April 2021 – Economic and Market Update

Executive Summary

- Markets are responding well to vaccination progress and consumers are returning to more normal behavior.

- Inflation is a real thing, but something we have not experienced significantly in a long time. As such, it appears to be misunderstood and a bit too feared.

The start of 2021 has seen its fair share of craziness on the markets, however, as the months have ticked by normalcy has returned. The indexes are performing better than last years hot stock picks and the battle over social media famous stocks has abated (think Gamestop). Fixed income is in the middle of the roughest patch it has seen in a very long time, which is not surprising given the interest rate environment we are in, coupled with inflation concerns. To put this into perspective, core fixed income has only ended the year down once in the last 15 years, back in 2013, when interest rates began to rise coming out of the financial crisis, and it looks like it may do it again. We are receiving a lot of questions about how we will handle a rising interest rate environment with potentially high inflation, so we will address these concerns later in our update. Valuations aside, the markets appear to be pricing in the large fiscal stimulus packages and an enthusiastic reopening of the country.

The U.S. is looking good on two fronts: new confirmed cases and total vaccinations. As you can see in the graphs below our current situation is favorable, particularly as it relates to COVID-19 vaccinations.

Our confirmed case rate has tapered up a bit in the last month, however, we are not seeing the exponential growth of the post-holiday time period. Fed Chair Powell recently communicated the tentative position we are in: “we’re clearly on a good path with, with cases coming down, as I mentioned but we’re not done.” His response was to a journalist questioning whether or not herd immunity projections and full-employment timelines would coincide and if policymakers needed to do more to get them in alignment. Basically, have we done enough or do we need to do more? Reading between the lines – no one really knows, but you should expect continued aggressive action until herd immunity is reached, but please don’t let your guard down.

Based on the graph above, hopefully, we will find ourselves in herd immunity range before too long. What we can say is that high-frequency economic data for the last two months show the confidence of people to get out and about has increased dramatically. The data is trending up.

