October 2023 – Economic and Market Update

EXECUTIVE SUMMARY

- The strong labor market may make it hard for the Federal Reserve to resist raising rates again in the future.

- The Magnificent Seven isn’t just a retread movie anymore, now it is the name of the high-flying mega-cap tech companies driving stock returns in 2023.

- Fixed income investing doesn’t look as bad as it used to; in fact, it is starting to look downright attractive.

The 3rd Quarter is over and the end of the year is around the corner. It may or may not feel like the end of the year if you are a resident of California and still haven’t had to file and pay your taxes for 2022. If you are covered under the CA Disaster Declaration, you were granted one final reprieve by the IRS that lasts until November 16th, 2023. Don’t wait until the 16th. It doesn’t make your tax preparer happy. The tax filing PSA is now over.

As the year has progressed, markets have experienced bouts of volatility as concerns about the direction of Federal Reserve interest rate policy have waxed and waned. That said, the economy in the U.S. shows remarkable resilience. No matter how many times it looks like the wheels might come off, they just keep on turning.

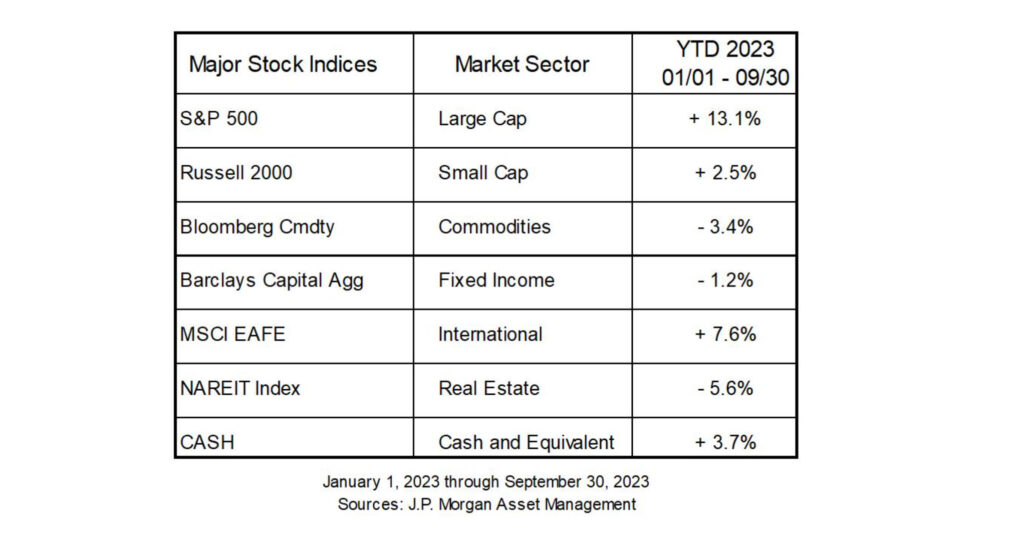

A term has been borrowed from Hollywood to describe the best stocks of the year, “The Magnificent Seven”. Apple, Microsoft, Alphabet (Google), Nvidia, Tesla, Amazon, and Meta (Facebook) have driven most of the stock market returns this year for the S&P 500. Fixed income has experienced another down year, though not as significant as last year. Interest rates have risen substantially as the Federal Reserve has increased the Fed Funds rate into the 5.25% – 5.50% range. With positive returns being so concentrated in a small number of stocks, returns year-to-date have been muted across the major asset classes with the exception of the S&P 500, which has a high concentration of the aforementioned seven stocks. i

The Labor Market

One of the main questions in the financial markets goes something like this, what will the Federal Reserve do with interest rates moving forward? For the time being rates have held steady over the last couple cycles. The projection a year ago that we would see rate decreases in late 2023 did not prove prophetic. Instead, the Federal Reserve has left open the door for more minor increases. The direction of the labor market will likely factor heavily into their decision making process.

