January 2021 – Economic and Market Update

Executive Summary

- Despite all the turmoil markets ended 2020 substantially above the intra-year lows.

- It is easy to conflate politics and market performance in our minds. The reality is far more mundane with positive market performance no matter the political leadership scenario. Fiscal and monetary stimulus does influence the markets, and we have that in spades.

- Re-stocking and re-opening have the potential to unleash significant economic activity with the vaccination process.

The year finished strong with enthusiasm surrounding the rollout of the vaccine(s) and an advanced timetable for the re-opening of America, and the world, based on reaching herd immunity sooner than originally planned. There are some hiccups, one being the new strains of COVID showing up in various parts of the globe. We will discuss how this is impacting our investment strategy later. We are not anticipating as many tactical changes in the coming year as we experienced in the last 9 months. This was a record year for rebalance and fund changes for Reason Financial. However, we will continue to keep our eye on the opportunities and challenges we see ahead and adjust, as necessary.

In the meantime, 2020, while painful in many ways, is a perfect case study in why it pays to endure the downs. The graph below illustrates the intra-year low as represented by a red dot. The solid bar represents the actual performance for the year despite the intra-year low.

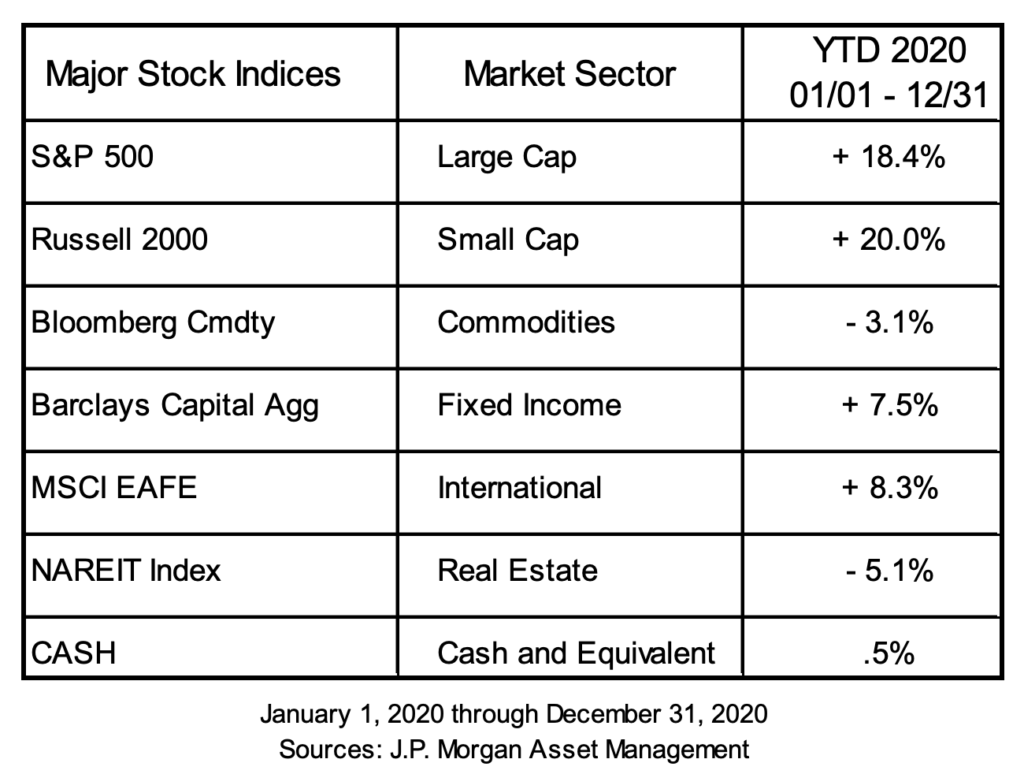

After turning down 34% in mid-March the S&P still closed up 16% for the year. Adjusted for dividends it was up 18.4%. U.S. Large and Small Cap stocks, in addition to Emerging Market equities, paced the global recovery. Commodities and Real Estate Investment Trusts (REIT’s) ended the year down.

Politics and the Markets

The markets have shrugged off the political drama. It is hard to be dispassionate about what we see going on around us, but the markets, generally speaking, could not care less. Every year around election time there are a variety of graphs that make their way through the news cycle showing market performance under a variety of different political control scenarios. Our favorite this last year comes to us courtesy of CNBC. They broke down possible leadership options into various buckets and additionally provided the number of years we have experienced each possible scenario. The “Years” column is what we find most helpful as it provides some background to how large the data set is. As you can see below, U.S. markets have averaged positive returns through all possible combinations of Presidential and Congressional leadership.