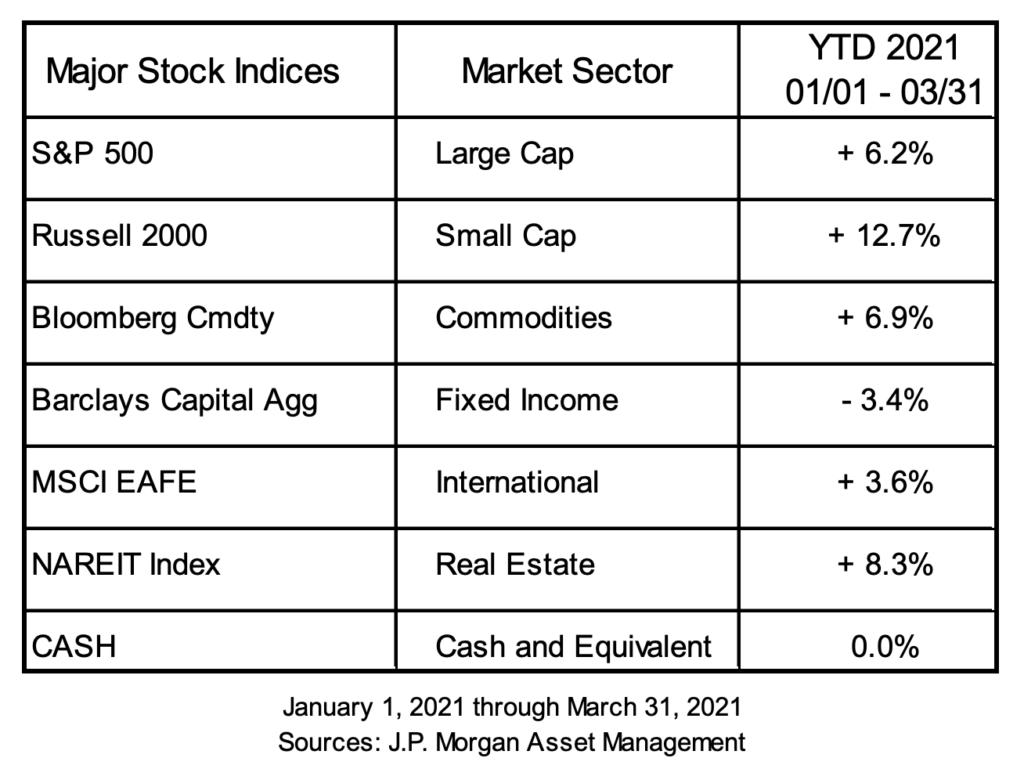

Guide to the Markets – U.S. Data are as of March 31, 2021

As the data trends positive, more people will continue to resume normal life with a lot of pent up demand and cash to burn. After a year of not spending much, and receiving large stimulus checks, there will be a lot of money chasing too few goods due to still constrained supply lines. This situation will eventually lead to inflation and rising interest rates. Leading to one of the more popular questions we have had to answer, and Chair Powell of the Federal Reserve as well, how high will inflation get?

Hyperinflation or something else

Are we going to go over the edge with inflation? The short answer is that it is very unlikely. Do we think we could go through a period of above average inflation? Yes.

The rhetoric we hear surrounding the future of inflation seems hyperbolic at best, and fear mongering at worst. Meaning, it sounds something like this, “hyperinflation is coming so you need to buy gold, or cryptocurrency, or xyz something or other”, as if there is a special amulet that will inherently provide protection against hyperinflation. In order to put hyperinflation in its proper context you first need to look at several modern examples to understand the ingredients which are necessary. For the sake of ease we will over-simplify the scenarios, please forgive us for that:

Germany Post WWI – The Weimar government misses a WWI reparations payment leading to occupation and confiscation of assets by the French. In turn, the government attempts to print money to get out of the crisis leading to political instability and hyperinflation, and the rise of the Nazi party.

Yugoslavia 1992 – After the fall of Communist Russia and subsequent failure of communist policies in former USSR countries money-printing was used to finance high deficits leading to hyperinflation.

Zimbabwe 2007 – Money-printing policy initiated to finance large deficits caused by ill-advised economic policies, such as land redistribution, leads to hyperinflation.

North Korea 2009 – Poorly executed currency reform by the communist dictatorship leads to hyperinflation and the black market in non-Won currency experiences skyrocketing prices for basic goods such as rice.

Venezuela 2016 – After the death of Hugo Chavez, the long tenured leader (dictator) of Venezuela, money-printing and deficit spending lead to hyperinflation amongst widespread civil disruptions directed at replacing the Chavez-installed Maduro regime.

In all instances, there existed a lack of trust in the government to provide stability, massive unemployment, and large government deficits financed by printing money. The lack of trust is not of the garden variety skeptiscm exhibited by many Americans. It is more of the burn it all to the ground and start fresh variety.

In short, hyperinflation is much less about the value of goods than it is about the perception of the current government to function and provide stability. The United States Dollar remains the standard reserve currency of the world. We remain, arguably, the most productive and wealthy nation in the history of the world. We have a free market, generally speaking, where competitiveness reigns and the best of the best rise to the top. A saying frequently attributed to Winston Churchill, but more accurately attributed to Israeli diplomat Abba Eban, comes to mind, “Men and nations behave wisely when they have exhausted all other resources.” We are in the midst of significant trials, we have exhausted all other alternatives, and we believe firmly in the ability of our country to move wisely forward as we are rapidly reaching the end of the ability to act otherwise.

Something else

It is our belief we will see a period where inflation will rise more rapidly than anything we have experienced in the past 20 to 30 years. We believe this will be a short phase marked by relatively high inflation in comparison to recent historical norms. It is not our expectation that we will see anything like what we saw in the early 80’s where inflation was as high as 14.76% in April of 1980. There is a lot of uncertainty but we expect to see inflation touch a high somewhere in the 3% to 5% range. Whether this period lasts for a quarter or a year is an unknown, but we believe it will be short-lived. To quote from the Fed Meeting Notes, “the median inflation projection of FOMC participants is 2.4 percent this year and declines to 2 percent next year before moving back up by the end of 2023”. To help illustrate we are bringing back Little Jane.,

Little Jane, of our favorite lemonade stand, has experienced something similar. The local lemon growers she relies upon for her lemons had a very poor growing season, and as a result the lemon supply has grown quite tight. Unfortunately for Jane, this means she and all her competitors have been fighting for the low supply of lemons to keep their stands stocked to provide beverages for their patrons, driving up the price of lemons. Doubly unfortunate for her, is the fact that there are no current importers of lemons from neighboring regions. However, lemon growers from the neighboring states have heard of the price increase and are rapidly building up the transportation infrastructure necessary to get their lemons into Little Jane’s market. She is excited for that to happen, because she knows that as soon as the supply problem is met, the now increased number of suppliers will create a glut of lemons on the market and prices will once again come down. In fact, with increased competition it is possible the prices might settle in lower than what she was paying before as the local growers now have to compete with growers from other regions. In the short term, things look a little painful, but in the long run, things are looking up for Little Jane.