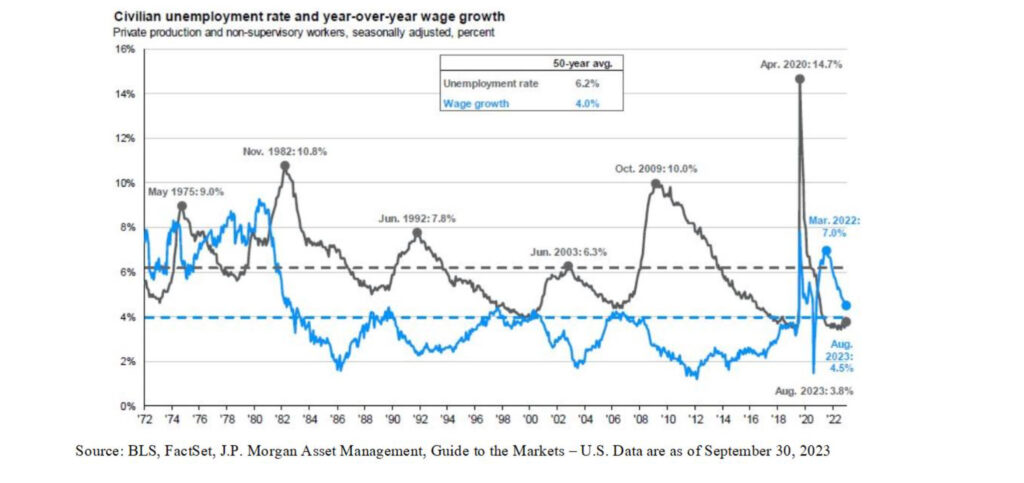

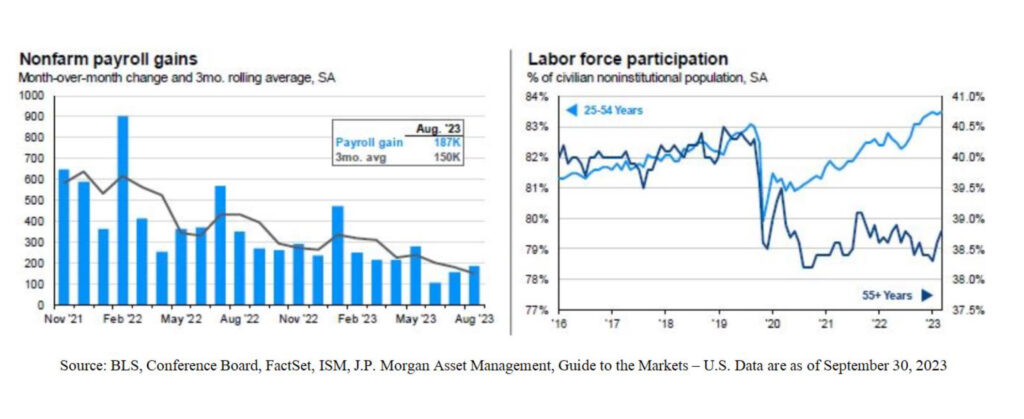

Wage growth is still above the historic average, 4.5% current growth versus historical growth of 4% as you can see in the graph on the previous page. Non-farm payroll gains have slowed down over the last couple years as you can see below. However, it is highly likely for the labor market to remain tight as structural employment issues remain a concern. By structural employment we are referring to the labor force participation rate and the availability of workers. Side by side with payroll gains below is the labor force participation rate broken into two cohorts, 25-54 year old workers, and 55+ aged workers.

The unemployment rate is low, currently at 3.8%. The proportion of 25-54 year old workers participating in the workforce is higher than it was prior to the pandemic. The proportion of 55+ workers in the labor force, has stagnated in the last year. The total labor pool is structurally limited by the number of workers available, and that pool looks like it is getting a little smaller. Federal Reserve Chair Jerome Powell comments often on the state of the labor market. ii

In his most recent press conference on September 20th, 2023, Chair Powell stated that, “The jobs-to-workers gap has narrowed, labor demand still exceeds the supply of available workers. FOMC participants expect the rebalancing in the labor market to continue, easing upward pressures on inflation.” With the labor pool being what it is, it is not a given for the rebalancing of the labor pool to occur in a way that fundamentally reduces upward pressures on inflation smoothly and easily.

