When Does Refinancing Actually Make Sense? A 2026 Reality Check

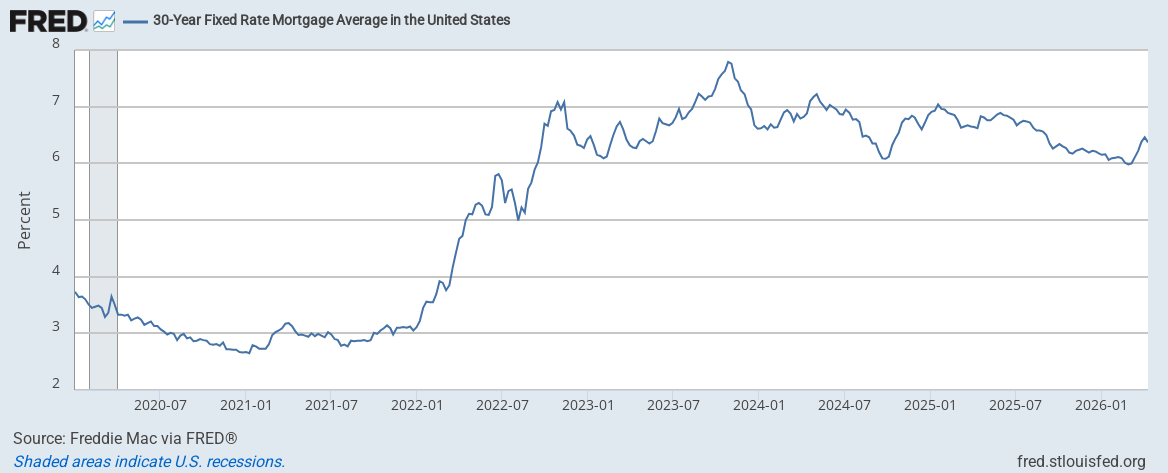

If you locked in a mortgage at 7% or higher in 2023 or 2024, you’ve probably been watching rates with one eye open for a while now. Thirty-year fixed rates have settled into the low 6% range. Freddie Mac’s weekly average hit 6.23% as of April 23, 2026, down from 6.30% the prior week. That’s not a 3% pandemic-era rate, but it is meaningfully lower than what many recent buyers are paying.

Rates have dropped. The real question is whether the drop is enough to justify the cost of refinancing for your situation.

Source: Freddie Mac via FRED. After bottoming near 2.65% in early 2021, rates surged past 7% in 2022–2023 before settling into the low 6% range heading into 2026.

The Math

The old rule of thumb, wait for a full percentage point drop, ignores the variables that matter most: your loan balance, your closing costs, and how long you plan to stay in the home.

The real calculation is the break-even point: total closing costs divided by your monthly payment savings. If you’re going to be in the home longer than that break-even period, the refinance pays for itself.

Here’s what that looks like in practice for a San Diego homeowner:

Scenario: $750,000 loan balance, refinancing from 7.25% to 6.25%

- Current monthly payment (P&I): $5,116

- New monthly payment at 6.25%: $4,619

- Monthly savings: $497

- Typical closing costs (2.5% of loan): ~$18,750

- Break-even: 38 months (just over 3 years)

That’s a meaningful payoff if you’re staying put. But bump that rate down to only 6.5% and the monthly savings drop to about $260, pushing break-even past 6 years.

Scenario: $500,000 loan, refinancing from 6.875% to 6.125%

- Monthly savings: ~$260

- Closing costs (~2.5%): ~$12,500

- Break-even: 48 months (4 years)

A 0.75% rate drop on a smaller loan still works, but the timeline stretches. Loan size matters as much as the rate gap.

Break-even months = closing costs ÷ monthly savings. Stay past that point and the refinance pays for itself.

