July 2019 – An Economic and Market Update

EXECUTIVE SUMMARY

- Markets have performed very well this year which seems to have brought out the recession forecasters, stick to your plan and avoid the noise.

- Congress is currently mulling over two bills which will significantly impact retirement planning in the long run, The SECURE Act (House), RESA (Senate)

- There is likely a low risk of recession in the U.S. at this time but there are a variety of reasons facing the global economy which temper our market expectations for the remainder of 2019.

LOOKING BACK

In Ray Bradbury’s coming of age novel Dandelion Wine, the elderly Mrs. Helen Bentley recalls a conversation with her late husband in reference to holding on to relics of the past, “It won’t work. No matter how hard you try to be what you once were, you can only be what you are here and now.” The context of this quote is a conversation between a group of young children and their elderly neighbor who is trying to point out that she, Mrs. Bentley, was once young like they were. In a rather bratty way, the children deny that she ever could have been as young as them and she must always have been old. This quote reminds us of a lot of what the markets, and headlines about the markets, feel like right now.

On March 13th of this year, reporting came out from CNBC regarding the UCLA Anderson Forecast stating that there is “a very real risk” the national economy will move into recession in late 2020. On April 10th the same news agency reported that Goldman Sachs economists indicate “a chance of recession is now just 10%.” Admittedly, timing is one issue with these two seemingly contradictory claims. Goldman Sachs reference point is out to mid-2020 while UCLA is a slightly longer timeframe of late-2020. The slight difference in timing does not negate the fact we are continually bombarded by contradictory information about the markets as well as a general sentiment that the end of the bull run is right around the corner. Our advice through the noise is to stay true to your plan. Do not let good planning run off the rails just because of confusing forecasts. Today’s bull market will not be what it once was despite new highs. It will be what it is, in the here and now, which is an elderly economic expansion fighting some tough headwinds.,

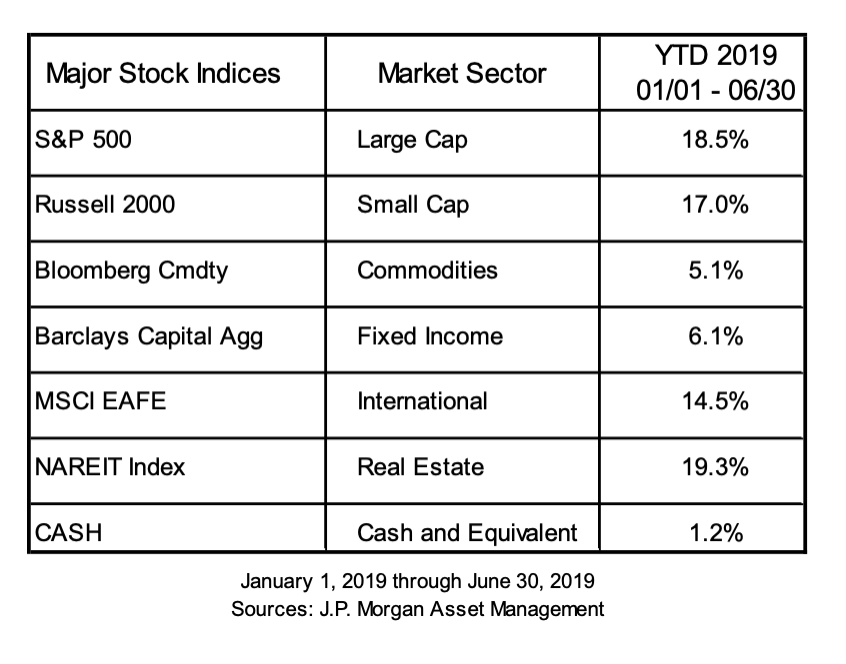

Guide to the Markets – U.S. Data are as of June 30, 2019

Despite that, it has been a good year so far. Interest rate stabilization and risk aversion have strengthened bond markets steadying the fixed income side of investment portfolios. Equity markets have, mostly, held the course in their recovery from the 4th quarter of 2018. Our expectation is that much of the run-up has occurred with new market highs having been set recently. Primarily, our belief is that with trade concerns and continued slowing global growth it will be hard to drive substantial market increases at this time without having economic data turn more positive.