Source: CNBC.com sourced from CFRA Investment Research

Based on the outcome of the Georgia special elections we are working under a unified government scenario. The top bar, reflecting an average S&P 500 change of 9.8%, represents a unified Democrat President and Congress. This has been the case for 22 years out of the past 76 on record, a little less than 1/3 of the time. We cannot use history to tell us that the markets will be up again under the current unified government, but we can certainly look to it as an indicator that markets are very good at looking beyond short-term struggles.

The Glass is Half Full

The financial crisis provided us some very important lessons when it comes to navigating large quantities of fiscal and monetary stimulus. First is that common sense is very hard to apply when you look at what is happening around you and how you believe that should translate to market performance. During the financial crisis we dealt with various maladies and global debt issues for years after the 2008/09 recession. Yet the markets still moved higher. Today we still have heightened unemployment with millions of people claiming unemployment benefits, housing and food security is a real concern, and many borders remain closed to some degree or another. During this time markets have set records. Common sense would not seem to apply.

During the Financial Crisis, the Federal Government issued what was at the time considered a huge fiscal stimulus bill in the form of the American Recovery and Reinvestment Act. It was a $787 billion bill directing spending in a multitude of ways. The Federal Reserve cut the interest to 0% and engaged in Quantitative Easing, expanding their balance sheet to stabilize the financial markets. The same thing is happening today, but in amounts of stimulus that are multiple times higher. To date the Federal Government has spent upwards of $3.5 trillion dollars and the Federal Reserve has expanded their balance sheet beyond any former QE programs. This fact leads to our second important lesson from the financial crisis, it does not make sense to hunker down when massive amounts of stimulus are putting the economy on over-drive.,

On December 16, 2020 Federal Reserve Chair Jerome Powell made the following comment:

“So, you know, we’re, we’re thinking that this could be another long expansion, and that we’ll keep our – what we’re saying is, we’re going to keep policy highly accommodative until the expansion is well down the tracks.”

On Friday, January 8th President-Elect Biden said the following:

“I’ve said before, the bi-partisan COVID relief package passed in December was a very important step, but just a down payment…We need more direct relief flowing to families, small businesses, including finishing the job of getting people that $2,000 in relief direct payment…”

He also said:

“Next week, I’ll be here with you all laying out the groundwork for the next COVID economic relief package that meets the critical moment of our economy and our country that we face at the moment.”

To us, these are two very clear indicators that the money spigot will not be turned off anytime soon and the economy will be running on sugar fueled injections for some time. We see potential pitfalls ahead, such as heightened tax rates and a tougher regulatory environment, but on balance we believe those risks are outweighed by the amount of stimulus proposed. Whether a bubble forms from this stimulus is for a different day. For now, we will not be fighting what otherwise appears to be strong market tailwinds.

The Planning Corner

The passage of Proposition 19 in California threw a wrench in the planning of most people in regards to how real estate is passed down to later generations. Our thoughts on this change to estate planning is clearly defined in an update we sent out around Christmas time and which is now posted on our website under the Research & Insights tab. The title is “Proposition 19 – What Happens Now?”

There is very limited time left to work with your estate planning attorney to make any changes you may want to make. You need to take action by February 16, 2021 if you are to take advantage of the current rules. If you have any questions we will certainly make ourselves available to help get you started.

The second change in Prop 19 allows people who are aged 55 and older to transfer the assessed value of their California primary residence to a newly purchased or newly constructed replacement primary residence of greater value than the current property. This is a sharp departure from the prior assessed value transfer where your replacement property needed to be of equal or lesser value. This rule change takes effect on April 1, 2021. Our advice, if you are age 55+ and are preparing to sell your home and move inside California to a more expensive primary residence is to be patient and wait another few months. Let the new law come into being and save yourself a lot of future property tax dollars.

Re-stocking and Opening

There are two words to remember as we move forward in 2021: re-stocking and re-opening. The U.S., and the world, are likely entering a phase of extreme economic activity. As we have all noticed when we walk through the door of Costco one of the first things we see is a whiteboard with a list of what they have and what they don’t have. On a small scale that should tell you there is a lot of re-stocking that needs to take place. As that occurs, goods manufactures will be making a lot of everything to meet current demand in addition to the manufacturing necessary to replenish inventories.

