January 2022 – Economic and Market Update

Executive Summary

- Inflation expectations are sticky business in the world of economics. In the world of common sense, they are more straightforward.

- Interest rates are expected to go higher, tapering is beginning, and fiscal stimulus appears to have come to an end. This should help to pull back inflation.

- Duration/interest rate risk is on the rise, and we are working to reduce exposure to expected rising rates.

The second year of Covid has come to a close with a new variant taking the stage. Markets performed well, except for tech equities and bonds which took a beating into the end of the year. As referenced in our prior update, the general performance of the stock market has been driven primarily by very large companies with strong returns masking the slow recovery for many of the S&P constituents. At this point in the recovery we are taking a broad diversification approach for equities and protecting against interest rate increases for fixed income. With tech taking a big hit, our more growth/tech oriented portfolios have underperformed the market as a whole. We continue to believe in the technology transformation and are adjusting portfolios to take advantage of this trend over the next 5 to 10 years.

Inflation

Inflation and Covid are both starting to feel a little long in the tooth as talking points, making the day they go away feel even further in the future than they probably are. The run-up in inflation is real, and the talking points of the Fed have changed from “transitory” to preventing “persistent” inflation. As you can see below, Headline CPI has rocketed in the last year from the relatively low readings experienced throughout the 2010’s.

Inflation is one of those common sense issues that can be challenging to read academic papers on. You are bombarded with a bunch of gobbledy-gook that can be hard to break through when common-sense should be the guide. If I think a car will be more expensive 6 months from now relative to today, I will buy today. If I think a car will be cheaper 6 months from now, I will delay and buy later. Economists will argue about the role of expectations in driving inflationary or deflationary pressures, but we all make

decisions in real-time and feel the effects as they happen. Some things can be delayed, many others cannot, like groceries, gas, and utilities.

In a recent Federal Reserve research report the opinion of the academics can be summed up rather well in the following:

“Related to this last point, an important policy implication would be that it is far more useful to ensure that inflation remains off of people’s radar screens than it would be to attempt to ‘re-anchor’ expected inflation at some level that policymakers viewed as being more consistent with their stated inflation goal.” Jeremy Rudd, Why Do We Think That Inflation Expectations Matter For Inflation? (And Should We?)

Apparently, if people aren’t thinking about it then it is not a problem, and if they are thinking about it, then it is. When they do think about it, they ask for a raise, or they should, which feeds the cycle even more. Speaking of wages:

Wage growth is ramping up at the highest rate since the early 80’s as well, with the rather unfortunate caveat that it is trailing Headline CPI by a full 1%. As of the last reading, 6.9% inflation versus 5.9% wage growth. So raises are not really all they are cracked up to be right now. Above trend increases in wage growth, with wage growth still trailing inflation is an issue. It creates a situation where more dollars are chasing higher priced goods and services, with a self-repeating cycle potentially creating persistent inflation. This will be one of the trends the Federal Reserve attempts to break as they work on price stability.

The Federal Reserve Bank of Dallas asked a series of questions in December. The results below highlight their responses.

As you can see in the column data on the right, inflation expectations for 2022 have increased and actual inflation in 2021 was substantially higher than expected. More significantly, 2022 inflation expectations from business responses in Dec ’21 were much higher than the responses in July ’21. In the same data set from the Fed the following question was asked, “If costs (including wages) are increasing, to what extent are you passing the higher costs on to customers in the way of price increases?” 75.9% of the respondents indicated they are passing some or all of the increase on to customers.

Back to common-sense, if businesses are experiencing higher costs, they will pass those through to the end consumer. This might feel like a “thank you, Captain Obvious” observation, but it does not always seem so when listening to various pundits in the news.

Our planning for many years has been anchored on expected inflation around 2%. We are not yet changing those assumptions. The main reason is that even though we are experiencing high inflation, we spent the 2010’s in a very low inflation environment keeping planning targets in line with what we have experienced, despite the recent surge in prices. For the time being, our practical advice is to delay large purchases and house projects until we make it past the current struggles. We anticipate high inflation through 2022 with easing coming in mid-2023.