THE PLANNING CORNER

We want to bring your attention to something that is currently being debated in the halls of Congress with significant bi-partisan support. The SECURE Act, before the House of Representatives, and RESA, before the Senate, is meant to broaden a variety of retirement savings options to strengthen the financial footing of Americans as they approach and navigate retirement. We see some positive provisions in these bills, such as removing age restrictions for contributing to IRA’s and delaying RMD requirements as far out as age 75.

We also have concerns that the process of financial planning is going to become more complicated because of one proposal in particular: elimination of the stretch IRA. Under current law, it is possible to pass retirement assets down to non-spousal beneficiaries whereby they have the option to take distributions over their lifetime(s) just as the decedent could. This spreads out the tax burden in addition to making it possible for assets to grow substantially more over time. The proposed changes vary by bill, but the options are for a 5 year or 10-year distribution timeframe with some provisions being made for smaller IRA account balances.

The elimination or modification of the stretch IRA option is a tax revenue issue for the government more than anything else. Under current law it is possible to spread out distributions in such a way that less tax will be remitted over the years than would be paid if larger distributions were forced over a shorter time domain. This is a potentially catastrophic provision for those who have accumulated significant retirement assets with plans to pass those assets down to their beneficiaries.

The likelihood of accelerated distribution requirements on inherited retirement assets being passed into law appears very high. This will increase the complexity of planning significantly for those impacted and makes in-life Roth conversions a better strategy than ever before. If your intent is for your children to inherit retirement assets, we believe it is very important to begin the process of planning for in-life Roth conversions. Long-term tax centric planning is at the core of who we are as a financial planning firm. We strongly encourage you to look realistically at your inheritance plans in order to avoid saddling future generations with potentially painful tax bills which may not be necessary. It is possible to balance your needs today with your plans for tomorrow, it just takes some good planning.

A LITTLE RAIN ON THE MARKET PARADE

Our expectation is that market gains will be tough to come by in the second half of this year. We believe it is an important time to weigh the risk versus reward balance and make rational decisions regarding your investment assets. We do not believe the sky is falling, though we are going to outline below several of the issues we see at hand. In order to keep the discussion positive, we will start with a recent statement by the Richmond Federal Reserve president Tom Barking. “It is hard to have a recession when unemployment is these low and interest rates are this low.”

