AN ECONOMIC AND MARKET UPDATE – JULY 2023

EXECUTIVE SUMMARY

- American Economy: a surprisingly robust start to 2023.

- Pandemic cash is running out and student loan forbearance is coming to an end.

- Short-term savings and emergency fund alternatives abound; now is a good time to look at how you are holding your money and whether better yielding alternatives are appropriate.

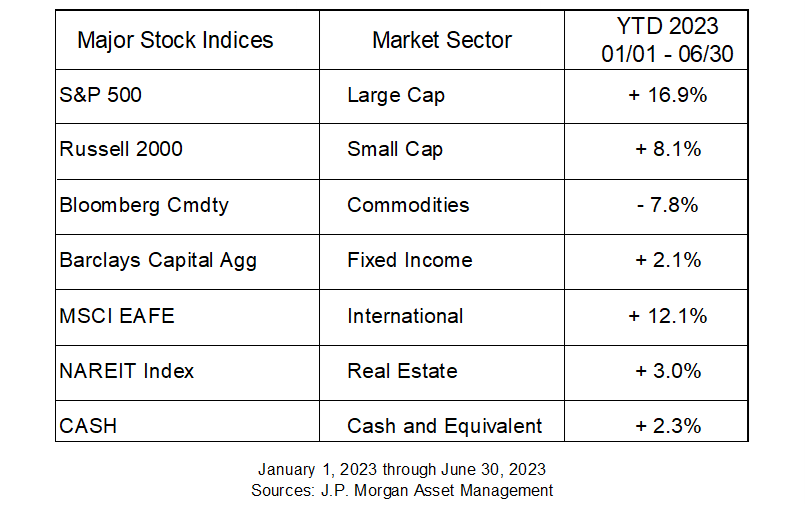

The U.S. economy is proving very resilient. The outlook at the start of the year was for a recession at some point in the second half of 2023. We have not seen the beginnings of a downturn yet, but we are seeing momentum slow. The S&P 500 has rebounded strongly, albeit in a concentrated recovery. Amazon, Apple, Microsoft, Google, and Nvidia have returned 47% while the remaining 495 companies in the S&P 500 have returned only 5% this year. This concentrated return is masking what would otherwise be a rather boring year. We remain committed to maintaining diversity in our portfolio allocation and looking for ways around the lopsided market returns experienced in the mega-cap space.[i]

The second best performer on the year has been international equities. We previously discussed our strategy of shifting portfolio allocations from domestic to international equities over the last two quarters. We have been implementing this strategy change and will continue to review how best to navigate what appears to be a looming domestic slowdown with a recently announced slowdown in Europe.[ii]

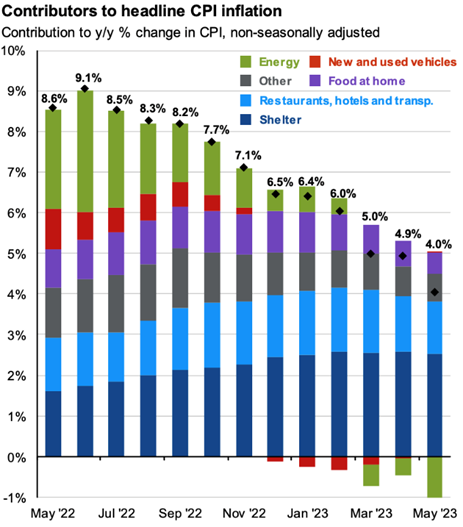

Commodities have been the worst performer year-to-date. The drop in commodity prices have substantially helped the consumer by lowering overall inflation, particularly as it relates to energy prices. We discussed this trend earlier in the year and have seen accelerated reductions in the pricing of energy in particular. Headline CPI is referenced below with energy inflation in green.

