April 2020 – An Economic and Market Update

Executive Summary

- Stock markets plummeted, the global economy came to a screeching halt, and the government gave out a LOT of money.

- There has been a lot of activity in our portfolios as we have performed ongoing rebalancing and tax-loss harvesting.

- There are financial strategies, such as a Roth Conversion, for if this shutdown lasts longer than anticipated.

- The way back is complicated and a pessimistic consumer is the greatest danger we see ahead.

Looking Back

The start of the year began with news out of China regarding a virus that most people likely felt a sense of ambivalence towards. After all, a variety of viruses have popped up in various places over the last 20 years causing problems, but with no real effect on the daily cadence of life here in the U.S. (Bird Flu, Swine Flu, Zika, MERS, SARS, Ebola). Fast forward to April and our lives have been put on hold as we enter our second month of stay-at-home orders.

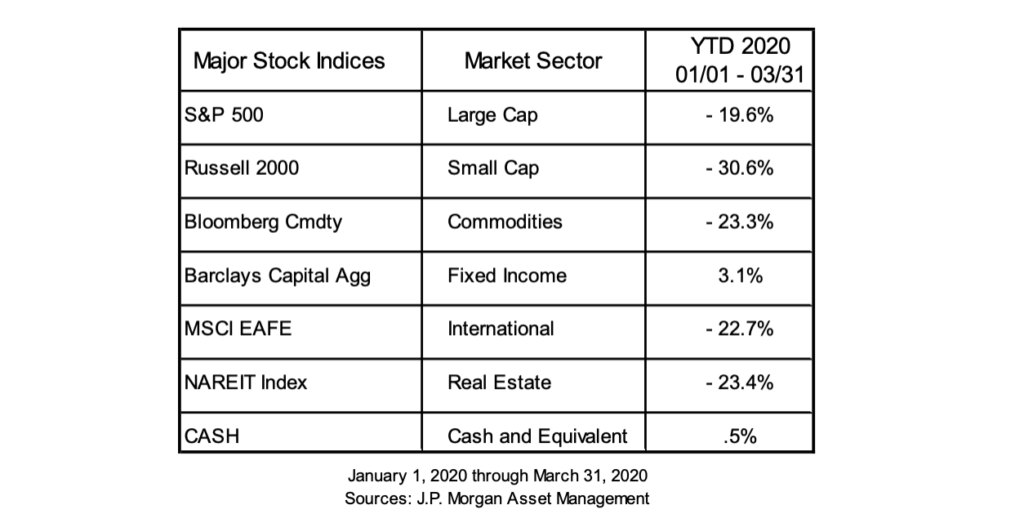

The markets remained relatively optimistic this virus would abate up until the moment Italy was hit hard and lockdowns began. At that point, the reality of a global economic shutdown became clear and the markets tumbled. It has not been pretty with the nadir (so far) of the market occurring in mid-March with the S&P 500 down 34%. The gray line in the graph below is the S&P 500, and the purple line is the MSCI All Country index of stocks representing international markets.

Guide to the Markets – U.S. Data are as of March 31, 2020

A coordinated global monetary response provided a boost by shoring up the financial system to avert a financial crisis like 2008/09. This was necessary as investment grade core bonds were beginning to show signs of stress, a problem when they are supposed to be the guardrails of a diversified portfolio. These actions were followed by large fiscal policy responses to help households and businesses.

The CARES Act and its corollary programs such as the enhanced unemployment benefits, Paycheck Protection Program (PPP), Economic Injury Disaster Loan (EIDL), tax filing relief, et al are the U.S. version of what many of the worlds governments are doing to help their citizens make it through the shutdowns. From a stabilization perspective, this appears to be working with the S&P 500 recovering roughly 25% from the bottom.