Recently, Mohamed A. El-Erian, prominent economist and president of Queens’ College, Cambridge, penned an article in the Financial Times. The title sums it up nicely, “The US may no longer avoid a recession”. One statement in his analysis struck a chord, “Indeed, the world’s most influential central bank has yet to sufficiently embrace the fundamental change in the basic characterization of the economy from a world of insufficient demand to one in which the supply sector is a lot less flexible for several years. The longer the Fed takes to adjust, the greater the hit to economic wellbeing.” iii

In looking at the situation facing the labor market, his statement seems spot on. The labor pool is what it is. Available workers are not what they once were in aging Western nations, and the supply of workers is constrained. All of this leads us to a simple conclusion: be prepared for, and make your big financial decisions, based on an interest rate environment that stays higher for longer.

Stock Valuations And Pricing Disparities

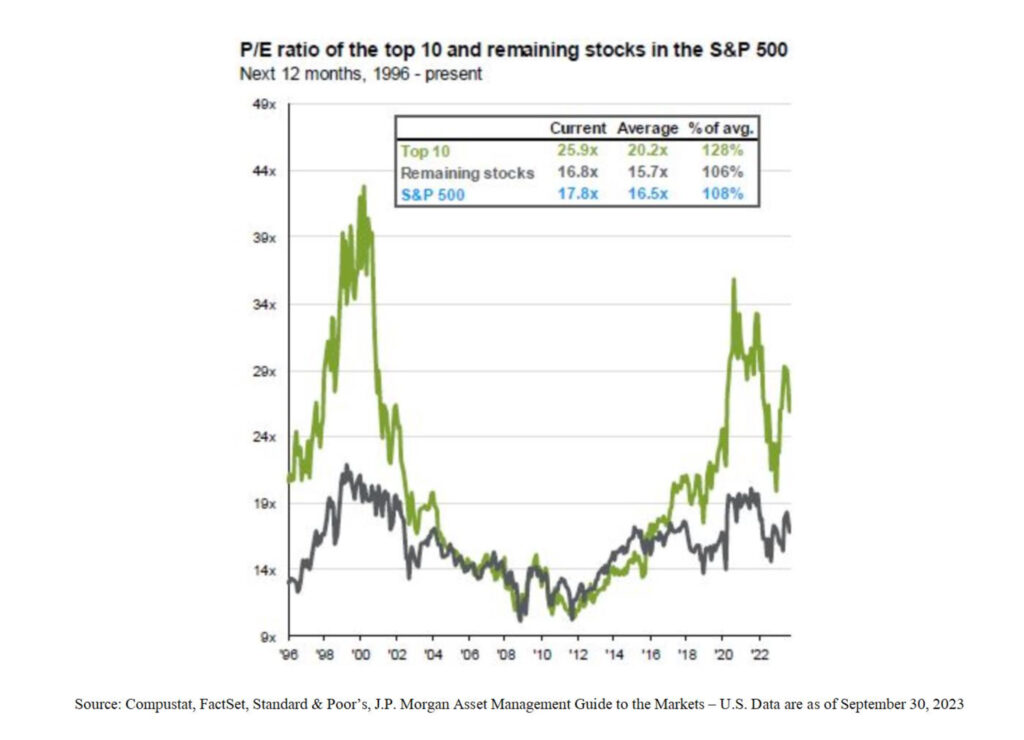

The top ten stocks in the S&P 500 are dramatically outpacing their peers. One way to look at this is in the P/E ratio spread. The top 10 are sitting at a current P/E, price to earnings, of 25.9x averaged out among them. The remaining 490 stocks in the index are at an average P/E ratio of 16.8x. If cap compression begins to occur among the largest holdings in the S&P, meaning the multiples come down, we could see a painful unwinding from the current index levels. We are a couple missed earnings reports away from seeing negative returns in the S&P. Domestic indicies without heavy concentrations to these specific mega-cap tech companies, such as the DOW 30 and Russell 2000, are flat to negative on the year.

