April 2022 – Economic and Market Update

Executive Summary

- Common sense discussions around inflation are starting to take place, but the voices are still out in the wilderness. Market performance during times of high inflation (4.4% – 10%) is vastly different from periods of severe inflation ( >10%).

- The SECURE Act 2.0 has passed the House. The final bill is not yet here, but anyone turning 72 in ’22 should take notice.

- Market volatility creates the perfect opportunity to look at a Roth conversion strategy.

What a year so far. It has been up and down, with mostly downs. The market bears are out in full force and the headwinds feel like a windstorm not a breeze. The only positive performing asset class to date is commodities, with all other major asset classes posting losses. The big news from last year carried over, inflation and Fed rate hikes, and the war in Ukraine burst on the scene making things worse. A slew of headline risk items made the rounds with mortgage rates posting their largest increase in a long time, if ever, the inversion of interest rates at the short end of the scale, and constant talk by technical analysis

market gurus of the dreaded death crossi (short-term market averages crossing below the 50-day and 200-day moving averages).

We have continued to move more conservative during this turmoil while also recognizing bad news does not necessarilly beget a bad market. For example, while imperfect as a recession forecaster, rate inversion, lags a recession by an average of 18 months. Meaning the market typically peaks long after a rate inversion, followed by a recession, when one occurs. The most important thing to do right now is to make sure your assets are managed appropriately for your phase of life.

WAITING TO EXHALE

“Skepticism is the chastity of the intellect.” – George Santayana

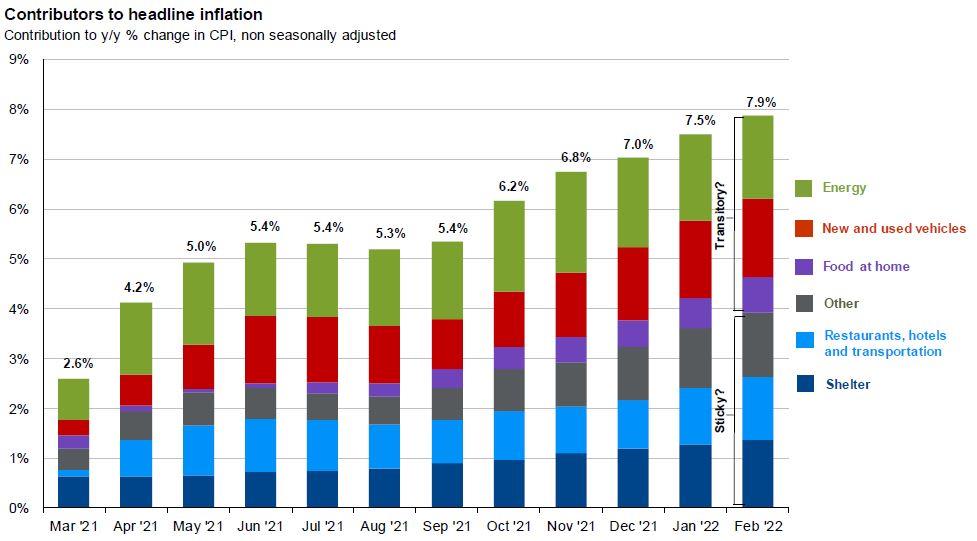

Everyone has a take on solving the problems facing the economy right now, but this aphorism from the philosopher Santayana seems appropriate for the current climate. There are a lot of proposals and thoughts, but none of them are generating warm and fuzzy feelings. Inflation has now reached 8.5% based on the March 2022 reading, and there are predictions we have reached peak inflation. The graph below does not include March, but it does breakdown the components of inflation which is useful.ii

The debate on whether or not inflation is transitory has settled – it’s not. However, there are components of inflation which may be more or less transitory as indicated in the previous graph. Energy prices, vehicles, and grocery store prices are more volatile and may work themselves out as opposed to stickier items such as the cost of housing. We will look at one issue and the popularly blamed culprit (skepticism warning in advance), vehicle prices and chip shortages, and then introduce a theory from a British economist.