Monetary Policy and Fiscal Policy

The Federal Reserve is doing two things to gain control of price stability. First, is an acceleration in the taper of balance sheet expansion. This will remove some accommodation from the financial markets by taking demand off the table for bonds. The second, is that they have begun telegraphing the eventual increase in interest rates off the 0 – 0.25 target range, this should create non-accommodative conditions thereby slowing price increases.

FOMC targets for the Fed Funds Rate by the end of 2022 are now in the .9% range with market expectations slightly higher at 1%. Whether this will be enough to begin tamping down inflation remains to be seen, but we will be watching, as apparently are others who feel differently about rate increases.

Chinese President Xi Jinping expressed his desire for the Fed to not impose rate increases, taking a moment in a conference recently to say: “If major economies slam on the brakes or take a U-turn in their monetary policies, there would be serious negative spillovers. They would present challenges to global economic and financial stability, and developing countries would bear the brunt of it.”

Something that should help rein in inflation, is less fiscal stimulus. Last spring, the final major Covid spending bill was passed bringing total Covid spending to $5.3 trillion dollars. One of the more prominent financial newspapers, The Financial Times, wrote an editorial in support of the spending. In a recent editorial they retracted: “While this newspaper supported the fiscal stimulus package, it is now clear Biden’s $1.9tn of spending should have been more limited and better targeted. It was an overcorrection…and has contributed to today’s rising inflation.”

With the Federal Reserve accelerating tapering, anticipated interest rate increases, and additional massive Federal spending bills off the table, the fuel for the inflation fire is slowly being cut. On the optimistic side, this will allow the forces we experienced during the 2010’s, demographics and technological advancement, to reassert themselves and return to more muted price and wage growth.

Fixed Income

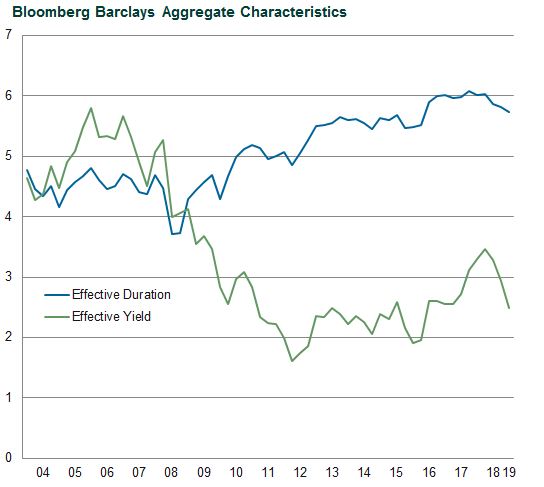

Our expectation of increased interest rates has forced us to look very hard at how our fixed income investments are allocated. For retiree’s and pre-retiree’s fixed income is a substantial portion of many investment portfolios. With persistent low interest rates over the last decade, the reach for yield has increased the average duration inside of traditional bond portfolios. Without diving into the deep end, longer duration is bad in a rising interest rate environment. A 1% increase in rates will result in a 10% reduction in the value of a bond with a duration of 10. One of the flagship bond indexes of the last 30 years is the Bloomberg Barclays Aggregate Bond Index, or AGG for short. For many years a derivative of this index was the backbone of our fixed income portfolio providing stability in yield and credit quality.

The graph above provides us data through 2019 when the duration of the AGG was sitting at about 5.73. It has continued an increase in duration during that time and is now at 6.6. It would be nice to say that this is an isolated phenomenon, but it is not.

In the graph above to the left, the column for Avg. Maturity is what you are looking for. The graph on the right illustrates the impact of a 1% rise in interest rates on the principal value of the bond. It does not look good for most of the bond asset classes. Our method on the bond side has been to reduce duration as much as possible. While the duration of the AGG is sitting at 6.6, and other U.S. investment grade bonds are at 8.7, we have reduced duration to the 2.6 to 2.7 range, with a current yield of 2.8%. We are doing our best to replace duration risk with projected yield.

