A Strong Economy or Looming Recession?

Investment Management Research Group (IMRG) of 1st Global

Impending signs of “doom” lurking around the corner sent U.S. stock markets into a tailspin this week, falling roughly 4 percent at their lowest intra-day point. Volatility and downward pressure has been a relatively consistent theme for the Dow Jones Industrial Average, the S&P 500 index and the Nasdaq Composite Index in recent weeks as oil prices have taken a dive, the U.S. and China continue to negotiate trade and tariffs, and whispers of recession could be heard around the marketplace.

Oil Prices

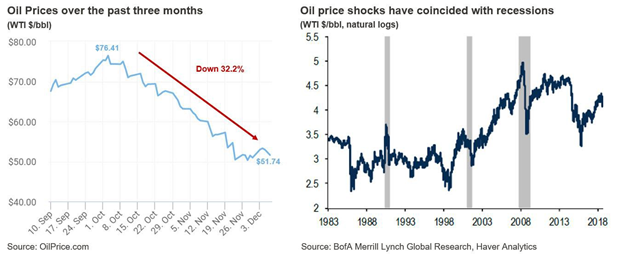

Oil has taken a dive during the fourth quarter of 2018, with West Texas Intermediate (WTI) prices falling from above $76 per barrel on Oct. 6 to just over $51 per barrel on Dec. 6. This sizable drop in crude has fueled fears of recession by many market followers given the strong historical connection between oil price shocks and economic recessions. In addition, correlations between crude oil prices and stock markets have been uncharacteristically high for much of 2018 – close to 0.80.

As you can see from the chart above on the right, oil prices have spiked prior to most of the recessions dating back several decades. In addition, analysts from Bank of America–Merrill Lynch believe that the Great Recession “might not have been as dire absent the oil price shock (Hamilton 2008). That said, an increase in oil prices this time-around may not be as damaging as the U.S. has become a much bigger producer of oil and, in turn, less reliant on crude imports.”

While oil prices have historically been driven by demand, markets now appear to be primarily driven by supply – specifically fears of oversupply. This is because many believe that U.S. technological advances in hydraulic fracturing and horizontal drilling over the last decade have changed the price dynamics of oil and gas. According to estimates from the Federal Reserve, the U.S. is expected to produce approximately 11.2 million barrels of oil per day by the end of 2018.

Recently, Organization of Petroleum Exporting Countries (OPEC), one of the world’s largest suppliers of crude oil, has been fanning fears of a glut in global oil supply. The group of oil- producing countries has been adhering to self-imposed production cuts over the past year, but these production caps are set to expire at the end of the year.

Although energy prices rallied in September with traders bracing for renewed U.S. sanctions on Iran coupled with President Trump’s threat to sanction foreign firms buying Iranian crude, October forecasts had suggested slower demand growth just as output from top producers were rising. Cartel member adherence to OPEC production cuts had been a support for the last year; however, the cuts expire at year’s end. OPEC-member countries met this week in Vienna to determine whether these production curbs would be renewed, but the meeting concluded without a final decision being made.

U.S./China Trade Talk

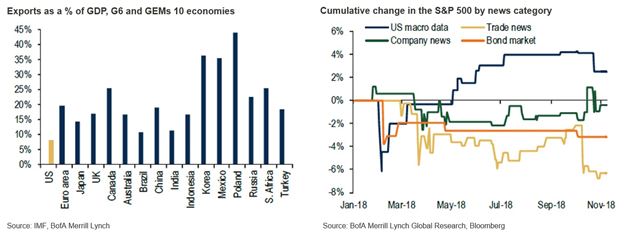

A significant amount of media attention has been placed on ongoing trade discussions between China and the U.S. – the world’s largest economies and trade partners. Even though leaders from the two countries appear to have come to a truce, there’s a significant likelihood tariffs on certain Chinese goods are on the horizon in 2019.

While the Trump Administration’s approach to trade negotiations will certainly continue to grab headlines, it’s important to remember that the eventual outcome will likely have a limited effect on the U.S. economy. The chart on the left below illustrates that the U.S. economy is much less reliant on exports than other major countries around the world. In a November 14, 2018 economic viewpoint from Bank of America–Merrill Lynch¹, analysts highlighted that, “Compared to other large economies the U.S. has limited exposure to global demand. Recent undulations in the global backdrop, from the soft patch of 2015-16 to the coordinated pickup in 2017, suggest that a slowdown in demand for U.S. exports would not be large enough to cause a recession.”

Considering this loose correlation, U.S. stock markets have moved disproportionately downward when trade talks have hit the front page. The chart on the right above from Bank of America– Merrill Lynch shows that “Trade News” has had a stronger downward effect on the S&P 500 Index than company news, the bond market and macroeconomic data on the U.S.