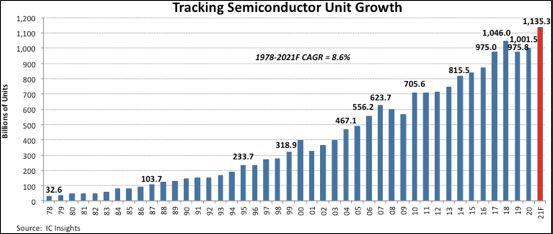

The chip shortage has been talked about a lot, particularly as it relates to automobiles. The war in Ukraine will likely put additional intermediate-term pressure on this problem. Neon gas is a key component of chip manufacturing with roughly half of the world’s neon gas supply sourced in Ukraine. After the annexation of Crimea by Russia in 2014, chip manufacturers began to diversify where their neon was sourced in addition to stockpiling the resource. It is estimated that suppliers and semiconductor manufacturers have somewhere between 3 and 12 months of supply on hand. This is not going to help alleviate the current problem, but it may help avoid exacerbation of the issue due to the war. iii

The big issue is that demand has skyrocketed and manufacturing cannot keep up. As seen below, semiconductor unit growth is the highest it has ever been. In a world seemingly bent on putting tech wherever tech can go, there is an insatiable demand for integrated circuits. We are in the market for a new fridge and were recently “wowed” by the ability to touch the door and have the front of the fridge turn transparent and the light turn on. Apparently, being able to see what is in the fridge without opening it is a need we never knew we had. Leftovers never looked so good.

From the headlines one would assume that chip manufacturing was down, not up, with record units produced and shipped as you can see by the red bar in the preceding graph. Digital connectivity has made integrated circuits ubiquitous and the continued arc of technology adoption across the board will make this worse, not better. Manufacturing will catch up, we just don’t know when. We are skeptical this will work itself out in the timeframe necessary to warrant the label of “transitory”.

Charles Goodhart, an economist and former U.K. central banker, made a prediction in 2020 that the world was in for a prolonged period of higher inflation. “The coronavirus pandemic will mark the dividing line between the deflationary forces of the last 30 to 40 years and the resurgent inflation of the next two decades.”iv

His reasoning was based on demographic changes and the squeezing of the global supply of cheap labor. With projected declining global populations and the rapid move of large numbers of global citizens into the ranks of the middle class, Goodhart hypothesizes that cheap labor is a thing of the past.

At this point, Goodhart is in the minority speculating higher long-term inflation is something we will all have to get used to. However, at least some central banking officials are getting the message. Isabel Schnabel of the European Central Bank recently said, “I take the things Charles says very seriously. Charles wants to alert us that we shouldn’t take for granted that the world ahead of us is going to look

the same as it did in the recent past”. As the Federal Reserve continues to pivot on their language concerning transitory versus sticky/entrenched/persistent inflation, labor force participation continues to lag pre-COVID levels, making Goodhart’s theory a rational analysis.

What to do

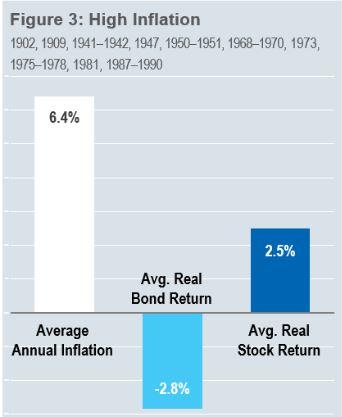

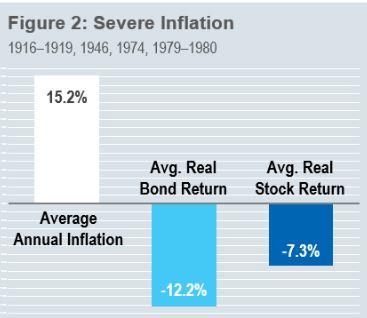

In 2011 a research company, O’Shaughnessy Asset Management, delved into market performance during various inflationary periods. They broke inflation down into several categories; severe, high, target/moderate, low, and deflation. High inflation was defined as anything between 4.4% and 10%, which is the current environment we are in. Up to 2011 there were 20 years going back to the year 1900 where the United States experienced high inflation.v

So what do we do if we think inflation is going to continue being a problem and markets are going to respond? What actions should be taken to protect against market volatility? First is to not abandon investing in general, based on the graph above. Average real stock returns in the face of high inflation are not extraordinary, but they are still positive. This is better than cash and better than bonds. What we

do know is that growth focused stocks tend to perform worse in inflationary environments with rising interest rates. To that point, we have continued to reduce our exposure to growth and reduce our exposure to high duration bonds.