We have done our best this year to try to focus on diversifying away from this concentration risk. In order to do that, we have made moves in our portfolios to meet the following three goals:

1. Be diversified.

2. Focus on quality.

3. Avoid market segments with high market caps.

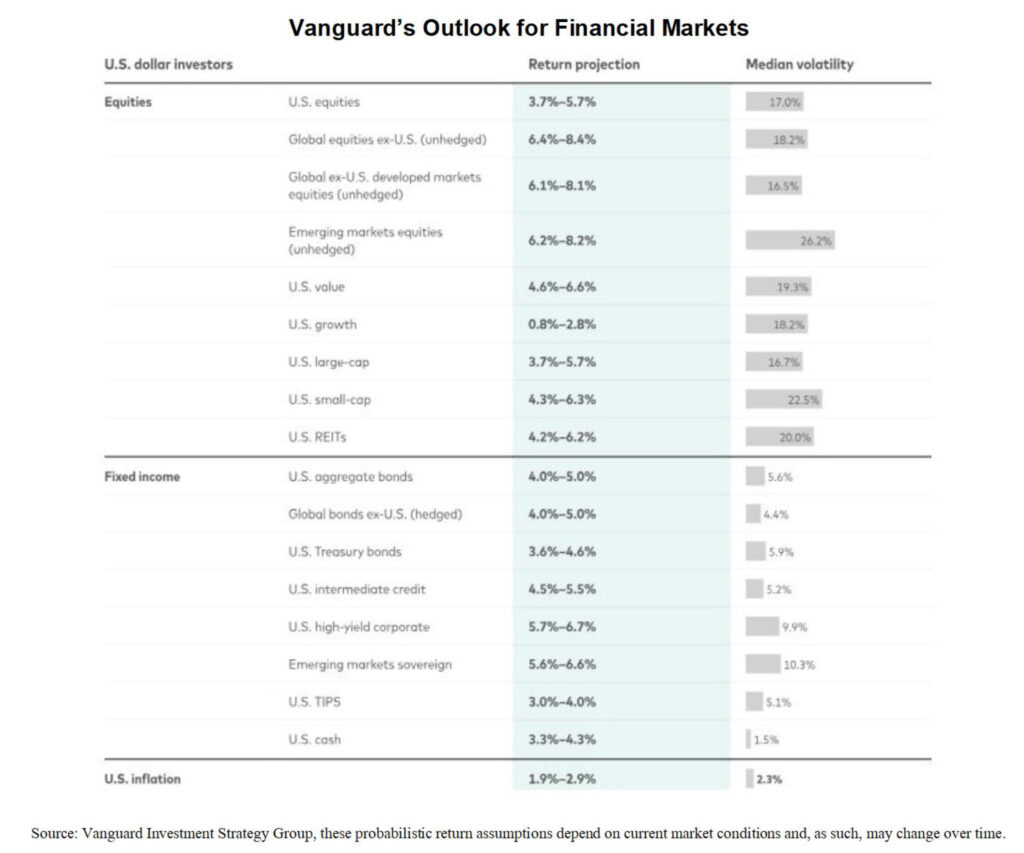

Our goal in focusing on these three priorities is to look out 3, 5, and 10 years and, hopefully, set ourselves up for success. At current valuations the 10-year outlook is for moderate growth as you can see below in the Vanguard Outlook for Financial Markets published in September 2023. iv

U.S equities are forecast for a relatively modest return between 3.7% – 5.7% versus U.S. aggregate bonds (high-quality) of 4.0% – 5.0%. The current interest rate environment is once again making fixed income investing look very attractive.

During the recovery from the 2008/09 financial crisis much was written about the end of the 30-year bull market in bonds. The last bond bull market saw its genesis in the 80’s during our last major inflation fight. No one is forecasting interest rates to rival what we saw 40 years ago, but the current interest rate regime may spark another mini bull market in bonds once again. With nominal rates now above 5% and real interest rates in the positive range, opportunities to gain both stability and capital appreciation will present themselves in the bond space.

