April 2016 – An Economic and Market Update

An Economic and Market Update

EXECUTIVE SUMMARY

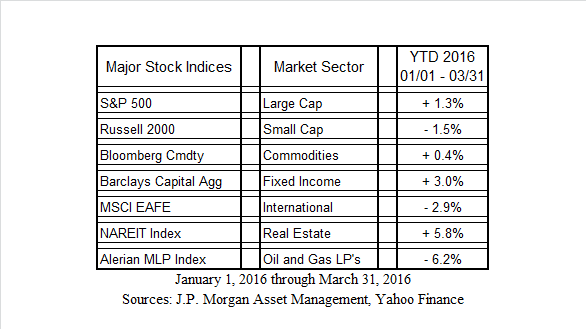

- The 1st quarter of 2016 presented investors with an initial period of sharp market drawdowns followed by steady recovery through the end of the quarter.

- The state of the labor market is a popular discussion topic for Presidential candidates with some sounding the alarm over low labor participation and others trumpeting the low unemployment rate. The truth, as usual, is a little more complicated.

- The Department of Labor introduced additional regulation covering financial advisers. The Fiduciary Rule, as it is called, is a complicated rule which will take time to sort out but should help to make the financial service industry more transparent regarding level of care and cost.

LOOKING BACK

The 1st quarter of 2016 was a good reminder of the emotional roller-coaster we endure through the peaks and valleys of a market cycle. Since reaching the bottom on February 11th marking 13.3% in market drawdown, the S&P 500 has managed a steady recovery providing a positive 1.3% end of quarter return. Oil and Natural Gas carried over downward trajectory from 2015 with most experts believing we may continue to see energy price volatility over the short-term.[i]

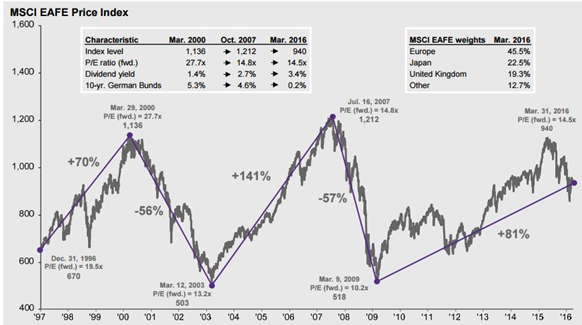

The Eurozone, China, and other developed foreign economies have not experienced the level of market and economic recovery necessary to return to pre-recession measures as indicated in the chart below. In fact, stagnant growth in international economies continues to be an area of heightened concern. Christine Lagarde, Managing Director of the International Monetary Fund (IMF), recently warned that, “the not-so-good news is that the recovery remains too slow, too fragile, and risks to its durability are increasing.”[ii]

Source: Compustat, FactSet, Standard & Poor’s, J.P. Morgan Asset Management

Guide to the Markets – U.S. Data are as of March 31, 2016

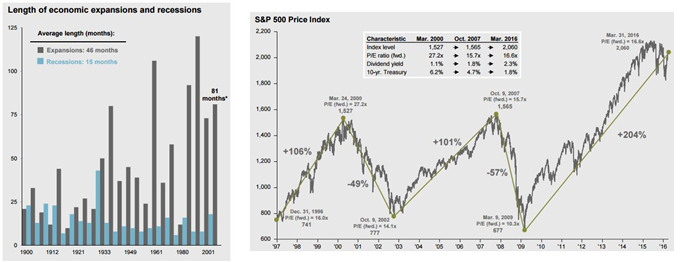

Meanwhile, the expansionary market the U.S. has been in since July 2009 is in its 81st month and stands at 4th all-time in duration. This fact makes it feel like the recovery is getting a bit “long in the tooth”, historically speaking, viewed through a lens of referencing present day events to those of the past.[iii]

Source: BEA, NBER, J.P. Morgan Asset Management Source: Compustat, FactSet, Standard & Poor’s, J.P. Morgan Asset Management Guide to the Markets – U.S. Data are as of March 31, 2016

We believe it is important to place recent volatility within the context of lagging international markets and continued price disruption in the oil & gas industry. Domestics markets are not an island unto themselves and some level of volatility is to be expected if our international peers and oil markets continue struggling.

THE ELECTION CYCLE

Five individuals remain in the Presidential Election cycle which originally included a list of 23 serious candidates: 17 Republican and 6 Democratic. In the long sprint to November 8th, we anticipate being subject to any number of speeches and discourses on a host of topics including: how to fix the tax system, boost employment, decrease the budget deficit, accelerate GDP, and so on. Most of what we will hear is rhetoric designed to inflame passions and generate votes. An area we will take a few minutes to ruminate on is employment and labor participation as it is likely to be discussed quite a bit.[iv]