What Is Ahead And What Are We Doing

In some respects, it feels superfluous writing an economic update at a time when the future trajectory of the economy is tied to such a vague concept as the timetable of a vaccination arriving on the scene. The very limited economic statement by the Federal Reserve recently, relative to the standard lengthy press conferences and research releases, makes us feel like we are not alone in this sentiment.

As an example of how strange a time it is, the public health enemy of the last several decades, smoking, is getting a turn in the sun with some speculative analysis suggesting it may help protect against Coronavirus. Speculation is not what we would prefer to base our lives upon, financial or otherwise.

Our path forward may be clouded, but the actions we take to maintain client portfolios is not. We are engaging in a variety of active strategies to keep all portfolios as best prepared for the coming recovery as possible. You will likely have noticed a significant number of trade confirmations the last couple of months as we navigated the crisis.

- Active rebalancing – anytime there is a significant market shift up or down we will be placing trades to keep all risk tolerance levels where they should be. In a down market this means selling out of bonds and buying equities when they are on sale. Conversely, in an up market this means selling out of equities and buying bonds. This should help us recover faster when there is a clear path forward for global economic activity to resume.

- Tax-loss harvesting – this is where we are actively taking losses and initiating new positions to offset current and future gains. This increases the tax efficiency of an investment portfolio over time. The abrupt market downturn has made it a fortuitous time to engage in this strategy.

- Protected cash – maintaining cash in an account above and beyond what is typically recommended in order to ensure there is a smart place to access capital when you need it. This allows us to avoid selling into a down market to meet distribution needs.

Market volatility is not fun, but it is manageable with discipline. If you have any questions regarding the application of these strategies in your portfolio(s) please do not hesitate to ask.

Consumer Confidence

The confidence of the consumer will be key to returning to some semblance of a normal market environment in the United States as nearly 2/3 of GDP is generated by consumption. Consumer confidence is (typically) a multivariable matter, meaning there is no single input that makes it tick. Wages, employment, inflation, politics and other factors make up a broad measurement of the level of optimism we collectively have as a society toward our saving and spending decisions. In the graph below you can see that prior to the pandemic, confidence was at historically high levels. The data is likely outdated as it does not capture the full scope of the lockdowns around the country after March 31. The black line represents OECD countries and the red line is the United States.

It is not hard to imagine that the single biggest bump in spirits would be for a successful vaccine to be announced tomorrow. However, with an expected timeline of at least a year to a year and a half before a vaccine is delivered to the marketplace this pushes our timeline out to two years or more before there is widespread dispersal of a vaccine. Our expectations are for some measure of social distancing to remain in place during the interim. This will be a drag on consumption, with the likely effect of slowing the economic recovery as we all lack confidence in a full return to life as normal.

As a trivial tidbit, the fastest vaccination to market, prior to what is being attempted right now, was for mumps. A recent National Geographic article documenting the current efforts to find a cure for COVID-19 stated that, “The mumps vaccine – considered the fastest ever approved – took four years to go from collecting viral samples to licensing a drug in 1967.”

As the consumer goes, so too does the producer. After all, those who provide the goods and services must have many customers to provide them to and for. In the simplest sense, imagine a neighborhood lemonade stand.

Every weekend Little Jane sets up her lemonade stand knowing that Mr. Smith and dozens of other neighborhood residents will come to purchase lemonade. However, under social-distancing guidelines and the general unease about the current situation most people are staying home. Little Jane will sell less lemonade as a result. Even though Mr. Smith is sitting at home on a beautiful hot day saying to himself that nothing would be better than a nice ice-cold glass of lemonade from Little Jane’s Lemonade Stand, he does not go out. Little Jane sells less lemonade as a result, requiring less lemons to juice, which means Little Johnny must be let go since Little Jane can handle the reduced volume on her own. The producer of the lemons sells less lemons to all the Little Jane Lemonade stands of the world, lays off some or all of his farmhands, and dumps his stock of unused lemons to rot in the middle of an orchard somewhere. Less lemonade also means less cups needed, less ice and water used, and less sugar to sweeten all that lemonade. The entire lemonade stand supply chain is impacted and shrinks. Finally, Little Jane shuts down, not sure if or when she will be able to reopen again.

