bonds traded in the secondary market—tend to fall. Yields climb as a result.

Remember: Yield and interest rates aren’t the same thing. If a $1,000 bond pays $20 in interest, the yield is 2%. However, if the price of that bond falls to $500, and it continues to pay a fixed interest payment of $20, the yield is now 4%.

Yield plus time

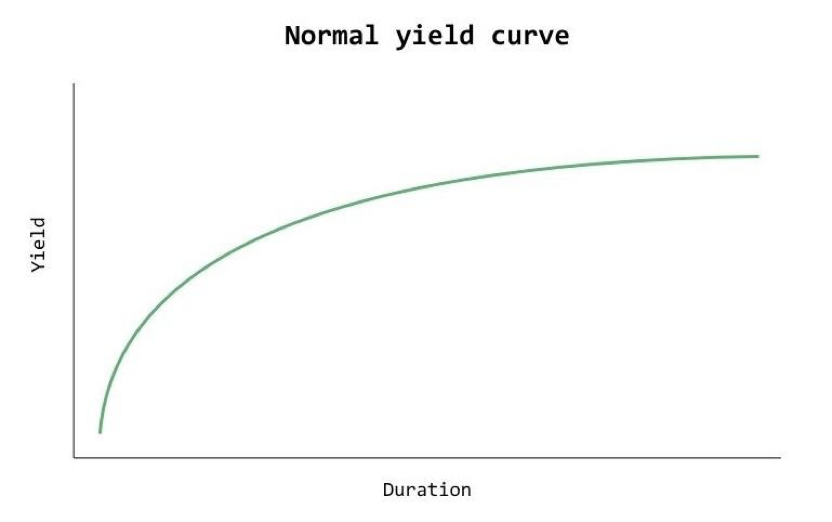

Under normal circumstances, short-term bonds have lower interest rates and yields than long-term bonds. This makes sense when you think about bonds as loans—you take on less risk when you lend someone money for a short period of time. The longer the timeframe, the greater the risk that something will go wrong and the borrower won’t repay the principle.

If you were to plot the average yield on bonds based on their duration, you’d see this risk play out. Short-term bonds tend to yield less; as the duration increases from T-bills to 2-year Treasuries, 10-year Treasuries, on to 20- and 30-year Treasuries, you can see yield increasing.

At least, that’s how it works during normal economic circumstances.

Inverted yield curves

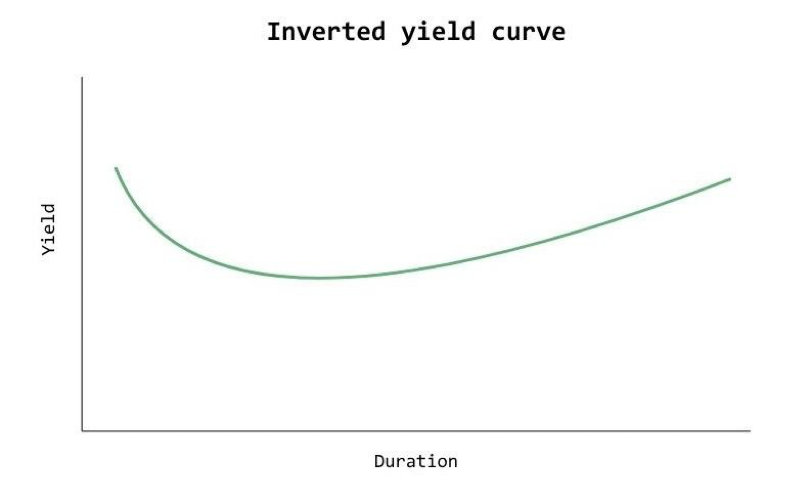

Every so often, the yield curve shifts. The most common shift is a simple flattening of the curve, but it can also fully invert. Inversion usually happens if or when the Fed begins hiking interest rates. Because rate hikes start at the shortest duration possible—overnight lending—and then trickle outwards, rate hikes tend to have a more significant and immediate impact on short-term debt, sending yields higher. Usually, this trickles out into longer-term debt as well, but when that happens, and how significant those yield shifts are, will all show up in the yield curve.

If yields on short-term debt increase more than on longer-term debt, you can end up with an inverted yield curve.

This can create a situation where short-term debt (which is generally viewed as less risky pays a higher yield than longer-term debt. This creates less incentive to lend money for a longer time period—the additional risk isn’t being compensated with higher yields.

While higher yields on short-term debt can create opportunity (for instance, cash-equivalent products may offer attractive returns), an inverted yield curve tends to signal economic trouble. It can indicate a disconnect between the perceived risk and reward of long-term investments in growth; it may also indicate that investors will hold off on making longer-term investments until economic conditions feel more predictable.