The real tricky business is when/if we see severe inflation at rates of 10% or higher. Historically, markets have fared much worse during these time frames.

As you can see, there are not a lot of data points for severe inflationary periods. We are looking at 8 years out of the last 121. However, markets performed very poorly during those stretches with the most recent being in the late ‘70s. It is important to remember that we are looking at smoke right now, but as of yet, there is no fire. There is positive news regarding supply chain disruption issues. Ports have cleared much of the backlog and are moving substantially more freight than even pre-COVID days. Employment is strong across the board. Corporate earnings are expected to be strong this earnings season, except for Netflix. So lots of news that gives us some hope that the smoke will clear and a fire will not start.

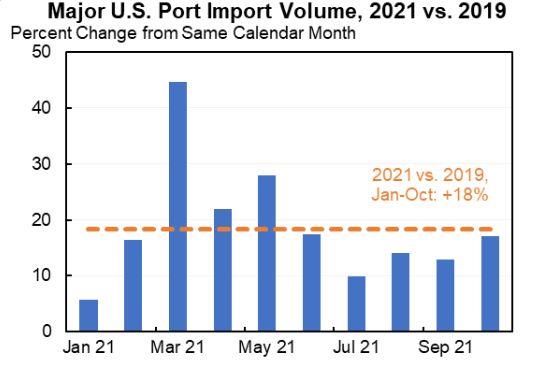

The graph below is courtesy of Professor Jason Furman, former chair of President Obama’s Council of Economic Advisors. He makes a strong case in a recent article published in Project Syndicate that the inflation we are seeing today is demand-push inflation, as opposed to supply-pull inflation which has been

the prevailing theory of the last year. One of his major points is clear from the graph. Goods are moving at levels far above pre-COVID levels. It is time to stop making this about supply and instead focus on demand. The fact that a prominent economist not associated with the current administration, or the last, is making the case for taking inflation seriously is heartening. Hopefully, consensus will continue to build towards a rational and informed approach to combating the current situation.

George Santayana is aso the originator of another useful aphorism, “Those who cannot remember the past are condemned to repeat it”. Denying the progenitor of today’s inflation is a recipe to return to prior severe inflation periods and the strongly negative outcomes therewith. We do not expect this to be the outcome as we see refreshing voices of reason chiming in to ring the alarm bells. To reiterate, under current inflation readings and based on historical data, stocks are a productive and useful hedge against inflation. If that changes, we will promptly communicate our forward strategy.

SECURE ACT 2.0 – AN UPDATE

For almost a year now we have been anticipating the passage of the next version of the SECURE (Securing A Strong Retirement) Act. This bill has finally passed the House of Representatives and moved on to the Senate after being stuck in purgatory behind the failed Build Back Better legislation.vi

As the rules are finalized we will provide an update with the key aspects of the bill. The most consequential proposal for current retirees is to raise the RMD (Required Minimum Distribution) age. In the first SECURE Act, the RMD age was raised from 70.5 to 72. The current proposal is set to raise the RMD age to 75 in a stepped phase-in, with a year added to the current RMD at different points over the next decade. For everyone turning 72 in 2022, this means we will likely need to get RMDs started as you will fall outside the framework as currently proposed. Upon passage of the law by the Senate we will begin individually contacting clients with the best strategy to ensure efficient taxation and full compliance.

For current savers, there are a variety of improvements to the retirement savings rules. One being automatic enrollment requirements in employer-sponsored retirement plans. For years economists have advocated automatic enrollment and auto-increase provisions for retirement plan participants. The hypothesis is that most people save if it is done automatically and requires an opt-out to not save, versus an opt-in to save. It appears this may finally be happening.