Producers and service providers are going through this calculus right now and it is not pretty. The various programs announced by Congress and the Federal Reserve will help to keep things going for a time. However, the assessment acquired by reading the most recent Federal Reserve Beige Book – Summary of Commentary on Current Economic Conditions, is that “All Districts reported highly uncertain outlooks among business contacts, with most expecting conditions to worsen in the next several months.”

All in all, it is a highly uncertain time. We believe very firmly that we will recover from this just like we have recovered from all other shocks of the past. However, we urge caution as we navigate the recovery. It will likely take more time than we would like for a full recovery to occur. Spending and purchasing decisions should be made wisely with an assumption that we will see a solution to the virus in the intermediate-term, not the short-term.

The Planning Corner

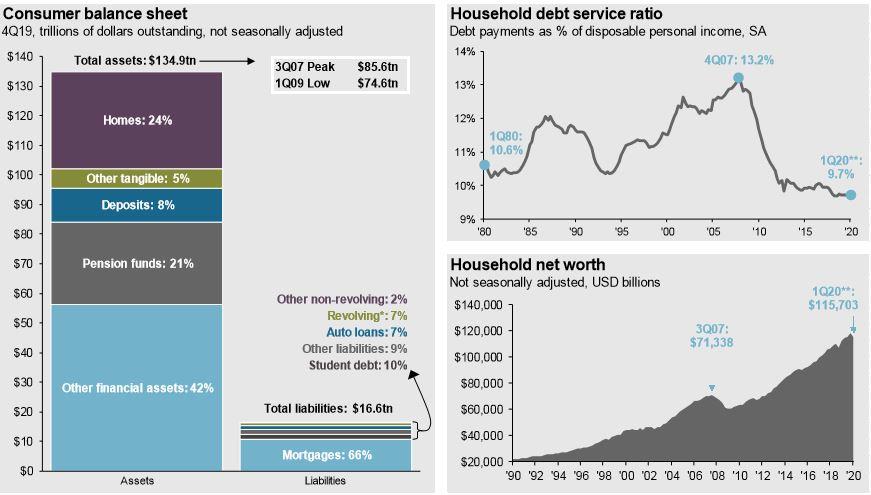

Pre-COVID the United States was in a very strong position. The average household was doing well and experiencing improvements to their financial well-being. As evidenced below, net worth was rising, and debt-servicing was as low as it had been in decades.

One of the hardest things we are all having to do right now is to change behavior after having a relatively comfortable long-term run of growth. Changing behavior is challenging. If there is a silver lining to be found it is that, in some respects, the restrictions being put on us will encourage good financial behavior. After all, it is hard to spend money on entertainment, eating out, and large purchases when it is a challenge just to leave the house. Our advice at this time is to assume that returning to the pre-Covid financial strength of the economy is going to take longer than anticipated. Match your spending decisions accordingly. Now is a better time than any to take a real look at the ways our disposable income flows out of our hands. Take stock of what matters and what does not.