Inversion of the U.S. Treasury Yield Curve

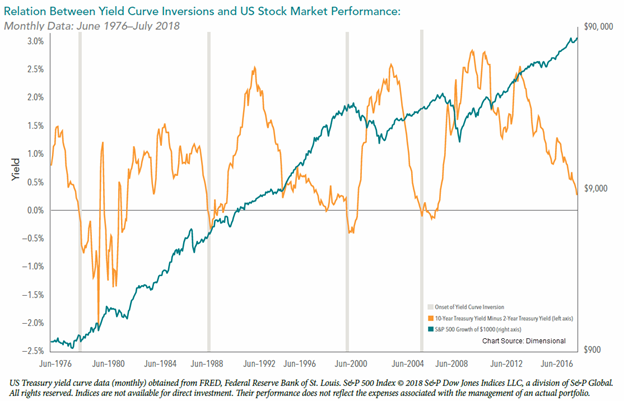

We also reached a technical flashpoint this week with a mild inversion in parts of the U.S. Treasury yield curve. As of the writing of this piece, the 2-year U.S. Treasury is yielding slightly more than the 5-year U.S. Treasury yield. The widely followed 2-10 year U.S. Treasury spread is 13 basis point currently.

While some market pundits believe this leading indicator is a sign that a recession is likely to begin in the near future, that’s not necessarily the case. Recent research from Dimensional, shows that the link between periods of yield inversion and negative stock market returns isn’t as strong as many think.

The below chart from Dimensional illustrates growth of a hypothetical $1,000 investment in the S&P 500 Index since June 1976 plotted against the term spread – which is defined as the 10- year U.S. Treasury yield minus the two-year U.S. Treasury yield.

The U.S. Treasury yield curve inverted in February 2006 but the S&P 500 posted positive returns for the following 12-months. In addition, the yield curve returned to a positive slope in June 2007 prior to the market’s downturn beginning in October 2007. Dimensional’s research shows that returns (in local currency) of major indices for five of the largest developed nations (U.S., UK, Australia, Germany and Japan) were higher 86 percent of the time 12 months later and 71 percent of the time after 36 months.

The company sums up its findings with the following, “If an investor interpreted the inversion as a sign of an imminent market decline, being out of stocks during the inverted period could have resulted in a substantial opportunity cost. And if the same investor invested in stocks once the curve returned to a positive slope, they would also have been exposed to the stock market weakness that followed”²

Positive Indicators of a Strong Economy or Looming Recession?

The impossible question many investors are likely asking themselves is – are we headed for a recession? The answer is…it depends on where you look.

The National Bureau of Economic Research (NBER), the organization responsible for officially declaring a recession, defines a recession as a “significant decline in economic activity spread across the economy, lasting more than a few months, normally visible in real GDP, real income, employment, industrial production, and wholesale-retail sales.”

By those measures, there’s certainly some positive indicators of a strong economy. While corporate debt is close to an all-time high during a business cycle, interest coverage ratios remain solid. Company earnings have been strong this year and unemployment in the U.S. continues to be low.

Economic data continues to show strength for the American consumer, which is important as consumers drive a large portion of the market. Consumers are continuing to spend during this holiday season and balance sheets look healthy with outstanding household debt as a percentage of total GDP around 79 percent – far below the peak levels of 125 percent seen in 2009.

Despite this strength, the consensus estimate of the probability that we will experience a decline in GDP a year from now has reached its highest level since 2008 according to the Survey of Professional Forecasters and reported by Goldman Sachs.³ This means we likely won’t know the answer to the recession question until this time next year. In the meantime, Wall Street and Main Street are keeping both eyes on the Federal

Reserve and rising interest rates. While nobody knows the Fed’s next move, a report from Capital Economics out this week said the company thinks “the Fed will raise rates twice in the opening six months of 2019, taking the fed funds target range to between 2.75 percent and 3 percent.”⁴

Recession or not, we believe clients should continue to follow their long-term financial plans and revisit their goals and objectives with their trusted financial advisors if feeling uncertain about the future. If the current market volatility persists, continuing to dollar cost average into the market at lower prices can be an opportunity to positively affect long-term performance.

Economic and market cycles come and go, but a solid, long-term financial plan revisited regularly can help withstand the test of time.

Sources:

¹ Bank of America–Merrill Lynch: U.S. Economic Viewpoint “Everything you need to know about recessions…and more” November 14, 2018.

² Dimensional: “What Does a Yield Curve Inversion Mean for Investors?” August 2018.

³ Goldman Sachs: Economics Research “U.S. Daily: Consensus Estimates of Recession Risk: The Wisdom of Crowds?” December 5, 2018.

⁴ Capital Economics: U.S. Economics Update “What would it take to convince the Fed to pause early?” December 3, 2018

About the Investment Management Research Group

The Investment Management Research Group (IMRG) of 1st Global is a team of tenured investment professionals that operates under the oversight of the 1st Global Investment Committee and is tasked with finding “best-in-class” investment managers and products for use across the IMS Select Portfolios strategies as well as other IMS programs. The team’s primary responsibilities include portfolio construction and investment manager due diligence, monitoring and selection. The team brings years of experience and investment knowledge to help guide clients with asset class allocation and individual fund selection, which are aimed at providing optimal risk-adjusted returns within each risk category.