Sources: BLS, FactSet, J.P. Morgan Asset Mgmt. Guide to the Markets – U.S. Data are as of June 30, 2023

This is great from an inflationary standpoint. However, it is important to note that pricing is based on the same observed month in the prior year. Recent inflation is calculated based off of June 2022 which was peak inflation to this point in the economic cycle. As you can see in the graph above, Headline CPI is coming down, but if you look at the top end of the bars where the food at home caps out (purple), elements of inflation still remain stubbornly above the desired level of 2%. So, good news, but we still need to see it come down further if we are to expect the Federal Reserve to begin an interest rate reduction cycle. [iii]

STRONG CONSUMPTION BUT CASH CRUNCH AHEAD

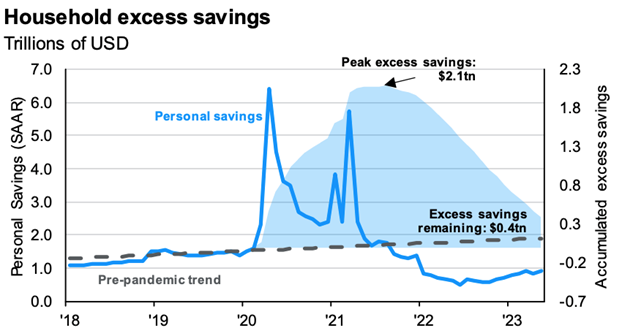

Previously, we discussed “Pandemic Cash” and the savings buffer this allowed for the consumer to build and navigate the last few years of frustration. Two points to make here. First, “Pandemic Cash” is almost out, finally. Second, student loan payments will resume beginning 10/01/23. These two circumstances will likely begin to put pressure on what has been a very resilient consumer over the last couple years.

Excess savings is a bit of a challenge to illuminate, but the easiest place to start is by examining your budget and how you currently think about saving and spending. With younger clients it is often a struggle to fund an IRA or Roth IRA or build up an emergency fund. According to a recent study by New York Life, the average emergency fund in the U.S. was $16,776. This is a big departure from the median figure which indicates that at least 50% of American’s do not have $1,000 saved up for an emergency. It is through this lens we need to look at the next two points.[iv]

Source: BEA, Federal Reserve, J.P. Morgan Asset Mgmt. Guide to the Markets – U.S. Data are as of June 30, 2023

As you can see in the graph above, it is estimated that sometime in the late 3rd or early 4th quarter this year, excess savings will be depleted. While this occurs, Congress passed a law preventing further student loan payment forbearance. The following quote is directly from the USA.gov financial aid and COVID-19 student loan forbearance page:

The Department of Education’s COVID-19 student loan forbearance program is ending. On September 1, 2023, interest resumes, and payments will be due beginning in October 2023.

If you have a student or former student in your life carrying student loans and they are not aware of this change, bring it up. This is a big one. They will be notified of the change, but after 3 years of limited payments this would be an easy payment to miss.[v]

Source: FactSet, FRB, J.P. Morgan Asset Mgmt. Guide to the Markets – U.S. Data are as of 06/30/23

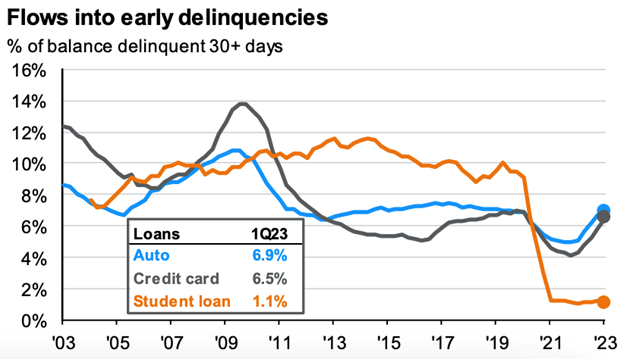

For your average household the resumption of student loan repayments will create a serious reduction in disposable cash. There are various figures out there in regards to the monthly student loan payments. We will use the Education Data Initiative which places the average payment at $503/month. In the graph above you can see that auto and credit card defaults have been on the rise with student loan defaults hanging out at artificially low rates based on COVID rules. We would expect a steep upward trend line in defaults for student loans to begin in the next two quarters. Most households would love to find an extra $6,000/year in their budget. The reverse is not going to be pretty.[vi]