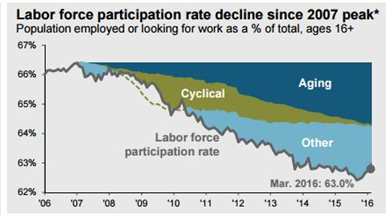

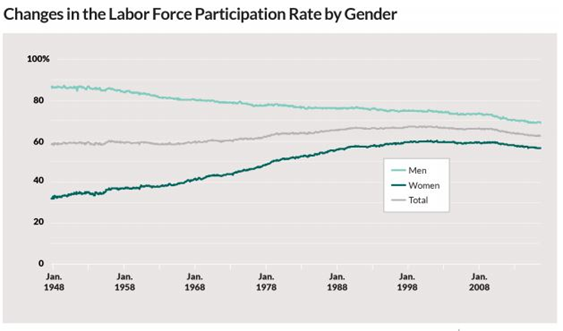

The United States is currently experiencing a 5% Unemployment Rate which is well below the 50 year moving average of 6.2%. There are those who will discount this rate of unemployment by referencing data contained in the Labor Force Participation Rate graph below. It is important to note that since the “Great Recession” the Cyclical Factors contributing to the downturn in Labor Force Participation have mostly been worked out of the system, despite what we may hear from the politicians currently pandering for our votes. We are left with the more persistent problems.[v]

Source: Bureau of Labor Statistics, FactSet, J.P. Morgan Asset Management

Labor Force Participation is a simple idea with a complex sum of inputs driving participation. Quite simply, it is the percentage of the working age population that is actively part of the labor force. People fall in and out of the labor force for reasons as varied as raising children, taking care of elderly parents or relatives, illness, educational attainment, and so on. We do have a labor force participation problem – but it is not new, nor is it young.[vi]

Source: Washington Center for Equitable Growth, US. Dept of Labor, BLS, Current Population Survey.

In testimony before Congress on July 15, 2015 Elisabeth S. Jacobs, the Senior Director for Policy and Academic Programs at the Washington Center for Equitable Growth, discussed the complex issue of Labor Force Participation. In her testimony she outlined a variety of factors contributing to the participation problem and the myriad solutions which, when put together, could improve the situation.[vii]

Men have been a declining presence in the labor force for sixty (60) years and women have had a declining presence since flat-lining in the 90’s, long before the Great Recession. Solutions posed have been to make work more flexible, allow for universal pre-kindergarten education, augmented family-friendly policies, criminal justice reform reducing incarceration and the attached stigma, and so on. The point being, there are no easy solutions and every solution will without doubt create another problem needing a solution. Ms. Jacobs ended her testimony with the following: “The trick for policymakers is to be strategic, and to pull the levers with the most potential to jump-start the labor market back into high gear.”[viii]

Our hope for this election cycle is that on November 8th we ultimately get to choose between two candidates well-suited to being the “strategic” mind necessary to engineer a solution to our Labor Force stagnation.

LOOKING FORWARD

The Federal Reserve seems to be losing some conviction in their rate-increase strategy. In fact, the Atlanta Federal Reserve President, Dennis Lockhart, recently stated that “based on what I’ve [sic] seen recently, I am not going to be advocating a move in April.” This is not unexpected but is easily viewed as a concession in the face of consumer spending data indicating a slow-down, and other indicators being weak. Our expectation is for another minor increase this year continuing a slow upward pace in the move of interest rates off the bottom.[ix]

Many have asked our opinion about the Fiduciary Rule recently passed by The Department of Labor. We welcome this change to the financial industry and are hopeful it will make our industry more transparent by holding everyone to the same standard. In fact, this rule really forces others in our industry to be subject to the fiduciary level of care we have operated under for many years by virtue of being a Registered Investment Advisory Firm and/or Certified Financial Planning™ professionals. More legislation is sure to come as this rule is picked apart and we welcome any questions you might have along the way.

We remain committed to the protection of your assets and the growth of your investment portfolio. Our focus is to protect value, provide you with trusted advice, and assist you and your family in making a lifetime of rational, informed and well-reasoned financial decisions. We thank you for your continued trust and support. Your input is always welcome and we ask that you contact us with any questions or concerns.

ENDNOTES

[i] Osterland, Andrew. “Energy Outlook for 2016: Looking for a Bottom.” Advisor Insight. CNBC.com, 2 March 2016. Web. 16 Apr. 2016. http://www.cnbc.com/2016/03/02/energy-outlook-for-2016-looking-for-a-bottom.html

[ii] Lagarde, Christine. “Decisive Action to Secure Durable Growth.” Joint event by Goethe University and the Bundesbank. Goethe University, Frankfurt, Germany. 5 April 2016. Lecture.

[iii] Compustat, FactSet, Standard & Poor’s, J.P. Morgan Asset Management

Guide to the Markets – U.S. Data are as of March 31, 2016

[iv] “Democratic Party presidential candidates, 2016.” Wikipedia: The Free Encyclopedia. Wikimedia Foundation, Inc. 15th Apr. 2016. Web. 18th Apr. 2016. https://en.wikipedia.org/wiki/Democratic_Party_presidential_candidates,_2016

[v] Source: Bureau of Labor Statistics, FactSet, J.P. Morgan Asset Management

[vi] Bureau of Labor Statistics

[vii] Jacobs, Elisabeth. “The Declining Labor Force Participation Rate: Causes, Consequences, and the Path Forward.” Congressional Testimony. Washington, DC: The Washington Cernter for Equitable Growth, 15 Jul. 2015.

[viii] Jacobs, Elisabeth. “The Declining Labor Force Participation Rate: Causes, Consequences, and the Path Forward.” Congressional Testimony. Washington, DC: The Washington Cernter for Equitable Growth, 15 Jul. 2015.

[ix] Hays, Kathleen. Interview with Dennis Lockhart. Bloomberg Television. 2016. Web. 14 Apr. 2016.

DISCLOSURE