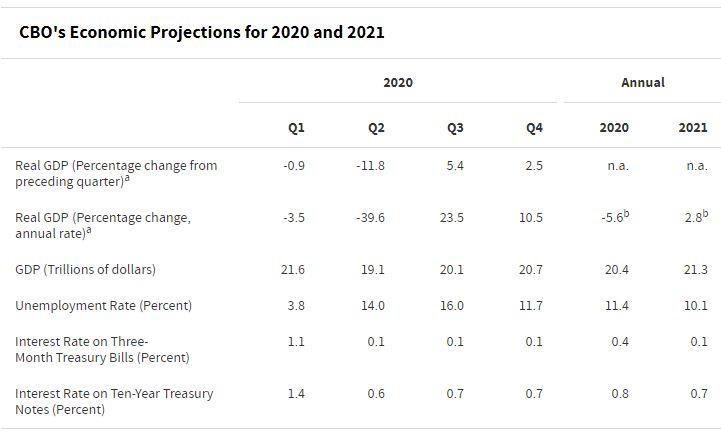

The Congressional Budget Office released their preliminary projections of economic growth for 2020/21. In the table below you can see that the projections are for real GDP to contract at an annualized rate of -39.6% in the second quarter followed by a strong rebound in the 3rd and 4th quarters. However, notice that the strong rebound does not replace what was lost, nor is it replaced by the end of 2021.

The takeaway for us is that we need to be cautiously optimistic that human inventiveness can solve this problem soon. However, in case it takes longer than anticipated we need to be prepared and have our finances are in order.

Steps you can take to begin this process:

- Assess your level of income sensitivity. If it is high, then we need to dive deeper into what can be done to insulate your finances during this time.

- Review all fixed costs and subscriptions.

- Can a mortgage be refinanced?

- Is there a cheaper alternative to the gym you are using?

- Are you paying hundreds of dollars a month to store stuff in a storage unit you have not visited in 5 years?

- Determine the most rational and cost-effective place for capital if you need it. If you are planning on assisting children or grandchildren through this time, then that needs to be planned for.

- Work on developing a financial plan or continue working on your financial plan.

- Review whether this is a good time for you to engage in a Roth Conversion strategy. The markets are down and that is usually the best time to convert from an IRA to a Roth.

Just like all of you sometimes we find ourselves wondering what day it is. A good distraction might be picking up some of those items we mentioned above, instead of checking the CA COVID-19 update page for the 452nd time. In case you have not seen it, this is a great resource:

Closing Thoughts

Our goal throughout this process has been to be as communicative as possible. We will continue to do so. Our office is technically closed to foot traffic, but we are expert users of technology. Be it a video conference, teleconference, screen-share, or secure email, we are available. It is challenging to have the mental fortitude to stick to a well-laid plan with the types of uncertainty we are facing. We are here to help you keep the long-term strategy in the forefront of your mind.

As always, we are here to help you make rational, informed and well-reasoned decisions, and we thank you for your continued trust and support. Your input is always welcome, and we ask that you contact us with any questions or concerns.

DISCLOSURE

All information is believed to be from reliable sources; however we make no representation as to its completeness or accuracy. All economic and performance data is historical and not indicative of future results. Market indices discussed are unmanaged. Investors cannot invest in unmanaged indices. Additional risks are associated with international investing, such as currency fluctuations, political and economic instability and differences in accounting standards.

Investing in securities in emerging markets involves special risks due to specific factors such as increased volatility, currency fluctuations and differences in auditing and other financial standards. Securities in emerging markets are volatile and can decline significantly in response to adverse issuer, political, regulatory, market, or economic developments.

An index is a statistical measure of change in an economy or a securities market. In the case of financial markets, an index is an imaginary portfolio of securities representing a particular market or a portion of it. Each index has its own calculation methodology and is usually expressed in terms of a change from a base value. Thus, the percentage change is more important than the actual numeric value. An investment cannot be made directly into an index.

Investing in fixed income securities involves credit and interest rate risk. When interest rates rise, bond prices generally fall. Investing in commodities may involve greater volatility and is not suitable for all investors. Investing in a non-diversified fund that concentrates holdings into fewer securities or industries involves greater risk than investing in a more diversified fund. The equity securities of small companies may not be traded as often as equity securities of large companies so they may be difficult or impossible to sell. Neither diversification nor asset allocation assure a profit or protect against a loss in declining markets. Past performance is not an indicator of future results.