LABOR MARKET STRENGTH

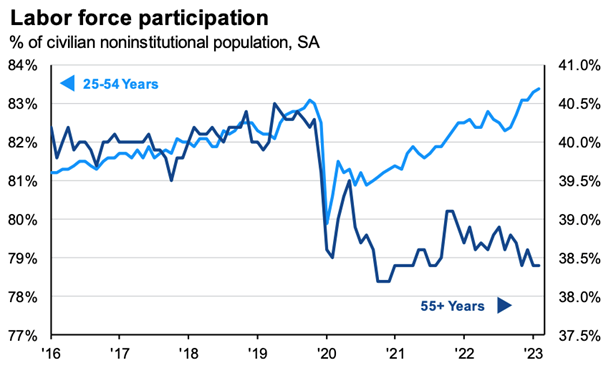

Despite the challenges encountered in the previous year, the labor market has delivered a robust performance. The economy consistently generates jobs at a significant rate, demonstrating the tenacity of the labor market in the face of tight monetary policy moves from the Federal Reserve. However, the pace of job gains has been decelerating, indicating a potential strain. An uptick in labor force participation has been a bright spot, bolstering job growth in recent months.

Source: BLS, FactSet, J.P. Morgan Asset Mgmt. Guide to the Markets – U.S. Data are as of June 30, 2023

This is a trend that will hit the structural limits of an aging demographic, but is exciting nonetheless, with the participation rate for adults between the ages of 25 and 54 fully rebounding to pre-pandemic levels. The participation rate for adults aged 55 and over has remained subdued, reflecting an aging Baby-Boom population experiencing a migration to retirement.

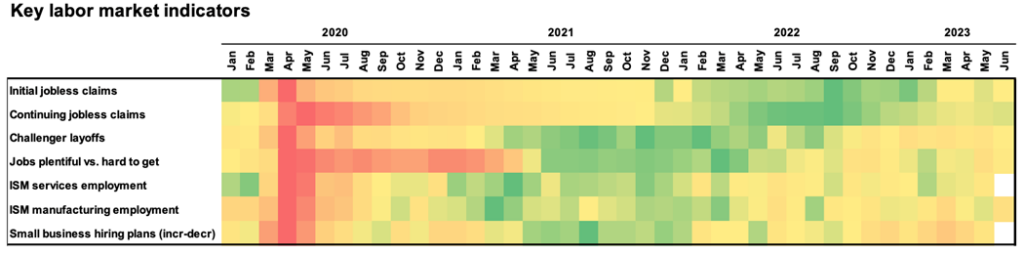

Labor market momentum is slowing. Initial jobless claims have increased and ISM manufacturing employment has taken a hit. None of the general indicators are in the red zone, but a slowdown is taking place. Not all of the data points are in for June 2023 as you can see in the chart below. Wage-driven inflation looks, finally, to be smoothing out. If the current trend continues we expect this to have an impact on how the Federal Reserve views future interest rate increases. To be clear, we are not anticipating a reduction in interest rates during 2023, but we believe it will impact how they view the decision to continue the current pause in rate increases and the size of future rate increases.

