April 2015 – An Economic and Market Update

EXECUTIVE SUMMARY

• Domestic markets are being pressured by lower consumption readings despite low energy prices putting more money in consumer pockets. ,

• Despite much hype over the aging of the American population, the U.S. demographic makeup is very encouraging when compared to many of the other developed and developing countries in the world.

• The current and projected Saver vs. Borrower ratio provides perspective on why a low interest rate environment may continue in the future as more and more savers compete for fewer borrowers.

LOOKING BACK – MAJOR STOCK INDICES YTD 2015

January 1, 2015 through March 31, 2015

S&P 500: +1.00%

Russell 2000: +4.30%

Bloomberg Cmdty Index: -5.9%

Barclays Bond Agg: +1.6%

MSCI EAFE +5.0%

NAREIT Index +4.0%

(Source: JP Morgan Asset Management)

The first quarter brought little in the way of comfort for investors as the stock markets experienced see-saw like action in most asset classes. Investors were rewarded however for their continued commitment to the developed international markets which performed considerably better than they have in some time.

In general the markets seemed to be searching for direction during the first quarter of 2015. While there are always many factors that impact market movements, Consumers and the Fed have been front and center. Despite positive income growth and significantly lower energy prices, consumption has been flat and inventories have continued to rise. At the same time, the Federal Reserve continues to go back and forth on when a rate increase will occur.

THE RISE OF THE MILLENIAL

As a society we give a lot of attention to the Baby Boom generation. After all, there are 76.4 million Baby Boomers, holding 50% of investable assets and over the next twenty years they will dramatically shift the landscape of the country as they move out of the workforce and into retirement. Numerous articles, research and dissertations have been written discussing the opportunities and challenges this will present our country and the world. However, the discussion often pays little attention to the incredibly positive position we as a country find ourselves in.

Different population cohorts (groups or in this case generations) have different characteristics.

Baby Boomers – age 50 and above – are what economists consider “Net Savers” or those that have moved from consumption/borrowing to savings/lending. By and large the Baby Boomer generation is past the hyper consumption lifestyle during which they were buying homes, raising families, paying taxes and financing college tuitions.

Generation X – early 30’s to 50 – are the new “Net Borrowers” and economists consider these to be the major consumption group in the economy. Generation X has replaced the Boomer and it is now their turn to play the role of hyper consumer and taxpayer.

The Millennials – Late teens to early 30’s – are the tail end of the “Net Borrowers” and just beginning to enter into the hyper consumer class. Millennials are characterized as having been shaped by technology, constant connectedness and social media.

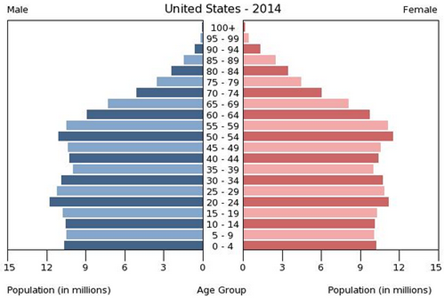

It is important to note the size of these different generations, how they are represented in the “population tree” below and the characteristics of each group as defined earlier.

Source: CIA World Factbook

The distribution of population among the different cohorts indicates that The United States appears to be in an advantageous position moving forward. Millennials will not reach the same proportional peak percentage of the population as Baby Boomers did at their height, but they will outnumber Boomers in absolute terms.

This means that the future of the United States will be driven by the largest (by number) population cohort in the history of the country. The next 40 years of the economy will be fueled by this larger population base paying taxes, driving consumption, and supporting the development of infrastructure, social programs, college funding, research and development, etc.

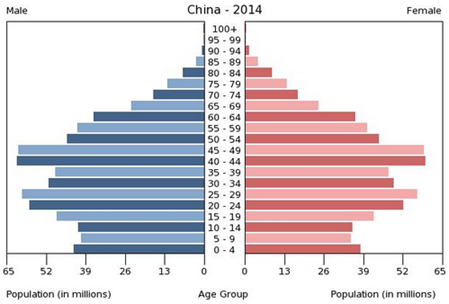

Source: CIA World Factbook

Source: CIA World Factbook

In comparing China to the United States there are several key differences in population makeup. China with a high number of Baby Boomers/Old Gen X’ers has a significant problem to address as this cohort retires and moves from the borrower/consumer to the savers. By all appearances there is not enough Gen X to bridge the gap to Millennials after which the population experiences a significant decline. At that point long run concerns surrounding the tax and consumption base necessary to fund social programs and a healthy economy become very real.