Securities offered through Avantax Investment ServicesSM, Member FINRA, SIPC. Investment Managed Solutions (IMS) Platform programs and services offered through Avantax Advisory ServicesSM. All other investment management and financial planning services are offered through Reason Financial. Reason Financial and Avantax Advisory Services are unaffiliated entities. Placing business through Avantax Insurance AgencySM and Avantax Insurance ServicesSM. CA Insurance Sean P Storck #0F25995, Steven Pollock # 0E98073

Copyright © 2020 Reason Financial all rights reserved.

Moffitt, Mike. “French Study: Smoking May Offer Some Protection against COVID-19.” SFGate, San Francisco Chronicle, 23 Apr. 2020, www.sfgate.com/science/article/French-study-Smoking-may-offer-some-protection-15221951.php.

Akpan, Nsikan. “Why a Coronavirus Vaccine Could Take Way Longer than a Year.” National Geographic, 10 Apr. 2020, www.nationalgeographic.com/science/2020/04/why-coronavirus-vaccine-could-take-way-longer-than-a-year/#close.

“The Beige Book – Summary of Commentary on Current Economic Conditions.” Edited by Federal Reserve District, www.federalreserve.gov, Federal Reserve District, 15 Apr. 2020, www.federalreserve.gov/monetarypolicy/files/BeigeBook_20200415.pdf.

Disclosure

This material is for general information only and is not intended to provide specific advice or recommendations for any individual. There is no assurance the views or strategies discussed are suitable for all investors or will yield positive outcomes. Investing involves risks including possible loss of principal. Any company names noted herein are for educational purposes only.

All information is believed to be from reliable sources; however we make no representation as to its completeness or accuracy. All economic and performance data is historical and not indicative of future results. Market indices discussed are unmanaged. Investors cannot invest in unmanaged indices. Additional risks are associated with international investing, such as currency fluctuations, political and economic instability and differences in accounting standards.

Investing in securities in emerging markets involves special risks due to specific factors such as increased volatility, currency fluctuations and differences in auditing and other financial standards. Securities in emerging markets are volatile and can decline significantly in response to adverse issuer, political, regulatory, market, or economic developments.

An index is a statistical measure of change in an economy or a securities market. In the case of financial markets, an index is an imaginary portfolio of securities representing a particular market or a portion of it. Each index has its own calculation methodology and is usually expressed in terms of a change from a base value. Thus, the percentage change is more important than the actual numeric value. An investment cannot be made directly into an index.

Investing in fixed income securities involves credit and interest rate risk. When interest rates rise, bond prices generally fall. Investing in commodities may involve greater volatility and is not suitable for all investors. Investing in a non-diversified fund that concentrates holdings into fewer securities or industries involves greater risk than investing in a more diversified fund. The equity securities of small companies may not be traded as often as equity securities of large companies so they may be difficult or impossible to sell. Neither diversification nor asset allocation assure a profit or protect against a loss in declining markets. Past performance is not an indicator of future results.

Financial Planning offered through Reason Financial, a state Registered Investment Advisor. Investment advice offered through Merit Financial Group, LLC an SEC Registered Investment Advisor. Merit Financial Group and Reason Financial are separate entities. Tax related services offered through Reason Tax Group. Reason Tax Group is a separate legal entity and not affiliated with Merit Financial Group, LLC. Sean P. Storck CA Insurance Lic#OF25995 and Steven W. Pollock CA Insurance Lic#OE98073

Copyright © 2026 Reason Financial all rights reserved.

Continue Reading

2nd Quarter 2026 – Economic and Market Update

Q1 2026 in review: oil shock, S&P 500 down 4.3%, commodities up 24.4%, the cease-fire that became a blockade — and the planning moves that matter most coming out of a quarter like this one.

It’s Now More Common To Have A Baby In Your Thirties Than In Your Twenties

DisclosureThis material is for general information only and is not intended to provide specific advice or recommendations for any individual.…

When Does Refinancing Actually Make Sense? A 2026 Reality Check

If you locked in a mortgage at 7% or higher in 2023 or 2024, you’ve probably been watching rates with…