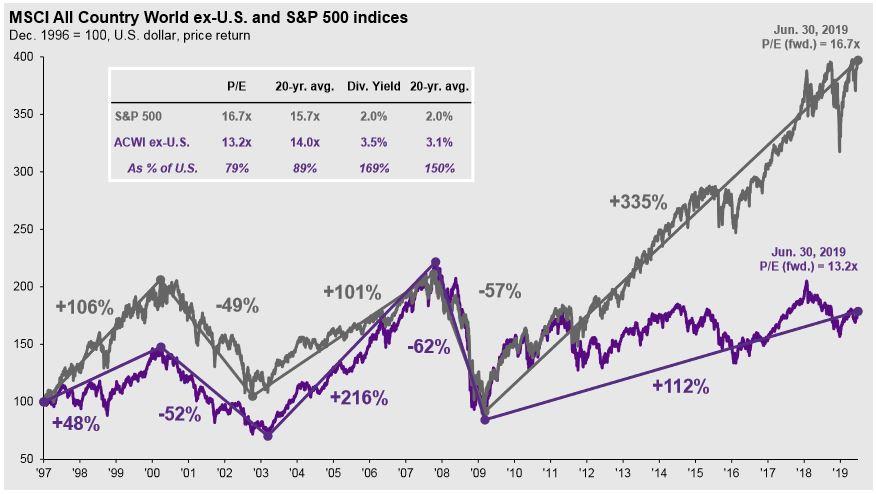

Guide to the Markets- U.S. Data are as of June 30, 2019

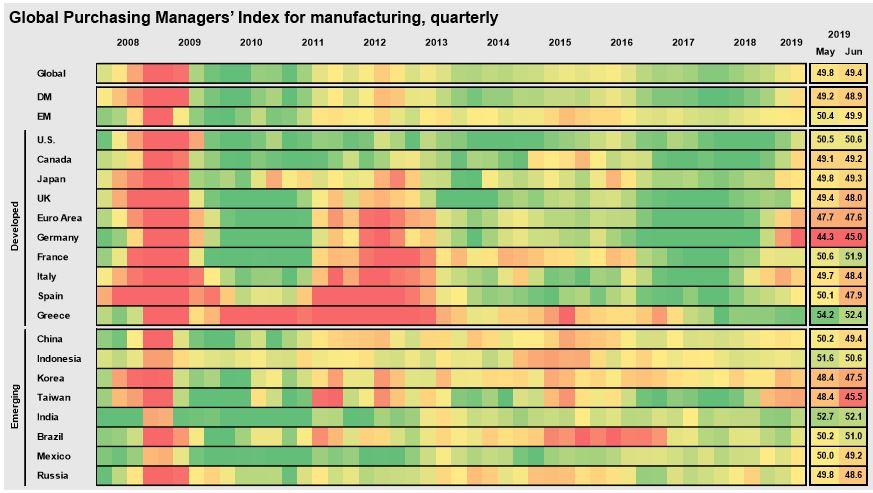

Global growth has slowed down. The global reading of the Purchasing Managers Index at the end of last quarter was holding steady at 50.6, readings over 50 indicate growth. The reading at the end of June of 49.4 indicates a slightly contracting global economy. A variety of data points confirm this change in the status quo.

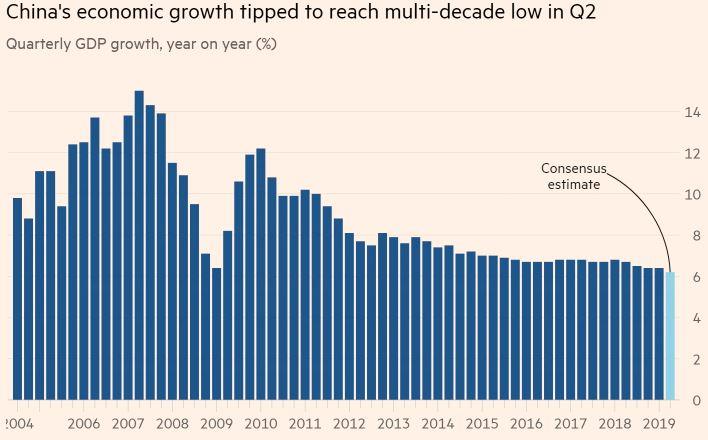

China is likely to experience the slowest expansion since the global financial crisis in 2008/9. Growth may come in higher than consensus, but when juxtaposed with the readings from PMI which indicate a slight slowdown, this is not very likely.

In addition to China slowing, India is facing tough times. According to the Financial Times, “Recent data showed unemployment in India at its worst level in decades, while growth domestic product growth fell to a five-year low of 5.8 percent in the first three months of 2019 compared with 6.6 percent a year earlier.” Additionally, a credit crunch in India is limiting access to capital for the average individual. Looking back to the financial crisis it is easy to see the deleterious effects of a broken credit system.

The United Kingdom finds itself facing its highest recession risk rating since the Financial Crisis, compounded significantly by political turmoil over future leadership and their relationship with the European Union.

Here in the United States tariff issues continue to be front and center. Some of the hardest-hit industries are also being hit by mother nature. Living in California we can sometimes forget that rain is a thing in other parts of the country. Right now farmers in the Midwest have been struggling with one of the wettest years on record causing extremely slow planting seasons. This will likely reduce crop yields due to a variety of factors. Late plantings expose crops to a higher danger of early frost damage. Farmers also will strategically plant varietals which grow faster due to a shorter season, the problem with this is that faster-growing typically means lower yielding. Agriculture is a big business and the tariffs have hit farmers hard. We may see slower growth here in the U.S. if the delayed growing season compounds the troubles already being faced in the form of tariffs. Having recently traveled through the Midwest to visit family, we can attest to the fact that this is the worst start to a growing season we have ever seen. The economic impact at this point is along the lines of a significant hurricane. We will need to wait several months to find out if there are cascading effects from crop failures and low crop yields.