Source: BLS, FactSet, Conference Board, ISM, NFIB, J.P. Morgan Asset Mgmt. Heatmap shading is relative to the time period shown. For jobless claims and layoffs, red reflects higher values and green reflects lower values. For ISM employment PMI’s shading is centered at a 50 level, with values above 50 reflecting acceleration (shaded green) and below 50 indicating deceleration (shaded red) of employment. Guide to the Markets – U.S. Data are as of June 30, 2023

THE FED HITS PAUSE – FOR NOW

In his press conference on June 14, 2023, Chairman Powell emphasized that price stability is crucial for the economy to benefit all. This is a continuance of language under the Powell regime emphasizing the need for bull markets and monetary policy to benefit as many people as possible, especially at the margins. Encouragingly, inflation is starting to retreat to more manageable levels. This development arises from a host of interrelated factors. The drop in energy prices, referenced earlier, since the latter half of 2022 has been a significant contributor. Supply chain improvements have also played a role. Additionally, reduced consumer demand across primary goods categories has relieved inflationary pressures. Under the current economic condition two more rate hikes of .25%, 25 basis points, are forecast for the remainder of 2023. Keep an eye on the labor market as it will likely be a major contributor to the Fed outlook on future rate adjustments.[vii]

THE PLANNING CORNER: CURRENT INTEREST RATES VERSUS YOUR SAVINGS ACCOUNT

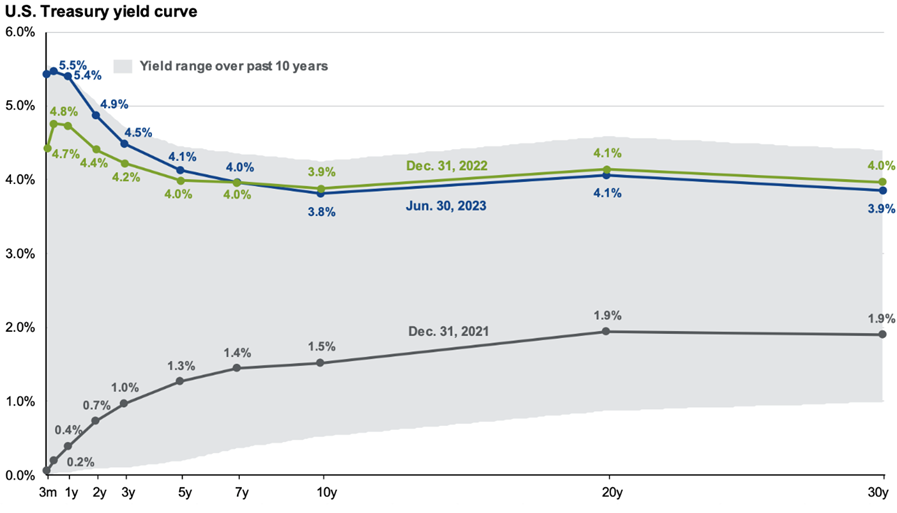

Source: FactSet, Federal Reserve, J.P. Morgan Asset Management, Guide to the Markets: U.S. Data are as of June 30, 2023

The graph above is an updated repeat from last quarter. Short-term interest rates are even better now than they were then. If you are not earning more than 3.5%, we strongly recommend looking at alternative strategies for your cash and emergency funds. The dark blue line is the yield curve as of the end of June. There are reasons to hold money in liquid form such as a checking account. However, continuing to hold your savings or emergency money in a low-interest account is not necessary or advisable under many circumstances. It is our strong recommendation to look at alternatives to a traditional savings account. If appropriate there are many better yielding options at this time.

LOOKING AHEAD

As we navigate through the second half of 2023, it is essential to stay focused on long-term financial goals while being aware of the changing economic landscape. The U.S. economy has shown resilience and investment opportunities persist. However, the outlook suggests a period of slower growth and challenges.

As always, we are here to guide you through these complex dynamics and help you make informed decisions aligned with your financial goals. We appreciate your continued trust and partnership and we welcome any questions or concerns you might have as we advance together.

The economic landscape is ever-evolving, but our commitment to supporting your financial journey remains unchanged. We will continue to closely monitor the situation, adjusting strategies as necessary, and keeping you informed of significant developments that may impact your financial outlook.

DISCLOSURE

All information is believed to be from reliable sources; however we make no representation as to its completeness or accuracy. All economic and performance data is historical and not indicative of future results. Market indices discussed are unmanaged. Investors cannot invest in unmanaged indices. Additional risks are associated with international investing, such as currency fluctuations, political and economic instability and differences in accounting standards.