Securities offered through 1st Global Capital Corp., Member FINRA, SIPC. Investment Management Solutions (IMS) Platform fee-based asset management accounts offered through 1st Global Advisors, Inc. All other investment management and financial planning services are offered through Reason Financial. Reason Financial and 1st Global are unaffiliated entities.

1st Global is headquartered at 12750 Merit Drive, Suite 1200 in Dallas, Texas 75251; (214) 294- 5000. Additional information about 1st Global is available via the Internet at www.1stGlobal.com.

All opinions expressed and data provided are subject to change without notice. Some of these opinions may not be appropriate to every investor. This commentary should not be considered a solicitation or offering of any investment product. Neither asset allocation nor diversification assures a profit or protects against a loss in declining markets.

Dollar-cost averaging does not assure a profit and does not protect against loss in declining markets.

Past performance is no guarantee of future results. Index performance does not reflect the deduction of any investment-related fees and expenses. It is not possible to invest directly in an index.

The Dow Jones Industrial Average is a price-weighted average of 30 blue chip stocks that are generally leaders in their industry.

The S&P 500 Index is a free-float market capitalization index of 500 large publicly held U.S.-based companies, capturing 80 percent coverage of U.S. equities. It is often used as a proxy for the American stock market.

The Nasdaq Composite Index is a capitalization-weighted index of all Nasdaq National Market and SmallCap stocks.

West Texas Intermediate (WTI) crude oil is the underlying commodity of the New York Mercantile Exchange’s oil futures contracts. Light, sweet crude oil is commonly referred to as oil in

the Western world.

Gross domestic product (GDP) is the monetary value of all the finished goods and services produced within a country’s borders in a specific time period, though GDP is usually calculated on an annual basis. It includes all of private and public consumption, government outlays, investments and exports less imports that occur within a defined territory.

Disclosure

This material is for general information only and is not intended to provide specific advice or recommendations for any individual. There is no assurance the views or strategies discussed are suitable for all investors or will yield positive outcomes. Investing involves risks including possible loss of principal. Any company names noted herein are for educational purposes only.

All information is believed to be from reliable sources; however we make no representation as to its completeness or accuracy. All economic and performance data is historical and not indicative of future results. Market indices discussed are unmanaged. Investors cannot invest in unmanaged indices. Additional risks are associated with international investing, such as currency fluctuations, political and economic instability and differences in accounting standards.

Investing in securities in emerging markets involves special risks due to specific factors such as increased volatility, currency fluctuations and differences in auditing and other financial standards. Securities in emerging markets are volatile and can decline significantly in response to adverse issuer, political, regulatory, market, or economic developments.

An index is a statistical measure of change in an economy or a securities market. In the case of financial markets, an index is an imaginary portfolio of securities representing a particular market or a portion of it. Each index has its own calculation methodology and is usually expressed in terms of a change from a base value. Thus, the percentage change is more important than the actual numeric value. An investment cannot be made directly into an index.

Investing in fixed income securities involves credit and interest rate risk. When interest rates rise, bond prices generally fall. Investing in commodities may involve greater volatility and is not suitable for all investors. Investing in a non-diversified fund that concentrates holdings into fewer securities or industries involves greater risk than investing in a more diversified fund. The equity securities of small companies may not be traded as often as equity securities of large companies so they may be difficult or impossible to sell. Neither diversification nor asset allocation assure a profit or protect against a loss in declining markets. Past performance is not an indicator of future results.

Financial Planning offered through Reason Financial, a state Registered Investment Advisor. Investment advice offered through Merit Financial Group, LLC an SEC Registered Investment Advisor. Merit Financial Group and Reason Financial are separate entities. Tax related services offered through Reason Tax Group. Reason Tax Group is a separate legal entity and not affiliated with Merit Financial Group, LLC. Sean P. Storck CA Insurance Lic#OF25995 and Steven W. Pollock CA Insurance Lic#OE98073

Copyright © 2026 Reason Financial all rights reserved.

Continue Reading

2nd Quarter 2026 – Economic and Market Update

Q1 2026 in review: oil shock, S&P 500 down 4.3%, commodities up 24.4%, the cease-fire that became a blockade — and the planning moves that matter most coming out of a quarter like this one.

It’s Now More Common To Have A Baby In Your Thirties Than In Your Twenties

DisclosureThis material is for general information only and is not intended to provide specific advice or recommendations for any individual.…

When Does Refinancing Actually Make Sense? A 2026 Reality Check

If you locked in a mortgage at 7% or higher in 2023 or 2024, you’ve probably been watching rates with…