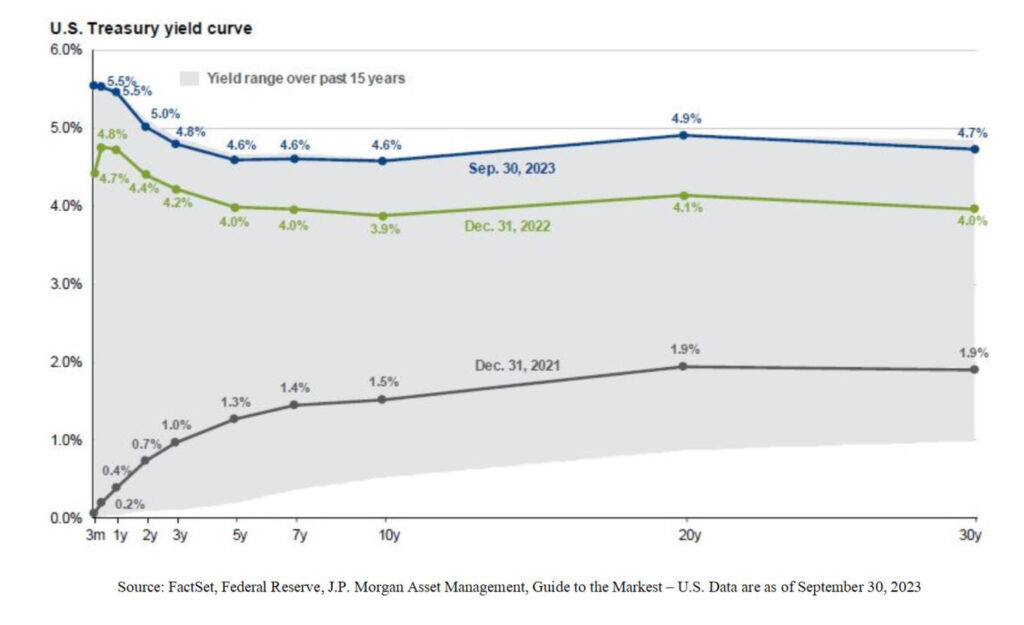

As you can see above, the yield curve has elevated substantially from just two years ago. There are now opportunities to earn yield which seemed impossible a short time ago, but are now more in line with historic norms. The short side of the curve is still inverted with short-term rates outpacing intermediate and long-term rates. However, as the higher for longer team gains steam you can see that the curve is flattening in the middle with 5 and 10-year rates now even. Investing in fixed income securities carries risks, primarily default and interest rate, but with rate increases forecast to be minimal moving forward we expect opportunities in this sector to present themselves.

Looking Ahead

Geo-political risks have heightened with the awful attacks on Israel by Hamas. There is still not enough clarity on how this situation will evolve, much less how economic markets will be impacted by it, for us to make any recommendations. A great source of continual analysis on the situation in Israel and the ongoing war in Ukraine is Peter Zeihan. We have found his insight to be thoughtful and thorough. He is a prominent geo-political analyst and frequent guest on the major media networks here in the U.S. If you find yourself looking for information, and are an internet user, we highly recommend his YouTube channel and Twitter (X) feed.

The Planning Corner: Unified Estate And Gift Tax Exclusion

Tax planning for death is slated to get more expensive starting in 2026. The Unified Estate and Gift Tax exclusion for 2023 is $12,920,000, per person. On January 1, 2026, barring any change in estate tax law between now and then, the unified exclusion will be revised down somewhere into the $5 million to $7 million range adjusted for inflation, per person, in accordance with the sunset provisions of the Tax Cuts and Jobs Act. v

While this is an issue that only a sliver of the population will be affected by, it is a very significant issue for those impacted. There are a variety of ways to plan for this change.