This has been a work in progress for the better part of 2021, and we do not anticipate a slackening through the remainder of 2022.

Is there a silver lining?

There is indeed a silver lining to be found. In inflationary environments stocks have traditionally provided a hedge against inflation, particularly in more moderate ranges from 1.1% to 4%. Current inflation presages reduced returns over time, but with moderated inflation we anticipate stocks to perform well over time. Low or negative inflation periods have much worse returns as you can see from the chart above.

At this time there are no legislative items to focus on. With Build Back Better possibly turning into Build Back Smaller via breaking it into multiple bills, there may be some items popping up in the coming year, but for now, it is legislative gridlock and business as usual.

In summary, our expectation for 2022 is for high volatility in equities and bonds as the various powers that be tinker, or sledgehammer, away at inflation. In his most recent press-conference, Fed Chair Jerome Powell had a Star Wars-esque moment when he said, “This is not the inflation we were looking for…”. He was referring to the myriad problems popping up from Covid leading to current economic conditions. Monetary and fiscal policy will be playing whack-a-mole to see what works while the rest of us pay at the register.

As always, our desire is to help you make rational, informed and well-reasoned decisions, and we thank you for your continued trust and support. Your input is always welcome, and we ask that you contact us with any questions or concerns.

DISCLOSURE

All information is believed to be from reliable sources; however we make no representation as to its completeness or accuracy. All economic and performance data is historical and not indicative of future results. Market indices discussed are unmanaged. Investors cannot invest in unmanaged indices. Additional risks are associated with international investing, such as currency fluctuations, political and economic instability and differences in accounting standards.

Investing in securities in emerging markets involves special risks due to specific factors such as increased volatility, currency fluctuations and differences in auditing and other financial standards. Securities in emerging markets are volatile and can decline significantly in response to adverse issuer, political, regulatory, market, or economic developments.

An index is a statistical measure of change in an economy or a securities market. In the case of financial markets, an index is an imaginary portfolio of securities representing a particular market or a portion of it. Each index has its own calculation methodology and is usually expressed in terms of a change from a base value. Thus, the percentage change is more important than the actual numeric value. An investment cannot be made directly into an index.

Investing in fixed income securities involves credit and interest rate risk. When interest rates rise, bond prices generally fall. Investing in commodities may involve greater volatility and is not suitable for all investors. Investing in a non-diversified fund that concentrates holdings into fewer securities or industries involves greater risk than investing in a more diversified fund. The equity securities of small companies may not be traded as often as equity securities of large companies so they may be difficult or impossible to sell. Neither diversification nor asset allocation assure a profit or protect against a loss in declining markets. Past performance is not an indicator of future results.

Sean P. Storck and Steven W. Pollock are registered representatives with and securities and Retirement Plan Consulting Program advisory services offered through LPL Financial, a Registered Investment Advisor. Member FINRA/SIPC. Financial Planning offered through Reason Financial, a state Registered Investment Advisor. Investment advice offered through Merit Financial Group, LLC an SEC Registered Investment Advisor. Merit Financial Group and Reason Financial are separate entities from LPL Financial. Tax related services offered through Reason Tax Group. Reason Tax Group is a separate legal entity and not affiliated with LPL Financial. LPL Financial does not offer tax advice or tax related services. Sean P. Storck CA Insurance Lic#OF25995 and Steven W. Pollock CA Insurance Lic#OE98073

i “FOMC Press Conference.” Board of Governors of the Federal Reserve System, 15 Dec. 2021, https://www.federalreserve.gov/monetarypolicy/fomcpresconf20211215.htm.

iiRudd, Jeremy B. (2021). “Why Do We Think That Inflation Expectations Matter for Inflation? (And Should We?),” Finance and Economics Discussion Series 2021-062. Washington: Board of Governors of the Federal Reserve System, https://doi.org/10.17016/FEDS.2021.062.

iii “Texas Business Outlook Surveys – Special Questions.” Dallasfed.org, 27 Dec. 2021, https://www.dallasfed.org/research/surveys/tbos/2021/2112q.aspx.

