January 2020 – An Economic and Market Update

Executive Summary

- Stock indexes posted incredible gains this year, shaking off persistent fears of a global slowdown and trade wars.

- Domestic growth prospects are favorable for the time being, but there may be structural problems coming in the form of declining global populations.

- Congress passed the SECURE Act and it brings with it changes that every pre-retiree and retiree should be aware of.

- The Federal Reserve is holding course on monetary policy in a bid to keep the economic expansion rolling.

Looking Back

While the end of 2018 could best be described as the downward plunge of a rollercoaster, 2019 was the steady ascent. In surprising fashion, all major indexes posted gains with Large Cap U.S. stocks pacing the market and Real Estate Investment Trusts taking second. Concerns of a global slowdown and trade war escalation brought downturns on two occasions during the late spring and mid-summer, but otherwise, it was a year of smooth sailing. News of an imminent U.S./China trade deal helped drive the markets up from October through the end of December.

“The agreement will offer some respite to investors in financial markets, which have see-sawed, at times dramatically, as the negotiations between the two capitals have unfolded. However, US and Chinese officials have offered few clear indications on the timing and prospects for the second phase of negotiations.”

This statement from the Financial Times provides some context for why markets calmed down since the announcement of the Phase One trade deal was made. However, it also warns us to expect volatility to begin anew once uncertainty brought on by future discussions begins.

Growth Prospects

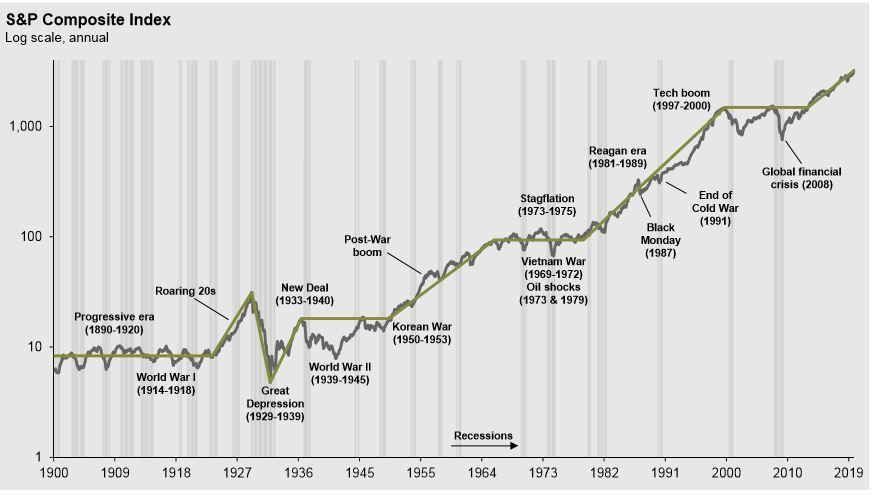

In the coming year, we expect continued strength in the United States; however, globally there will be concerns that growth is not resuming at levels necessary to pull us out of a slowing trend. For context, the S&P Composite Index since 1900 has made three significant jumps over the course of its history. We appear to be in the fourth such instance at present. It is far more complicated than just looking at a graph and saying history is going to repeat itself, but it looks like there is still room to run in a secular bull market even if we hit a recession (or three) along the way.

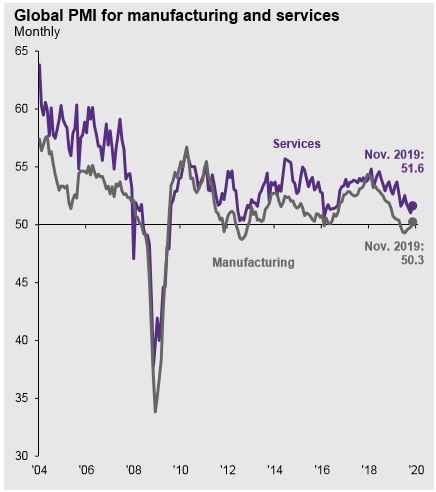

Concern about global economic conditions is warranted. For the last two years, Global PMI has been steadily dropping, although it did encouragingly creep up towards the end of 2019. This trend may be a result of traditional economic problems such as debt issues, low productivity, inflation, unemployment, and the like. It may also be something we need to start growing accustomed too.