1. Gift now.

2. Charitable trust planning.

3. Estate portability if a spouse passes away.

4. Irrevocable life insurance trust.

These are just a few of the options. We plan with what we know. What we know right now is the exclusion is being reduced on January 1, 2026. Many things may change between now and then. However, with interest payments on the Federal Government debt higher than they have been in many years, coupled with large fiscal deficits and ballooning Federal Debt, gathering more tax revenue is going to be on the list of government priorities.

The end of the year is nearly here. It’s a tad early, but we want to give you a few items you may wish to put on your New Year’s Resolution list. Or don’t want to put on there, but should.

1. If you don’t have a family trust yet, talk to us about whether or not you need one. If so, we have multiple estate planning attorneys we can recommend.

2. Bump your retirement contribution savings rate up. If you aren’t saving 15% to 20% of your annual income, get the percentage you are saving a little closer to that figure.

3. Review your current life insurance and make sure it is suitable for your current life circumstances.

4. Create a file, digital or analog, which has a list of all current assets and liabilities. If something happens to you, it will make the life of your successor much better. This is very important if that successor happens to be your spouse, who has avoided being involved in the finances all these years.

As always, we are here to guide you through these complex dynamics and help you make informed decisions aligned with your financial goals. We appreciate your continued trust and partnership, and we welcome any questions or concerns you might have as we advance together.

The economic landscape is ever-evolving, but our commitment to supporting your financial journey remains unchanged. We will continue to closely monitor the situation, adjusting strategies as necessary, and keeping you informed of significant developments that may impact your financial outlook.

DISCLOSURE

All information is believed to be from reliable sources; however we make no representation as to its completeness or accuracy. All economic and performance data is historical and not indicative of future results. Market indices discussed are unmanaged. Investors cannot invest in unmanaged indices. Additional risks are associated with international investing, such as currency fluctuations, political and economic instability and differences in accounting standards.

Investing in securities in emerging markets involves special risks due to specific factors such as increased volatility, currency fluctuations and differences in auditing and other financial standards. Securities in emerging markets are volatile and can decline significantly in response to adverse issuer, political, regulatory, market, or economic developments.

An index is a statistical measure of change in an economy or a securities market. In the case of financial markets, an index is an imaginary portfolio of securities representing a particular market or a portion of it. Each index has its own calculation methodology and is usually expressed in terms of a change from a base value. Thus, the percentage change is more important than the actual numeric value. An investment cannot be made directly into an index.

Investing in fixed income securities involves credit and interest rate risk. When interest rates rise, bond prices generally fall. Investing in commodities may involve greater volatility and is not suitable for all investors. Investing in a non-diversified fund that concentrates holdings into fewer securities or industries involves greater risk than investing in a more diversified fund. The equity securities of small companies may not be traded as often as equity securities of large companies so they may be difficult or impossible to sell. Neither diversification nor asset allocation assure a profit or protect against a loss in declining markets. Past performance is not an indicator of future results.

Sean P. Storck and Steven W. Pollock are registered representatives with and securities and Retirement Plan Consulting Program advisory services offered through LPL Financial, a Registered Investment Advisor. Member FINRA/SIPC. Financial Planning offered through Reason Financial, a state Registered Investment Advisor. Investment advice offered through Merit Financial Group, LLC an SEC Registered Investment Advisor. Merit Financial Group and Reason Financial are separate entities from LPL Financial. Tax related services offered through Reason Tax Group. Reason Tax Group is a separate legal entity and not affiliated with LPL Financial. LPL Financial does not offer tax advice or tax related services. Sean P. Storck CA Insurance Lic#OF25995 and Steven W. Pollock CA Insurance Lic#OE98073