WHAT DOES THIS MEAN FOR INTEREST RATES

WHAT DOES THIS MEAN FOR INTEREST RATES

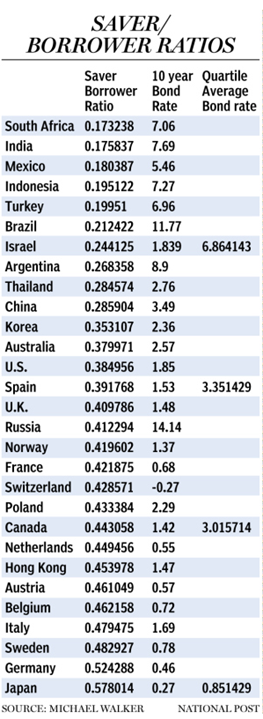

Every quarter the collective financial world closely watches the Federal Reserve to see if any hint of interest rate movements will be announced. While The Federal Reserve sets rates for interbank lending there is also a real world economy comprised of many individuals asking to borrow money from those with money to lend. In this most simplistic sense a traditional supply and demand market exists. More Savers leads to a surplus of lendable dollars requiring lower interest rates to attract Borrowers.

The relative proportion of Savers/Borrowers in a society has a lot to do with this process. According to economist Michael Walker, former executive director of the Fraser Institute, “It’s time to abandon the notion that world interest rates are going back up to historic levels – at least in countries that have migrated into the Borrower’s market end of the demographic spectrum.”

Again this seems to bode well for the United States. We will likely have more balanced population demographics as seen earlier in the population tree and now again in a more rudimentary measurement of Savers/Borrowers. Our expectation is that rates will rise over time, but that any rise in rates will be tempered by the fact that this is a Borrowers market not a Savers.

LOOKING FORWARD

The United States is well-positioned for long term growth. While generational differences will always exist, we are on the precipice of seeing how Millennials will shoulder their responsibilities. Our diverse population, and economy coupled with our free-market philosophy should allow us to continue to adjust as world economic conditions evolve.

We remain committed to the protection of your assets and the growth of your investment portfolio. Our focus is to protect value, provide you with trusted advice, and assist you and your family in making good decisions.

We thank you for your continued trust and support. Your input is always welcome and we ask that you contact us with any questions or concerns.

DISCLOSURE

All information is believed to be from reliable sources; however we make no representation as to its completeness or accuracy. All economic and performance data is historical and not indicative of future results. Market indices discussed are unmanaged. Investors cannot invest in unmanaged indices. Additional risks are associated with international investing, such as currency fluctuations, political and economic instability and differences in accounting standards.

Investing in securities in emerging markets involves special risks due to specific factors such as increased volatility, currency fluctuations and differences in auditing and other financial standards. Securities in emerging markets are volatile and can decline significantly in response to adverse issuer, political, regulatory, market, or economic developments.

An index is a statistical measure of change in an economy or a securities market. In the case of financial markets, an index is an imaginary portfolio of securities representing a particular market or a portion of it. Each index has its own calculation methodology and is usually expressed in terms of a change from a base value. Thus, the percentage change is more important than the actual numeric value. An investment cannot be made directly into an index.

Investing in fixed income securities involves credit and interest rate risk. When interest rates rise, bond prices generally fall. Investing in commodities may involve greater volatility and is not suitable for all investors. Investing in a non-diversified fund that concentrates holdings into fewer securities or industries involves greater risk than investing in a more diversified fund. The equity securities of small companies may not be traded as often as equity securities of large companies so they may be difficult or impossible to sell. Neither diversification nor asset allocation assure a profit or protect against a loss in declining markets.