The reason is that at some point a major structural problem is going to start hitting countries all over the world. The problem: declining population. In 1937, the economist John Maynard Keynes lectured on “Some Economic Consequences of a Declining Population”. Logically it seems easy to connect the dots that fewer people consume fewer things leading to slower growth. In his lecture he says the following, “with a stationary population we shall, I argue, be absolutely dependent for the maintenance of prosperity and civil peace on policies of increasing consumption by a more equal distribution of incomes and of forcing down the rate of interest.” So far, he nailed our current interest rate environment across the globe. He also effectively predicted the discussions we would be having ad nauseum about income inequality. A point to note is that the population demographics of the United States are superior to almost every other country in the world providing some insulation from these problems.

Our hope is that the structural problems that declining global populations create are not quite ready to roost, and instead, the relative improvement in Global PMI visible in the earlier graph is a continuing trend. If not, global growth will likely face headwinds for a very long time.

The Secure Act of 2019

SECURE stands for “Setting Every Community Up for Retirement Enhancement”. The CLIFF Notes version of the bill follows. The Act appears to be focused on three areas: widen access to 401k plans by making them easier to set up and participate in, account for an aging workforce by increasing the RMD age and removing the age limit on IRA contributions, and raise taxes by limiting the tax-deferral of Inherited IRA’s.

Diving deeper, here are the sections of the Act (bolded areas by Reason Financial):

Title I: Expanding and Preserving Retirement Savings

- Section 101. Expand Retirement Savings by Increasing the Auto Enrollment Safe Harbor Cap.

- Section 102. Simplification of Safe Harbor 401(k) Rules.

- Section 103. Increase Credit Limitation for Small Employer Pension Plan Start-Up Costs.

- Section 104. Small Employer Automatic Enrollment Credit.

- Section 105. Treat Certain Taxable Non-Tuition Fellowship and Stipend Payments as Compensation for IRA purposes.

- Section 106. Repeal of Maximum Age for Traditional IRA Contributions.

- Section 107. Qualified Employer Plans Prohibited from Making Loans through Credit Cards and Other Similar Arrangements.

- Section 108. Portability of Lifetime Income Options.

- Section 109. Treatment of Custodial Accounts on Termination of Section 403(b) Plans.

- Section 110. Clarification of Retirement Income Account Rules Relating to Church-Controlled Organizations.

- Section 111. Allowing Long-Term Part-Time Workers to Participate in 401(k) Plans

- Section 112. Penalty-free Withdrawals from Retirement Plans for Individuals in Case of Birth or Adoption.

- Section 113. Increase in Age for Required Beginning Date for Mandatory Distributions.

- Section 114. Community Newspapers Pension Funding Relief.

- Section 115. Treating Excluded Difficulty of Care Payments as Compensation for Determining Retirement Contribution Limitations.

There are a variety of provisions here which are interesting for us. Many of them are meant to spur savings by simplifying 401k rules and enhancing participation in employer-provided retirement vehicles. This is an improvement to current law as participation in a 401k plan is easier to automate than setting up an IRA for yourself. A variety of academic research studies have shown that mechanisms inside 401k plans such as auto-enrollment, auto-deferral, and auto-escalation for contributions significantly improve long-term savings results. Lowering the hurdle to establish and fund a qualified retirement account on a regular basis should improve participation in retirement savings plans over time. There is a great Ted Talk given by behavioral economist Schlomo Benartzi called, “Saving for Tomorrow, Tomorrow”, which will provide context for why we believe these changes will ultimately benefit savers. Hopefully, these changes will decrease the savings gap we have in this country by making contributions to retirement accounts easier and less confusing.