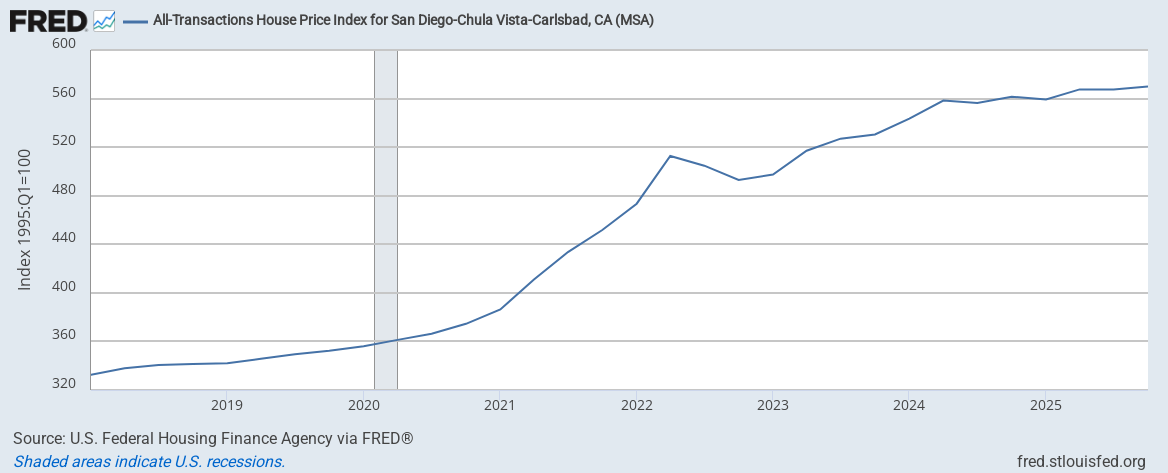

San Diego home values have nearly doubled since 2018, meaning many homeowners are sitting on significant equity. Source: U.S. Federal Housing Finance Agency via FRED.

Putting It All Together

The play for 2026:

- Run your break-even calculation using current rates. If you’re at 7%+ and can get into the low 6% range, the monthly savings likely justify the closing costs within 3–4 years.

- Consider a no-closing-cost refinance if you’re unsure about your timeline. Some lenders will roll fees into the loan or bump your rate by 0.125%–0.25% in exchange for zero out-of-pocket closing costs.

- Don’t forget about cash-out options. If you’ve built equity and have higher-rate debt elsewhere, a cash-out refinance at 6.25% can consolidate that debt at a fraction of the rate.

When to Hold Off

Wait if:

- Your rate gap is under 0.5%. The savings likely won’t outpace closing costs in a reasonable timeframe unless your loan balance is very large.

- You’re planning to move within 2–3 years. You won’t reach break-even.

- Your loan balance is under $200,000. The absolute dollar savings may not justify the effort.

- You have less than 10 years remaining. Refinancing into a new 30-year loan resets your amortization clock, which can cost you more in total interest.

What to Do Next

Pull your most recent mortgage statement and note your current rate, remaining balance, and remaining term. Then talk to your advisor about whether the numbers work for your situation.

If you have questions about whether refinancing fits your plan, reach out. We’re happy to run the numbers with you.

Sources: Freddie Mac Primary Mortgage Market Survey (April 9, 2026); National Association of Realtors; San Diego County Tax Collector.

This material is for general information only and is not intended to provide specific advice or recommendations for any individual. There is no assurance the views or strategies discussed are suitable for all investors or will yield positive outcomes. Investing involves risks including possible loss of principal. Any company names noted herein are for educational purposes only.

All information is believed to be from reliable sources; however we make no representation as to its completeness or accuracy. All economic and performance data is historical and not indicative of future results. Market indices discussed are unmanaged. Investors cannot invest in unmanaged indices. Additional risks are associated with international investing, such as currency fluctuations, political and economic instability and differences in accounting standards.

Investing in securities in emerging markets involves special risks due to specific factors such as increased volatility, currency fluctuations and differences in auditing and other financial standards. Securities in emerging markets are volatile and can decline significantly in response to adverse issuer, political, regulatory, market, or economic developments.