If you are a parent supporting a young adult starting out in life there is an improved Savers Credit to look at. In short, if you are low income the government will provide a tax credit of up to 50% of your retirement contribution, capped at $1,000 or $2,000 depending on filing status and income. This credit would go to the filer – your child. If you help subsidize your child’s life while they are starting out, the best way to do so could very well be to assist in funding a retirement account for them. Not only will it help prepare them for the future, but they may be able to obtain a significant tax credit.

Hopefully, we will have a final bill to mull over later this summer. The recent iteration passed with strong bipartisan support of 414-5, leading to strong expectations of the bill being written into law soon. There are no controversial proposals in this legislation, unlike the last bill which included major changes to stretch IRA provisions. Our expectation is for minor tweaks to the version which passed the House.

THE PLANNING CORNER

Market volatility is here and it is not fun. However, it is the perfect time to start looking at the appropriateness of a Roth Conversion. Down markets provide the best opportunity to convert IRA dollars to Roth dollars as a future market rebound will magnify the value of the conversion in the long run. Converting at a market peak is never fun as you pay taxes on the conversion and a downturn means the value of your account is quickly below the amount you paid taxes on.

Now is the time to put together a tax plan and conversion strategy. There is always a lot to do when the summer hits but we recommend putting some time on the calendar for us to create a conversion strategy if it is appropriate for your circumstances.

As always, our desire is to help you make rational, informed and well-reasoned decisions, and we thank you for your continued trust and support. Your input is always welcome and we ask that you contact us with any questions or concerns.

DISCLOSURE

All information is believed to be from reliable sources; however we make no representation as to its completeness or accuracy. All economic and performance data is historical and not indicative of future results. Market indices discussed are unmanaged. Investors cannot invest in unmanaged indices. Additional risks are associated with international investing, such as currency fluctuations, political and economic instability and differences in accounting standards.

Investing in securities in emerging markets involves special risks due to specific factors such as increased volatility, currency fluctuations and differences in auditing and other financial standards. Securities in emerging markets are volatile and can decline significantly in response to adverse issuer, political, regulatory, market, or economic developments.

An index is a statistical measure of change in an economy or a securities market. In the case of financial markets, an index is an imaginary portfolio of securities representing a particular market or a portion of it. Each index has its own calculation methodology and is usually expressed in terms of a change from a base value. Thus, the percentage change is more important than the actual numeric value. An investment cannot be made directly into an index.

Investing in fixed income securities involves credit and interest rate risk. When interest rates rise, bond prices generally fall. Investing in commodities may involve greater volatility and is not suitable for all investors. Investing in a non-diversified fund that concentrates holdings into fewer securities or industries involves greater risk than investing in a more diversified fund. The equity securities of small companies may not be traded as often as equity securities of large companies so they may be difficult or impossible to sell. Neither diversification nor asset allocation assure a profit or protect against a loss in declining markets. Past performance is not an indicator of future results.

Sean P. Storck and Steven W. Pollock are registered representatives with and securities and Retirement Plan Consulting Program advisory services offered through LPL Financial, a Registered Investment Advisor. Member FINRA/SIPC. Financial Planning offered through Reason Financial, a state Registered Investment Advisor. Investment advice offered through Merit Financial Group, LLC an SEC Registered Investment Advisor. Merit Financial Group and Reason Financial are separate entities from LPL Financial. Tax related services offered through Reason Tax Group. Reason Tax Group is a separate legal entity and not affiliated with LPL Financial. LPL Financial does not offer tax advice or tax related services. Sean P. Storck CA Insurance Lic#OF25995 and Steven W. Pollock CA Insurance Lic#OE98073

Copyright © 2021 Reason Financial all rights reserved.

i Chen, James. “What Is a Death Cross?” Investopedia, Investopedia, 16 Mar. 2022, https://www.investopedia.com/terms/d/deathcross.asp.

ii Published by Statista Research Department, and Apr 25. “United States – Monthly Inflation Rate March 2021/22.” Statista, 25 Apr. 2022, https://www.statista.com/statistics/273418/unadjusted-monthly-inflation-rate-in-the-us/#:~:text=The%20change%20in%20this%20price,has%20weakened%20in%20recent%20years.