The repeal of the age limit on IRA contributions and the extension of age for Required Minimum Distributions (RMD’s) to age 72 are positive. This should help increase the viability of retirement funds for those who are currently retired or approaching retirement. There has been a lot of print spent on discussing the aging of the workforce and deferment of retirement for workers in their 60’s and 70’s. The old rules made two things challenging for those working past 70. First, workers were unable to contribute to an IRA even though they otherwise met the requirement of having earned income (wages and self-employment). Second, RMD’s sped up distributions from retirement accounts even if distributions were not required for living expenses. If you are turning 70 ½ this year please call us to discuss whether this rule impacts you or not. If you are already taking RMD’s, this does not apply to you.

Title II: Administrative Improvements

These provisions are primarily for employers and are not pertinent to the discussion at hand.

Title III: Other Benefits

- Section 301. Benefits for Volunteer Firefighters and Emergency Medical Responders.

- Section 302. Expansion of 529 Plans.

Section 302 is the most interesting for taxpayers who have 529 plans in place for their children or grandchildren. It provides for student loan repayment options which are attractive for parents who are carrying debt from helping their children through college.

Title IV: Revenue Provisions

- Section 401. Modifications to Required Minimum Distribution Rules.

- Section 402. Increase in Penalty for Failure to File.

- Section 403. Increased Penalties for Failure to File Retirement Plan Returns.

- Section 404. Increase Information Sharing to Administer Excise Taxes.

Make no mistake, these sections are meant to increase taxes.

The accounts most impacted are IRA Beneficiary Designation Accounts. This is a very specific type of IRA that has been inherited. The rules regarding non-spousal inherited IRA’s have always been a bit confusing, and we will outline some of the reasons why below.

IRA Beneficiary Designation Accounts (BDA) are required to be kept separate from any other retirement funds the inheritor may have, such as their own IRA or other retirement plans. This is because the funds are subject to special distribution rules from the onset of inheritance. The most profound of those rules allowed for a lifetime distribution scenario for the beneficiary, a strategy referred to as a Stretch IRA. This allowed the inheriting beneficiary to continue to defer taxation on the IRA except for mandatory Required Minimum Distributions every year. This rule has been updated in a big way.

Under Section 401 of the new law, titled Modification of Required Distributions Rules for Designated Beneficiaries, except in the case of ‘eligible designated beneficiaries’, the Stretch provision will no longer be allowed, and all funds must be distributed from an Inherited IRA within 10 years. An ‘eligible designated beneficiary’ is either a spouse, a child under the age of majority, or a disabled beneficiary.

The result is the advancement of taxation on inherited retirement dollars. This will be a boon for taxing agencies, but not for retirement account owners who have been planning with a now outdated rulebook. Outside of a primary residence, the largest asset most people have is their retirement account. As a result, planning for the most tax-efficient way for beneficiaries to inherit assets has been to first discuss the impacts of inheriting an IRA and how the stretch provisions made it possible for inherited assets to last for a substantial amount of time increasing tax efficiency and asset growth.

We discussed this early in 2019 as an area of possible tax law that our clients should be aware of. There was a high level of certainty that some amendments would be made to the IRA BDA as there was broad bipartisan support in Congress. Thankfully, the 10-year rule made it into law versus the 5-year rule which was originally discussed in the Senate.