iv Goldstein, Steve. “Xi Jinping Warns Fed against Hiking Interest Rates.” MarketWatch, MarketWatch, 18 Jan. 2022, https://www.marketwatch.com/story/xi-jinping-warns-fed-against-hiking-interest-rates-11642502735?siteid=yhoof2&yptr=yahoo.

v The Editorial Board. “Biden’s Disappointing First Year in Office.” Financial Times, Financial Times, 29 Dec. 2021, https://www.ft.com/content/33cd24e7-2a82-4259-9ef0-58b3f0a7a2d2.

vi Shingler, Thomas. “Analyzing Changes to the Bloomberg Barclays Aggregate.” Callan, 28 Oct. 2020, https://www.callan.com/blog-archive/aggregate-changes/.

vii Roland, Emily R, and Matthew D Miskin. “Inflation and Stock Market Performance: John Hancock Investment Mgmt.” John Hancock Investment Management, 1 Nov. 2021, https://www.jhinvestments.com/viewpoints/market-outlook/inflation-whats-next-and-how-to-position-portfolios.

viii “FOMC Press Conference.” Board of Governors of the Federal Reserve System, 15 Dec. 2021, https://www.federalreserve.gov/monetarypolicy/fomcpresconf20211215.htm.

Disclosure

This material is for general information only and is not intended to provide specific advice or recommendations for any individual. There is no assurance the views or strategies discussed are suitable for all investors or will yield positive outcomes. Investing involves risks including possible loss of principal. Any company names noted herein are for educational purposes only.

All information is believed to be from reliable sources; however we make no representation as to its completeness or accuracy. All economic and performance data is historical and not indicative of future results. Market indices discussed are unmanaged. Investors cannot invest in unmanaged indices. Additional risks are associated with international investing, such as currency fluctuations, political and economic instability and differences in accounting standards.

Investing in securities in emerging markets involves special risks due to specific factors such as increased volatility, currency fluctuations and differences in auditing and other financial standards. Securities in emerging markets are volatile and can decline significantly in response to adverse issuer, political, regulatory, market, or economic developments.

An index is a statistical measure of change in an economy or a securities market. In the case of financial markets, an index is an imaginary portfolio of securities representing a particular market or a portion of it. Each index has its own calculation methodology and is usually expressed in terms of a change from a base value. Thus, the percentage change is more important than the actual numeric value. An investment cannot be made directly into an index.

Investing in fixed income securities involves credit and interest rate risk. When interest rates rise, bond prices generally fall. Investing in commodities may involve greater volatility and is not suitable for all investors. Investing in a non-diversified fund that concentrates holdings into fewer securities or industries involves greater risk than investing in a more diversified fund. The equity securities of small companies may not be traded as often as equity securities of large companies so they may be difficult or impossible to sell. Neither diversification nor asset allocation assure a profit or protect against a loss in declining markets. Past performance is not an indicator of future results.

Financial Planning offered through Reason Financial, a state Registered Investment Advisor. Investment advice offered through Merit Financial Group, LLC an SEC Registered Investment Advisor. Merit Financial Group and Reason Financial are separate entities. Tax related services offered through Reason Tax Group. Reason Tax Group is a separate legal entity and not affiliated with Merit Financial Group, LLC. Sean P. Storck CA Insurance Lic#OF25995 and Steven W. Pollock CA Insurance Lic#OE98073

Copyright © 2026 Reason Financial all rights reserved.

Continue Reading

2nd Quarter 2026 – Economic and Market Update

Q1 2026 in review: oil shock, S&P 500 down 4.3%, commodities up 24.4%, the cease-fire that became a blockade — and the planning moves that matter most coming out of a quarter like this one.

It’s Now More Common To Have A Baby In Your Thirties Than In Your Twenties

DisclosureThis material is for general information only and is not intended to provide specific advice or recommendations for any individual.…

When Does Refinancing Actually Make Sense? A 2026 Reality Check

If you locked in a mortgage at 7% or higher in 2023 or 2024, you’ve probably been watching rates with…