iii Shead, Sam. “Chip Industry under Threat with Neon Production Set to Fall off a Cliff Following Russia’s Invasion of Ukraine.” CNBC, CNBC, 25 Mar. 2022, https://www.cnbc.com/2022/03/25/russia-ukraine-war-laser-neon-shortage-threatens-semiconductor-industry.html.

iv Fairless, Tom. “Will Inflation Stay High for Decades? One Influential Economist Says Yes.” The Wall Street Journal, Dow Jones & Company, 9 Mar. 2022, https://www.wsj.com/articles/inflation-high-forecast-economist-goodhart-cpi-11646837755#:~:text=He%20predicted%20that%20inflation%20in,the%20decade%20before%20the%20pandemic.

v O’Shaughnessy, Jim. “Inflation and the US Bond and Stock Markets.” Inflation and the US Bond and Stock Markets | O’Shaughnessy Asset Management, Apr. 2011, https://www.osam.com/Commentary/inflation-and-the-us-bonds-and-stock-markets#:~:text=Stocks%20do%20significantly%20better%20than,high%20inflation%20is%202.51%20percent.

vi Stewart, Jackie, and Joy Taylor. “Secure Act 2.0: 14 Ways the Proposed Law Could Change Retirement Savings.” Kiplinger, Kiplinger, 1 Apr. 2022, https://www.kiplinger.com/retirement/retirement-plans/602821/secure-act-2.

Disclosure

This material is for general information only and is not intended to provide specific advice or recommendations for any individual. There is no assurance the views or strategies discussed are suitable for all investors or will yield positive outcomes. Investing involves risks including possible loss of principal. Any company names noted herein are for educational purposes only.

All information is believed to be from reliable sources; however we make no representation as to its completeness or accuracy. All economic and performance data is historical and not indicative of future results. Market indices discussed are unmanaged. Investors cannot invest in unmanaged indices. Additional risks are associated with international investing, such as currency fluctuations, political and economic instability and differences in accounting standards.

Investing in securities in emerging markets involves special risks due to specific factors such as increased volatility, currency fluctuations and differences in auditing and other financial standards. Securities in emerging markets are volatile and can decline significantly in response to adverse issuer, political, regulatory, market, or economic developments.

An index is a statistical measure of change in an economy or a securities market. In the case of financial markets, an index is an imaginary portfolio of securities representing a particular market or a portion of it. Each index has its own calculation methodology and is usually expressed in terms of a change from a base value. Thus, the percentage change is more important than the actual numeric value. An investment cannot be made directly into an index.

Investing in fixed income securities involves credit and interest rate risk. When interest rates rise, bond prices generally fall. Investing in commodities may involve greater volatility and is not suitable for all investors. Investing in a non-diversified fund that concentrates holdings into fewer securities or industries involves greater risk than investing in a more diversified fund. The equity securities of small companies may not be traded as often as equity securities of large companies so they may be difficult or impossible to sell. Neither diversification nor asset allocation assure a profit or protect against a loss in declining markets. Past performance is not an indicator of future results.

Financial Planning offered through Reason Financial, a state Registered Investment Advisor. Investment advice offered through Merit Financial Group, LLC an SEC Registered Investment Advisor. Merit Financial Group and Reason Financial are separate entities. Tax related services offered through Reason Tax Group. Reason Tax Group is a separate legal entity and not affiliated with Merit Financial Group, LLC. Sean P. Storck CA Insurance Lic#OF25995 and Steven W. Pollock CA Insurance Lic#OE98073

Copyright © 2026 Reason Financial all rights reserved.

Continue Reading

2nd Quarter 2026 – Economic and Market Update

Q1 2026 in review: oil shock, S&P 500 down 4.3%, commodities up 24.4%, the cease-fire that became a blockade — and the planning moves that matter most coming out of a quarter like this one.

It’s Now More Common To Have A Baby In Your Thirties Than In Your Twenties

DisclosureThis material is for general information only and is not intended to provide specific advice or recommendations for any individual.…

When Does Refinancing Actually Make Sense? A 2026 Reality Check

If you locked in a mortgage at 7% or higher in 2023 or 2024, you’ve probably been watching rates with…