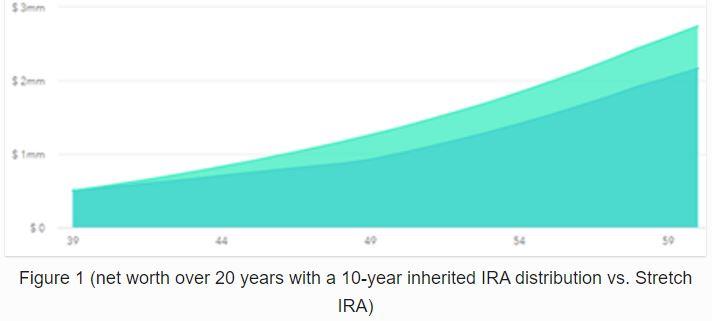

The assumptions built into the graph above are of a single person making $100,000/year inheriting a $500,000 IRA and having no other assets. The light blue represents the growth of a stretch IRA under the old rules and the darker blue represents growth under the new 10-year distribution requirements. Ultimately, the beneficiary will lose out on nearly $600,000 in asset appreciation under these assumptions. And that is only if they re-invest the after-tax distributions instead of spending them. A big benefit of the Inherited IRA stretch provision has been to disincentive profligate spending of inherited IRAs due to the tax consequences. This disincentive has been removed, making it easier to justify spending the larger distributions mandated under the new law.

This is a big change, but as an ode to a phrase we have been hearing repeatedly in the recent presidential candidate debates, we’ve got a plan for that. If your intent is to leave a large retirement account to your beneficiaries, now is as good of a time as any to start planning for how to most efficiently pass your assets to the next generation. With a long-term plan the tax consequences can be minimized in a variety of ways. Every situation will vary so it is important for us to have a discussion on the best way to minimize the impacts for you and your family.

The Fed Listens: No Really, They Do

Expectations are our beliefs about what will happen in the future. How we come by those expectations is a complicated process of taking in a breadth of knowledge and distilling down to what outcomes are likely based on what we see. A popular concern for many people, us included, is whether or not the economic expansion can continue further from where it is today. The Federal Reserve plays a strong role in shaping expectations about where the economy is and where it is headed.

In 2019, the Fed moved towards an accommodative monetary policy stance which has played a part in continuing the current expansion. Chair Powell has made a variety of comments on the reasons why.

Over the course of the last year, the Federal Reserve has hosted/sponsored a variety of conferences and opportunities for speakers and panelists to have a forum by which they can discuss the impacts of Fed policy on their particular communities. Those events have been called, “Fed Listens”, as a nod to their stepping out of the halls of academia and research to speak with people from all walks of life. The dual mandate of the Federal Reserve to maintain stable inflation and unemployment obviously reaches all of us one way or another, making these forums a valuable way to get feedback from those affected by the policy. Inflation impacts the price we pay for everything we consume. Interest rates impact how we make long-term purchasing decisions such as buying a home. Maintaining low and stable unemployment numbers assists in propelling wage growth to the benefit of all workers and keeps the highest possible number of people employed. Anecdotal evidence of the success of the current policy was reported recently by Bloomberg that for the first time in 26 years, all major U.S. metro areas experienced income gains.

In the Federal Open Market Committee meeting minutes from December, it was noted that “representatives from underserved communities who participated in the Fed Listens events generally saw the current strong labor market as providing significant benefits to their communities, most notably by creating greater opportunities for individuals who have experienced difficulty finding jobs in the past. Nevertheless, these representatives noted that the benefits from current labor market conditions flowing to people in their communities were less than those implied by national statistics, and they expressed concerns that the recent gains might not be sustained in the event of an economic downturn.”

This statement helps explain the boost of accommodative policy we received last year. Incoming data has confirmed weak inflation, positive wage growth, and both low unemployment and rising labor market participation. The impression from this data is that there is still slack in the employment market thereby allowing the Fed to push expansionary monetary policy further.

Additionally, Fed participants “generally saw the feedback from Fed Listens events as reinforcing the importance of sustaining the economic expansion so that the effects of a persistently strong job market reach more of those who, in the past, had experienced difficulty finding employment.”

The Federal Reserve is going to accommodate the continuation of this economic expansion based on their comments. The unintended consequences of this may create a bubble we have to deal with in the future, but for now, it looks like the spigot of easy money will stay open.

The Planning Corner

There is a lot to plan for in the coming years. The SECURE Act has fundamentally changed the way in which planning for tax efficiency through inherited retirement assets works. We strongly encourage everyone with assets in retirement plans to discuss with us their intent for the next generation. Tax inefficiency is real. Finding the best way to plan for how you will use the funds during your life and how those remaining funds will be used after you pass away is an important component of sound long-term financial planning.