Past performance is not an indicator of future results.

Securities offered through 1st Global Capital Corp., Member FINRA and SIPC. Bruce Rawdin-Baron, Steven W. Pollock, Sean Storck and Nicole Albrecht are Registered Representatives of 1st Global Capital Corp. Investment advisory services, including RBFI portfolios offered through Rawdin-Baron Financial, Inc. IMS platform accounts offered through 1st Global Advisors, Inc. Rawdin-Baron Financial, Inc. and 1st Global Capital Corp. are unaffiliated entities. Rawdin-Baron Financial, Inc. is a Registered Investment Adviser. Placing business through 1st Global Insurance Services. Registration does not imply a certain level of skill or training. We currently have individuals licensed to offer securities in the states of Arizona, California, Illinois, Indiana, Kansas, Massachusetts, Michigan, New York, Oregon and Washington. This is not an offer to sell securities in any other state or jurisdiction. CA Department of Insurance License: Bruce Rawdin-Baron #0736631, Steven W. Pollock #OE98073, Sean Storck #0F25995 and Nicole Albrecht #0F99962.

Copyright © 2015 Rawdin-Baron Financial Inc., all rights reserved.

Rawdin-Baron Financial, Inc., 4747 Morena Blvd, Ste 102, San Diego, CA 92117

Disclosure

This material is for general information only and is not intended to provide specific advice or recommendations for any individual. There is no assurance the views or strategies discussed are suitable for all investors or will yield positive outcomes. Investing involves risks including possible loss of principal. Any company names noted herein are for educational purposes only.

All information is believed to be from reliable sources; however we make no representation as to its completeness or accuracy. All economic and performance data is historical and not indicative of future results. Market indices discussed are unmanaged. Investors cannot invest in unmanaged indices. Additional risks are associated with international investing, such as currency fluctuations, political and economic instability and differences in accounting standards.

Investing in securities in emerging markets involves special risks due to specific factors such as increased volatility, currency fluctuations and differences in auditing and other financial standards. Securities in emerging markets are volatile and can decline significantly in response to adverse issuer, political, regulatory, market, or economic developments.

An index is a statistical measure of change in an economy or a securities market. In the case of financial markets, an index is an imaginary portfolio of securities representing a particular market or a portion of it. Each index has its own calculation methodology and is usually expressed in terms of a change from a base value. Thus, the percentage change is more important than the actual numeric value. An investment cannot be made directly into an index.

Investing in fixed income securities involves credit and interest rate risk. When interest rates rise, bond prices generally fall. Investing in commodities may involve greater volatility and is not suitable for all investors. Investing in a non-diversified fund that concentrates holdings into fewer securities or industries involves greater risk than investing in a more diversified fund. The equity securities of small companies may not be traded as often as equity securities of large companies so they may be difficult or impossible to sell. Neither diversification nor asset allocation assure a profit or protect against a loss in declining markets. Past performance is not an indicator of future results.

Financial Planning offered through Reason Financial, a state Registered Investment Advisor. Investment advice offered through Merit Financial Group, LLC an SEC Registered Investment Advisor. Merit Financial Group and Reason Financial are separate entities. Tax related services offered through Reason Tax Group. Reason Tax Group is a separate legal entity and not affiliated with Merit Financial Group, LLC. Sean P. Storck CA Insurance Lic#OF25995 and Steven W. Pollock CA Insurance Lic#OE98073

Copyright © 2026 Reason Financial all rights reserved.

Continue Reading

2nd Quarter 2026 – Economic and Market Update

Q1 2026 in review: oil shock, S&P 500 down 4.3%, commodities up 24.4%, the cease-fire that became a blockade — and the planning moves that matter most coming out of a quarter like this one.

It’s Now More Common To Have A Baby In Your Thirties Than In Your Twenties

DisclosureThis material is for general information only and is not intended to provide specific advice or recommendations for any individual.…

When Does Refinancing Actually Make Sense? A 2026 Reality Check

If you locked in a mortgage at 7% or higher in 2023 or 2024, you’ve probably been watching rates with…