These are just a few of the issues we see impacting economic growth and potentially rattling markets in the second half of the year. It has been a great run in the last six months, but our expectation is for tempered growth through the end of the year. To reiterate the regional Federal Reserve Bank president, it is very hard to have a full-blown recession when unemployment is these low and interest rates are this low. A massive downturn is unlikely, but with markets being forward-looking the issues we have outlined should help to temper our expectations.

COMING TO A CLOSE

Planning is more important then it has ever been. If you are concerned that the projected slowdown may impact your current financial plan please bring this to our attention. We are here to help you make rational, informed and well-reasoned decisions, and we thank you for your continued trust and support. Your input is always welcome, and we ask that you contact us with any questions or concerns.

DISCLOSURE

All information is believed to be from reliable sources; however, we make no representation as to its completeness or accuracy. All economic and performance data is historical and not indicative of future results. Market indices discussed are unmanaged. Investors cannot invest in unmanaged indices. Additional risks are associated with international investing, such as currency fluctuations, political and economic instability and differences in accounting standards.

Investing in securities in emerging markets involves special risks due to specific factors such as increased volatility, currency fluctuations and differences in auditing and other financial standards. Securities in emerging markets are volatile and can decline significantly in response to adverse issuer, political, regulatory, market, or economic developments.

An index is a statistical measure of the change in an economy or a securities market. In the case of financial markets, an index is an imaginary portfolio of securities representing a particular market or a portion of it. Each index has its own calculation methodology and is usually expressed in terms of a change from a base value. Thus, the percentage change is more important than the actual numeric value. An investment cannot be made directly into an index.

Investing in fixed income securities involves credit and interest rate risk. When interest rates rise, bond prices generally fall. Investing in commodities may involve greater volatility and is not suitable for all investors. Investing in a non-diversified fund that concentrates holdings into fewer securities or industries involves greater risk than investing in a more diversified fund. The equity securities of small companies may not be traded as often as equity securities of large companies so they may be difficult or impossible to sell. Neither diversification nor asset allocation assures a profit or protect against a loss in declining markets. Past performance is not an indicator of future results.

Securities offered through 1st Global Capital Corp., Member FINRA and SIPC. Steven W. Pollock, Sean P. Storck, Matthew J. Anderson, and Nicole Albrecht are Registered Representatives of 1st Global Capital Corp. Investment advisory services, including RBFI portfolios offered through Reason Financial. IMS platform accounts offered through 1st Global Advisors, Inc. Reason Financial. and 1st Global Capital Corp. is unaffiliated entities. Reason Financial is a Registered Investment Adviser. Placing business through 1st Global Insurance Services. Registration does not imply a certain level of skill or training. We currently have individuals licensed to offer securities in the states of Arizona, California, Illinois, Indiana, Kansas, Massachusetts, Michigan, New York, Oregon, and Washington. This is not an offer to sell securities in any other state or jurisdiction. CA Department of Insurance License: Steven W. Pollock #OE98073, Sean P. Storck #0F25995, Matthew J. Anderson #0F21959 and Nicole Albrecht #0F99962.

Copyright © 2019 Reason Financial all rights reserved.

Reason Financial

4747 Morena Blvd, Suite 102, San Diego, CA 92117

ENDNOTES

1 Daniels, Jeff. “Economy at ‘Very Real Risk’ of Falling into Recession in Late 2020, UCLA Forecast Says.” CNBC, CNBC, 13 Mar. 2019, www.cnbc.com/2019/03/13/economy-at-very-real-risk-of-entering-recession-in-late-2020-ucla.html.

2 Domm, Patti. “Goldman Sachs Says Chance of a Recession Is Now Just 10%.” CNBC, CNBC, 10 Apr. 2019, www.cnbc.com/2019/04/10/goldman-sachs-says-chance-of-a-recession-is-now-just-10percent.html.

3 Neal, Richard E. “The Setting Every Community Up For Retirement Enhancement Act of 2019.” www.waysandmeans.house.gov, House Committee On Ways & Means, waysandmeans.house.gov/sites/democrats.waysandmeans.house.gov/files/documents/SECURE%20Act%20section%20by%20section.pdf.