We are here to help you make rational, informed and well-reasoned decisions, and we thank you for your continued trust and support. Your input is always welcome, and we ask that you contact us with any questions or concerns.

DISCLOSURE

All information is believed to be from reliable sources; however we make no representation as to its completeness or accuracy. All economic and performance data is historical and not indicative of future results. Market indices discussed are unmanaged. Investors cannot invest in unmanaged indices. Additional risks are associated with international investing, such as currency fluctuations, political and economic instability and differences in accounting standards.

Investing in securities in emerging markets involves special risks due to specific factors such as increased volatility, currency fluctuations and differences in auditing and other financial standards. Securities in emerging markets are volatile and can decline significantly in response to adverse issuer, political, regulatory, market, or economic developments.

An index is a statistical measure of the change in an economy or a securities market. In the case of financial markets, an index is an imaginary portfolio of securities representing a particular market or a portion of it. Each index has its own calculation methodology and is usually expressed in terms of a change from a base value. Thus, the percentage change is more important than the actual numeric value. An investment cannot be made directly into an index.

Investing in fixed income securities involves credit and interest rate risk. When interest rates rise, bond prices generally fall. Investing in commodities may involve greater volatility and is not suitable for all investors. Investing in a non-diversified fund that concentrates holdings into fewer securities or industries involves greater risk than investing in a more diversified fund. The equity securities of small companies may not be traded as often as equity securities of large companies so they may be difficult or impossible to sell. Neither diversification nor asset allocation assures a profit or protect against a loss in declining markets. Past performance is not an indicator of future results.

Securities offered through Avantax Investment ServicesSM, Member FINRA, SIPC. Investment Managed Solutions (IMS) Platform programs and services offered through Avantax Advisory ServicesSM. All other investment management and financial planning services are offered through Reason Financial. Reason Financial and Avantax Advisory Services are unaffiliated entities. Insurance services offered through 1st Global Insurance Services, Inc. CA Insurance Steven W. Pollock #OE98073, Sean P. Storck #OF25995, Nicole Albrecht #OF99962.

Copyright © 2020 Reason Financial all rights reserved.

1 Politi, James. “US and China Prepare to Seal ‘Phase One’ Trade Deal.” www.ft.com, Financial Times, 15 Jan. 2020, www.ft.com/content/eb72b49c-3714-11ea-a6d3-9a26f8c3cba4.

2 Harding, Robin. “The Costs of a Declining Population.” www.ft.com, Financial Times, 14 Jan. 2020, www.ft.com/content/c017334e-36bb-11ea-a6d3-9a26f8c3cba4.

3 Neal, Richard E. “THE SETTING EVERY COMMUNITY UP FOR RETIREMENT ENHANCEMENT ACT OF 2019 (THE SECURE ACT).” www.waysandmeans.house.gov, House Committee On Ways & Means, 2019, waysandmeans.house.gov/sites/democrats.waysandmeans.house.gov/files/documents/SECURE%20Act%20section%20by%20section.pdf.

4 Benartzi, Shlomo, director. Saving For Tomorrow, Tomorrow. TED, Ted.com, 2011, www.ted.com/talks/shlomo_benartzi_saving_for_tomorrow_tomorrow?language=en.

5 Tanzi, Alex. “For First Time in 26 Years, All U.S. Metros Enjoyed Income Gains.” Yahoo! Finance, Yahoo!, 14 Jan. 2020, ca.finance.yahoo.com/news/first-time-26-years-u-150735277.html.

6 “Minutes of the Federal Open Market Committee December 10–11, 2019.” www.FederalReserve.gov, Board of Governors of the Federal Reserve Board, 3 Jan. 2020, www.federalreserve.gov/monetarypolicy/fomccalendars.htm.

7 “Minutes of the Federal Open Market Committee December 10–11, 2019.” www.FederalReserve.gov, Board of Governors of the Federal Reserve Board, 3 Jan. 2020, www.federalreserve.gov/monetarypolicy/fomccalendars.htm.