An index is a statistical measure of change in an economy or a securities market. In the case of financial markets, an index is an imaginary portfolio of securities representing a particular market or a portion of it. Each index has its own calculation methodology and is usually expressed in terms of a change from a base value. Thus, the percentage change is more important than the actual numeric value. An investment cannot be made directly into an index.

Investing in fixed income securities involves credit and interest rate risk. When interest rates rise, bond prices generally fall. Investing in commodities may involve greater volatility and is not suitable for all investors. Investing in a non-diversified fund that concentrates holdings into fewer securities or industries involves greater risk than investing in a more diversified fund. The equity securities of small companies may not be traded as often as equity securities of large companies so they may be difficult or impossible to sell. Neither diversification nor asset allocation assure a profit or protect against a loss in declining markets. Past performance is not an indicator of future results.

Financial Planning offered through Reason Financial, a state Registered Investment Advisor. Investment advice offered through Merit Financial Group, LLC an SEC Registered Investment Advisor. Merit Financial Group and Reason Financial are separate entities. Tax related services offered through Reason Tax Group. Reason Tax Group is a separate legal entity and not affiliated with Merit Financial Group, LLC. Sean P. Storck CA Insurance Lic#OF25995 and Steven W. Pollock CA Insurance Lic#OE98073

Copyright © 2026 Reason Financial all rights reserved.

Disclosure

This material is for general information only and is not intended to provide specific advice or recommendations for any individual. There is no assurance the views or strategies discussed are suitable for all investors or will yield positive outcomes. Investing involves risks including possible loss of principal. Any company names noted herein are for educational purposes only.

All information is believed to be from reliable sources; however we make no representation as to its completeness or accuracy. All economic and performance data is historical and not indicative of future results. Market indices discussed are unmanaged. Investors cannot invest in unmanaged indices. Additional risks are associated with international investing, such as currency fluctuations, political and economic instability and differences in accounting standards.

Investing in securities in emerging markets involves special risks due to specific factors such as increased volatility, currency fluctuations and differences in auditing and other financial standards. Securities in emerging markets are volatile and can decline significantly in response to adverse issuer, political, regulatory, market, or economic developments.

An index is a statistical measure of change in an economy or a securities market. In the case of financial markets, an index is an imaginary portfolio of securities representing a particular market or a portion of it. Each index has its own calculation methodology and is usually expressed in terms of a change from a base value. Thus, the percentage change is more important than the actual numeric value. An investment cannot be made directly into an index.

Investing in fixed income securities involves credit and interest rate risk. When interest rates rise, bond prices generally fall. Investing in commodities may involve greater volatility and is not suitable for all investors. Investing in a non-diversified fund that concentrates holdings into fewer securities or industries involves greater risk than investing in a more diversified fund. The equity securities of small companies may not be traded as often as equity securities of large companies so they may be difficult or impossible to sell. Neither diversification nor asset allocation assure a profit or protect against a loss in declining markets. Past performance is not an indicator of future results.

Financial Planning offered through Reason Financial, a state Registered Investment Advisor. Investment advice offered through Merit Financial Group, LLC an SEC Registered Investment Advisor. Merit Financial Group and Reason Financial are separate entities. Tax related services offered through Reason Tax Group. Reason Tax Group is a separate legal entity and not affiliated with Merit Financial Group, LLC. Sean P. Storck CA Insurance Lic#OF25995 and Steven W. Pollock CA Insurance Lic#OE98073

Copyright © 2026 Reason Financial all rights reserved.

Continue Reading

2nd Quarter 2026 – Economic and Market Update

Q1 2026 in review: oil shock, S&P 500 down 4.3%, commodities up 24.4%, the cease-fire that became a blockade — and the planning moves that matter most coming out of a quarter like this one.

It’s Now More Common To Have A Baby In Your Thirties Than In Your Twenties

DisclosureThis material is for general information only and is not intended to provide specific advice or recommendations for any individual.…

Robot Umps, Cap Taps, and the New Game Within the Game

By Team Reason | Reason Financial & Tax If you’ve watched a baseball game this season you’ve noticed something new.…