4 Sandler, Rachel. “Here’s Why We Suddenly Stopped Hearing About A Recession.” Forbes, Forbes Magazine, 10 May 2019, www.forbes.com/sites/rachelsandler/2019/05/10/heres-why-we-suddenly-stopped-hearing-about-a-recession/#3f8cd4103e37.

5 Lockett, Hudson. “India Car Sales Plunge by a Quarter as Credit Crunch Bites.” Financial Times, Financial Times, 10 July 2019, www.ft.com/content/6a523792-a2f5-11e9-974c-ad1c6ab5efd1.

6 Parkin, Benjamin. “India’s Shadow Banking Crisis Sparks Credit Crunch.” Financial Times, Financial Times, 3 July 2019, www.ft.com/content/4400e274-9638-11e9-8cfb-30c211dcd229.

7 Giles, Chris. “UK at Highest Risk of Recession since 2007, Says Think-Tank.” Financial Times, Financial Times, 13 July 2019, www.ft.com/content/2b2c7022-a486-11e9-974c-ad1c6ab5efd1.

8 “Weekly Weather and Crop Bulletin.” Www.usda.gov, U.S. Department of Agriculture, 16 July 2019, www.usda.gov/oce/weather/pubs/Weekly/Wwcb/wwcb.pdf.

9 Bloch, Sam. “Historic Losses Faced by Nebraska Farmers ‘Will Impact Food on Your Table.’” New Food Economy, 25 Mar. 2019, newfoodeconomy.org/nebraska-south-dakota-wisconsin-flooding-historic-loss-farmers-emergency/.

Disclosure

This material is for general information only and is not intended to provide specific advice or recommendations for any individual. There is no assurance the views or strategies discussed are suitable for all investors or will yield positive outcomes. Investing involves risks including possible loss of principal. Any company names noted herein are for educational purposes only.

All information is believed to be from reliable sources; however we make no representation as to its completeness or accuracy. All economic and performance data is historical and not indicative of future results. Market indices discussed are unmanaged. Investors cannot invest in unmanaged indices. Additional risks are associated with international investing, such as currency fluctuations, political and economic instability and differences in accounting standards.

Investing in securities in emerging markets involves special risks due to specific factors such as increased volatility, currency fluctuations and differences in auditing and other financial standards. Securities in emerging markets are volatile and can decline significantly in response to adverse issuer, political, regulatory, market, or economic developments.

An index is a statistical measure of change in an economy or a securities market. In the case of financial markets, an index is an imaginary portfolio of securities representing a particular market or a portion of it. Each index has its own calculation methodology and is usually expressed in terms of a change from a base value. Thus, the percentage change is more important than the actual numeric value. An investment cannot be made directly into an index.

Investing in fixed income securities involves credit and interest rate risk. When interest rates rise, bond prices generally fall. Investing in commodities may involve greater volatility and is not suitable for all investors. Investing in a non-diversified fund that concentrates holdings into fewer securities or industries involves greater risk than investing in a more diversified fund. The equity securities of small companies may not be traded as often as equity securities of large companies so they may be difficult or impossible to sell. Neither diversification nor asset allocation assure a profit or protect against a loss in declining markets. Past performance is not an indicator of future results.

Financial Planning offered through Reason Financial, a state Registered Investment Advisor. Investment advice offered through Merit Financial Group, LLC an SEC Registered Investment Advisor. Merit Financial Group and Reason Financial are separate entities. Tax related services offered through Reason Tax Group. Reason Tax Group is a separate legal entity and not affiliated with Merit Financial Group, LLC. Sean P. Storck CA Insurance Lic#OF25995 and Steven W. Pollock CA Insurance Lic#OE98073

Copyright © 2026 Reason Financial all rights reserved.

Continue Reading

2nd Quarter 2026 – Economic and Market Update

Q1 2026 in review: oil shock, S&P 500 down 4.3%, commodities up 24.4%, the cease-fire that became a blockade — and the planning moves that matter most coming out of a quarter like this one.

It’s Now More Common To Have A Baby In Your Thirties Than In Your Twenties

DisclosureThis material is for general information only and is not intended to provide specific advice or recommendations for any individual.…

When Does Refinancing Actually Make Sense? A 2026 Reality Check

If you locked in a mortgage at 7% or higher in 2023 or 2024, you’ve probably been watching rates with…