We expect the re-opening to unleash significant pent-up demand as people once again feel like it is safe to “get up and move about the cabin” to borrow a phrase from the airline industry.The driving factor behind this process being successful is continued good news on vaccine efficacy and vaccine delivery. We are looking beyond a successful vaccination program and beginning to position our portfolios for success post-COVID. A couple of graphs will help illustrate what we are looking at.

In the graph above you can see that during the last year growth has continued to become more expensive relative to value, continuing a trend which started several years ago. We have not reached the obscene overvaluations of the late 90’s, but it is obvious the gap between the two has been widening. Eventually this paradigm will shift. As we navigate the months ahead our expectation is to begin a rotation back into value to take advantage of a recovery on that side of the market and to take profits on the growth side. Another way to look at this is to breakdown sector by sector performance in 2020.

As you can see in the next graph, each bar represents a sector of the economy. Moving left to right across the graph are the best performing sectors of the economy to the worst performing sectors.

Source: FactSet, Standard & Poor’s, J.P. Morgan Asset Management

Guide to the Markets – U.S. Data are as of December 31, 2020

The top two performers for 2020 were Online Retail and Information Technology. This makes sense as many of us turned to online shopping and delivery for all of our necessary items and a large portion of the workforce was forced to work from home. We are sure there are worse things to do in this world, but working from home with children practicing the piano surely ranks high. The worst performers were in sectors that will require a re-opening to return to profitability such as hotels, office buildings and airline travel. We were successfully able to profit off this trend with some of the moves we made early on in the pandemic. We have already begun the process of taking some of those profits, such as with the rebalance we performed in late December.

Additionally, our expectation is for international stocks to begin to close the performance gap. Our intention with our last rebalance was to take advantage of the valuation differences between international and domestic stocks by shifting some of the portfolio over to international holdings. We have decided to hold off in this transition as we evaluate the effects of the new COVID strains manifesting in other parts of the globe, in addition to some of the new shutdowns which have occurred, such as what is currently underway in England.

International stocks have lagged the United States for quite some time. It is not a given that they will all of a sudden start performing better and close the gap. However, relative valuations are beginning to make the sector attractive as an increased portion of our overall asset allocation strategy.

The markets look forward, and so are we. This last year was extraordinary in many respects, and completely ordinary in others. After all, the bed still had to get made and dinner still needed to be put on the table. The tax season is once again upon us, and while our expectation is that we will continue to “see” most people through a computer monitor, we are looking forward to speaking to everyone soon.

As always, our desire is to help you make rational, informed and well-reasoned decisions, and we thank you for your continued trust and support. Your input is always welcome, and we ask that you contact us with any questions or concerns.

DISCLOSURE

All information is believed to be from reliable sources; however we make no representation as to its completeness or accuracy. All economic and performance data is historical and not indicative of future results. Market indices discussed are unmanaged. Investors cannot invest in unmanaged indices. Additional risks are associated with international investing, such as currency fluctuations, political and economic instability and differences in accounting standards.

Investing in securities in emerging markets involves special risks due to specific factors such as increased volatility, currency fluctuations and differences in auditing and other financial standards. Securities in emerging markets are volatile and can decline significantly in response to adverse issuer, political, regulatory, market, or economic developments.

An index is a statistical measure of change in an economy or a securities market. In the case of financial markets, an index is an imaginary portfolio of securities representing a particular market or a portion of it. Each index has its own calculation methodology and is usually expressed in terms of a change from a base value. Thus, the percentage change is more important than the actual numeric value. An investment cannot be made directly into an index.

Investing in fixed income securities involves credit and interest rate risk. When interest rates rise, bond prices generally fall. Investing in commodities may involve greater volatility and is not suitable for all investors. Investing in a non-diversified fund that concentrates holdings into fewer securities or industries involves greater risk than investing in a more diversified fund. The equity securities of small companies may not be traded as often as equity securities of large companies so they may be difficult or impossible to sell. Neither diversification nor asset allocation assure a profit or protect against a loss in declining markets. Past performance is not an indicator of future results.

Sean P. Storck and Steven W. Pollock are registered representatives with and securities and Retirement Plan Consulting Program advisory services offered through LPL Financial, a Registered Investment Advisor. Member FINRA/SIPC. Financial Planning offered through Reason Financial, a state Registered Investment Advisor. Investment advice offered through Merit Financial Group, LLC an SEC Registered Investment Advisor. Merit Financial Group and Reason Financial are separate entities from LPL Financial. Tax related services offered through Reason Tax Group. Reason Tax Group is a separate legal entity and not affiliated with LPL Financial. LPL Financial does not offer tax advice or tax related services. Sean P. Storck CA Insurance Lic#OF25995 and Steven W. Pollock CA Insurance Lic#OE98073

Copyright © 2021 Reason Financial all rights reserved.