Investing in securities in emerging markets involves special risks due to specific factors such as increased volatility, currency fluctuations and differences in auditing and other financial standards. Securities in emerging markets are volatile and can decline significantly in response to adverse issuer, political, regulatory, market, or economic developments.

An index is a statistical measure of change in an economy or a securities market. In the case of financial markets, an index is an imaginary portfolio of securities representing a particular market or a portion of it. Each index has its own calculation methodology and is usually expressed in terms of a change from a base value. Thus, the percentage change is more important than the actual numeric value. An investment cannot be made directly into an index.

Investing in fixed income securities involves credit and interest rate risk. When interest rates rise, bond prices generally fall. Investing in commodities may involve greater volatility and is not suitable for all investors. Investing in a non-diversified fund that concentrates holdings into fewer securities or industries involves greater risk than investing in a more diversified fund. The equity securities of small companies may not be traded as often as equity securities of large companies so they may be difficult or impossible to sell. Neither diversification nor asset allocation assure a profit or protect against a loss in declining markets. Past performance is not an indicator of future results.

Sean P. Storck and Steven W. Pollock are registered representatives with and securities and Retirement Plan Consulting Program advisory services offered through LPL Financial, a Registered Investment Advisor. Member FINRA/SIPC. Financial Planning offered through Reason Financial, a state Registered Investment Advisor. Investment advice offered through Merit Financial Group, LLC an SEC Registered Investment Advisor. Merit Financial Group and Reason Financial are separate entities from LPL Financial. Tax related services offered through Reason Tax Group. Reason Tax Group is a separate legal entity and not affiliated with LPL Financial. LPL Financial does not offer tax advice or tax related services. Sean P. Storck CA Insurance Lic#OF25995 and Steven W. Pollock CA Insurance Lic#OE98073

[i] Phillips, Matt. “These Five Companies Are Responsible for S&P 500’s 2023 Gains – Axios.” Axios Markets, 1 June 2023, www.axios.com/2023/06/01/sp500-tech-companies-stock-price.

[ii] Arnold, Martin. “Eurozone Economic Downturn Deepened in July, Business Survey Indicates.” Financial Times, 24 July 2023, www.ft.com/content/69c32792-8759-409b-9ad7-f094b5a508ab.

[iii] Garriga, Carlos, and Devin Werner. “Inflation, Part 3: What Is the Fed’s Current Goal? Has the Fed Met Its Inflation Mandate?” Economic Research – Federal Reserve Bank of St. Louis, 2 Sept. 2022, research.stlouisfed.org/publications/economic-synopses/2022/09/02/inflation-part-3-what-is-the-feds-current-goal-has-the-fed-met-its-inflation-mandate.

[iv] “New York Life Wealth Watch Survey Finds Key Financial Differences among American Families.” Business Wire, 19 Apr. 2023, www.businesswire.com/news/home/20230419005330/en/New-York-Life-Wealth-Watch-Survey-Finds-Key-Financial-Differences-Among-American-Families.

[v] “Covid-19 Student Loan Forbearance (Pause).” USA.Gov, 20 July 2023, www.usa.gov/covid-student-loan help#:~:text=The%20Department%20of%20Education’s%20COVID,extensions%20of%20the%20payment%20pause.

[vi] Hanson, Melanie. “Average Student Loan Payment [2023]: Cost per Month.” Education Data Initiative, 1 June 2023, educationdata.org/average-student-loan-payment#:~:text=The%20average%20monthly%20student%20loan,average%20salaries%20among%20college%20graduates.

[vii] “Transcript of Chair Powell’s Press Conference — June 14, 2023.” Federal Reserve Press Conference, 14 June 2023, www.federalreserve.gov/mediacenter/files/FOMCpresconf20230614.pdf.