Copyright © 2021 Reason Financial all rights reserved. i Krauskopf, Lewis. “Analysis: Wall Street’s ‘Magnificent Seven’ Face Moment of Truth as Earnings Season Arrives.” Reuters, Thomson Reuters, 19 Oct. 2023, www.reuters.com/markets/us/wall-streets-magnificent-seven-face-moment-truth-earnings-season-arrives-2023-10-19/#:~:text=Huge%20rallies%20for%20the%20so,outsized%20weighting%20in%20the%20index. ii “September 19-20, 2023 FOMC Press Conference.” Federal Reserve, Federal Reserve, 20 Sept. 2023, https://www.federalreserve.gov/monetarypolicy/fomcpresconf20230920.htm. Accessed 16 Oct. 2023. iii El-Erian, Mohamed. “The US May No Longer Avoid a Recession.” Financial Times, Financial Times, 5 Oct. 2023, www.ft.com/content/02a899eb-e899-4b6f-8848-b5240a7127e9. iv “Our Investment and Economic Outlook, September 2023.” Vanguard, Vanguard , 14 Sept. 2023, corporate.vanguard.com/content/corporatesite/us/en/corp/articles/investment-economic-outlook-sept-2023.html. v Roundtree, Scott. “Estate Tax Law Changes in 2026 May Impact Your Taxes a Lot-Gift Now!” LSL CPAs, 28 June 2023, lslcpas.com/estate-tax-law-changes-in-2026-may-impact-your-taxes-a-lot-gift-now/#:~:text=The%20unified%20estate%20and%20gift,ending%20December%2031%2C%202025).

Disclosure

This material is for general information only and is not intended to provide specific advice or recommendations for any individual. There is no assurance the views or strategies discussed are suitable for all investors or will yield positive outcomes. Investing involves risks including possible loss of principal. Any company names noted herein are for educational purposes only.

All information is believed to be from reliable sources; however we make no representation as to its completeness or accuracy. All economic and performance data is historical and not indicative of future results. Market indices discussed are unmanaged. Investors cannot invest in unmanaged indices. Additional risks are associated with international investing, such as currency fluctuations, political and economic instability and differences in accounting standards.

Investing in securities in emerging markets involves special risks due to specific factors such as increased volatility, currency fluctuations and differences in auditing and other financial standards. Securities in emerging markets are volatile and can decline significantly in response to adverse issuer, political, regulatory, market, or economic developments.

An index is a statistical measure of change in an economy or a securities market. In the case of financial markets, an index is an imaginary portfolio of securities representing a particular market or a portion of it. Each index has its own calculation methodology and is usually expressed in terms of a change from a base value. Thus, the percentage change is more important than the actual numeric value. An investment cannot be made directly into an index.

Investing in fixed income securities involves credit and interest rate risk. When interest rates rise, bond prices generally fall. Investing in commodities may involve greater volatility and is not suitable for all investors. Investing in a non-diversified fund that concentrates holdings into fewer securities or industries involves greater risk than investing in a more diversified fund. The equity securities of small companies may not be traded as often as equity securities of large companies so they may be difficult or impossible to sell. Neither diversification nor asset allocation assure a profit or protect against a loss in declining markets. Past performance is not an indicator of future results.

Financial Planning offered through Reason Financial, a state Registered Investment Advisor. Investment advice offered through Merit Financial Group, LLC an SEC Registered Investment Advisor. Merit Financial Group and Reason Financial are separate entities. Tax related services offered through Reason Tax Group. Reason Tax Group is a separate legal entity and not affiliated with Merit Financial Group, LLC. Sean P. Storck CA Insurance Lic#OF25995 and Steven W. Pollock CA Insurance Lic#OE98073

Copyright © 2026 Reason Financial all rights reserved.

Continue Reading

2nd Quarter 2026 – Economic and Market Update

Q1 2026 in review: oil shock, S&P 500 down 4.3%, commodities up 24.4%, the cease-fire that became a blockade — and the planning moves that matter most coming out of a quarter like this one.

It’s Now More Common To Have A Baby In Your Thirties Than In Your Twenties

DisclosureThis material is for general information only and is not intended to provide specific advice or recommendations for any individual.…

When Does Refinancing Actually Make Sense? A 2026 Reality Check

If you locked in a mortgage at 7% or higher in 2023 or 2024, you’ve probably been watching rates with…