1 “National Fiscal Policy Response to the Great Recession.” Wikipedia, Wikimedia Foundation, 23 Dec. 2020, en.wikipedia.org/wiki/National_fiscal_policy_response_to_the_Great_Recession#:~:text=In%202008%20the%20United%20States,low%20and%20middle%20income%20Americans.

2 “Here’s Everything the Federal Government Has Done to Respond to the Coronavirus So Far.” Peter G. Peterson Foundation, Peter G. Peterson Foundation, 13 Jan. 2021, www.pgpf.org/blog/2021/01/heres-everything-congress-has-done-to-respond-to-the-coronavirus-so-far.

3 Powell, Jerome. “Transcript of Chair Powell’s Press Conference December 16, 2020.” Federal Reserve Press Conference, 16 Dec. 2020, pp. 1–30.

4 Biden, Joe. Joe Biden Introduces Economics & Labor Nominees Speech Transcript, 8 Jan. 2021.

5 Biden, Joe. Joe Biden Introduces Economics & Labor Nominees Speech Transcript, 8 Jan. 2021.

6 John, Tara, et al. “UK Prime Minister Imposes Harsh Lockdown as New Covid-19 Variant Spreads.” CNN, Cable News Network, 5 Jan. 2021, www.cnn.com/2021/01/04/uk/uk-lockdown-covid-19-boris-johnson-intl/index.html.

Disclosure

This material is for general information only and is not intended to provide specific advice or recommendations for any individual. There is no assurance the views or strategies discussed are suitable for all investors or will yield positive outcomes. Investing involves risks including possible loss of principal. Any company names noted herein are for educational purposes only.

All information is believed to be from reliable sources; however we make no representation as to its completeness or accuracy. All economic and performance data is historical and not indicative of future results. Market indices discussed are unmanaged. Investors cannot invest in unmanaged indices. Additional risks are associated with international investing, such as currency fluctuations, political and economic instability and differences in accounting standards.

Investing in securities in emerging markets involves special risks due to specific factors such as increased volatility, currency fluctuations and differences in auditing and other financial standards. Securities in emerging markets are volatile and can decline significantly in response to adverse issuer, political, regulatory, market, or economic developments.

An index is a statistical measure of change in an economy or a securities market. In the case of financial markets, an index is an imaginary portfolio of securities representing a particular market or a portion of it. Each index has its own calculation methodology and is usually expressed in terms of a change from a base value. Thus, the percentage change is more important than the actual numeric value. An investment cannot be made directly into an index.

Investing in fixed income securities involves credit and interest rate risk. When interest rates rise, bond prices generally fall. Investing in commodities may involve greater volatility and is not suitable for all investors. Investing in a non-diversified fund that concentrates holdings into fewer securities or industries involves greater risk than investing in a more diversified fund. The equity securities of small companies may not be traded as often as equity securities of large companies so they may be difficult or impossible to sell. Neither diversification nor asset allocation assure a profit or protect against a loss in declining markets. Past performance is not an indicator of future results.

Financial Planning offered through Reason Financial, a state Registered Investment Advisor. Investment advice offered through Merit Financial Group, LLC an SEC Registered Investment Advisor. Merit Financial Group and Reason Financial are separate entities. Tax related services offered through Reason Tax Group. Reason Tax Group is a separate legal entity and not affiliated with Merit Financial Group, LLC. Sean P. Storck CA Insurance Lic#OF25995 and Steven W. Pollock CA Insurance Lic#OE98073

Copyright © 2026 Reason Financial all rights reserved.

Continue Reading

3rd Quarter 2026 – Economic and Market Update

Q2 2026 in review: the S&P 500’s best quarter since 2020, oil’s round trip from $114 back to $70, a 4.2% CPI print that would not quit, and a new Fed chair who took 2026 rate cuts off the table — plus what a 15% quarter means for the allocation you actually own.

America at 250: A Birthday Worth Sitting With for a Moment

The United States just turned 250 — and the story reads surprisingly well as a series of 50-year check-ins. Founding-era population the size of San Diego County, two presidents with impeccable dramatic timing, a telephone demo in Philadelphia, quarters you’re still finding in your change — and one compounding machine that started counting in 1926.

American Teens Aren’t Working Summer Jobs Like They Used To

DisclosureThis material is for general information only and is not intended to provide specific advice or recommendations for any individual.…