Taken in this light, you may start to see why an inverted yield curve has preceded every major recession in the U.S. since the 50s.

There is a catch, however. Just because inverted yield curves are a good predictor of economic trouble, they can’t predict the severity of the economic reaction or the timing of it.

Consider this: The yield curve inverted in 2006, a full three years before the economy officially entered a recession in 2009, in the wake of the financial crisis. Another significant yield curve inversion? The late 1970s when Paul Volcker’s Fed raised rates aggressively to combat inflation.

The yield curve post-COVID 19

More recently, the yield curve inverted in July 2022 and stayed largely inverted through the end of 2024. We haven’t yet experienced a recession. Does that mean we’re due for a downturn, or that the yield curve is no longer serving as an accurate indicator?

The answer may be: It depends. Some experts think we did experience a mild recession in 2022, as initial GDP reports showed two quarters of contraction. However, the government body in charge of officially declaring a recession—the National Bureau of Economic Analysis—did not count it as such. Retrospectively, this makes sense; later revisions to GDP showed the slowdown wasn’t as significant as first readings suggested.

However, we have continued to see economic uncertainty. The economy contracted in the first quarter of 2025. The situation seems to have corrected itself—the economy grew again in the second and third quarter.

Still, there are reasons to keep an eye on the factors that tend to contribute to a recession, such as the job market, which is starting to show signs of weakness.

Ultimately, we won’t know whether the inverted yield curve we’ve seen on and off over the past three years was a harbinger of economic trouble for quite some time. In a more practical sense, it can help us spot opportunities for our clients (such as the potential to generate higher returns on cash equivalents), and it serves as a helpful input as we continually evaluate the health of various markets and the economy overall.

If you have questions about interest rates, yield, or general economic outlook, subscribe to our newsletter or request an appointment.

Disclosure

This material is for general information only and is not intended to provide specific advice or recommendations for any individual. There is no assurance the views or strategies discussed are suitable for all investors or will yield positive outcomes. Investing involves risks including possible loss of principal. Any company names noted herein are for educational purposes only.

All information is believed to be from reliable sources; however we make no representation as to its completeness or accuracy. All economic and performance data is historical and not indicative of future results. Market indices discussed are unmanaged. Investors cannot invest in unmanaged indices. Additional risks are associated with international investing, such as currency fluctuations, political and economic instability and differences in accounting standards.

Investing in securities in emerging markets involves special risks due to specific factors such as increased volatility, currency fluctuations and differences in auditing and other financial standards. Securities in emerging markets are volatile and can decline significantly in response to adverse issuer, political, regulatory, market, or economic developments.

An index is a statistical measure of change in an economy or a securities market. In the case of financial markets, an index is an imaginary portfolio of securities representing a particular market or a portion of it. Each index has its own calculation methodology and is usually expressed in terms of a change from a base value. Thus, the percentage change is more important than the actual numeric value. An investment cannot be made directly into an index.

Investing in fixed income securities involves credit and interest rate risk. When interest rates rise, bond prices generally fall. Investing in commodities may involve greater volatility and is not suitable for all investors. Investing in a non-diversified fund that concentrates holdings into fewer securities or industries involves greater risk than investing in a more diversified fund. The equity securities of small companies may not be traded as often as equity securities of large companies so they may be difficult or impossible to sell. Neither diversification nor asset allocation assure a profit or protect against a loss in declining markets. Past performance is not an indicator of future results.

Financial Planning offered through Reason Financial, a state Registered Investment Advisor. Investment advice offered through Merit Financial Group, LLC an SEC Registered Investment Advisor. Merit Financial Group and Reason Financial are separate entities. Tax related services offered through Reason Tax Group. Reason Tax Group is a separate legal entity and not affiliated with Merit Financial Group, LLC. Sean P. Storck CA Insurance Lic#OF25995 and Steven W. Pollock CA Insurance Lic#OE98073

Copyright © 2026 Reason Financial all rights reserved.

Continue Reading

2nd Quarter 2026 – Economic and Market Update

Q1 2026 in review: oil shock, S&P 500 down 4.3%, commodities up 24.4%, the cease-fire that became a blockade — and the planning moves that matter most coming out of a quarter like this one.

It’s Now More Common To Have A Baby In Your Thirties Than In Your Twenties

DisclosureThis material is for general information only and is not intended to provide specific advice or recommendations for any individual.…

When Does Refinancing Actually Make Sense? A 2026 Reality Check

If you locked in a mortgage at 7% or higher in 2023 or 2024, you’ve probably been watching rates with…