Our argument for this case is rooted in the experience of the last decade. The 2010’s saw previously unprecedented increases in fiscal and monetary expansion. During that time period inflation remained tepid and below the target set by the Federal Reserve. The forces at play then in regards to population demographics and technological innovation, are still at play now.

In fact, the Federal Reserve balance sheet roughly quadrupled in the years after the financial crisis versus roughly doubling in the last year of the pandemic. In his most recent address Fed Chair Powell addressed the challenges with increasing inflation since the Financial Crisis when he said, “So we’ve said we’d like to see inflation run moderately above two percent for some time…part of that just is, talking about inflation is one thing; actually having inflation run above two percent is the real thing…over the years we’ve talked about two percent inflation as a goal, but we haven’t achieved it.” Inflation was not a thing after quadrupling the Fed balance sheet, albeit without the level of fiscal stimulus we have seen in the last year. Assuming, rampant inflation is going to be a thing after a decade of tepid inflation is not, therefore, a reasonable assumption to make. Our current expectation is for inflation to run a bit more aggressive than the conservative projections of the Fed based on the speed in which the current set of stimulus plans was implemented as you will see in the graph below.

As the restocking and reopening of the world continues to accelerate, there is certainly pent up demand and a higher likelihood of too many dollars chasing too few goods, leading to inflation. The supply problem will work itself out, just like in the case of Little Jane, as supply ramps back up to full capacity and additional competitors or alternatives enter the marketplace, prices should come back down. There are constraints to how high it can run, however, in that you can only go out to eat so many times per day, live in so many houses, and go on so many vacations. Constraints exist, and those constraints, in the absence of abject failure by the government, will lead to stabilization of inflation in the short to intermediate term.

To put the money printing in context, without diving too deeply into the varying definitions of what constitutes money supply, we find the graph below useful.

Guide to the Markets – U.S. Data are as of March 31, 2021

As you can see, coming out of the Financial Crisis the Federal Reserve took roughly the same set of tactics they are taking now, albeit spread out over a longer period of time. Treasury volume was increased, Mortgage Backed Securities (MBS) were increased, and other miscellaneous means of stimulating the economy were made. Different decade, same tactics. This is not to say the piper will not have to be paid someday, it just is unlikely to be in the very near future. The piper has very long payment terms, until she doesn’t.

The next year or two will prove a trying time period for fixed income investors. As inflation rises the expectation is that interest rates will need to rise to keep inflation in check. This will negatively impact fixed income investments. The course we are plotting is to keep duration short and risk as diversified and low as possible. Our core fixed income portfolio is overweight short duration bonds at this time, and we are disinclined to make a change to that strategy right now. To date we have been successful as our fixed income portfolios have treaded water while the Barclays Aggregate Bond Fund is down 3.4%. We will continue to work hard to balance the teeter-totter that is yield versus interest rate and duration risk.

The Planning Corner

The over arching theme for us right now is that projections moving forward look good. A combination of government spending and enthusiasm for reopening should keep the economy moving at a higher rate than we would normally see. A large part of this has to do with a successfull vaccine strategy relative to most of the rest of the world. Out of all major developed nations, only Israel and the United Kingdom have a higher vaccination rate than the United States, and we are climbing higher faster. The U.S. is dramatically past our other global peers in terms of getting “jabs” into arms as it has come to be known colloquially. We are not sure where the term “jabs” became the accepted terminology, but it is.

Most economic indicators right now are a greenlight for go. In the absence of substantial setbacks in the fight against COVID-19, we believe that we should be in a good position a year from now relative to today.

There is a lot of legislation being talked about at this time which we will certainly begin to work into our thought processes as clarity is provided by legislative bodies. These include:

- SECURE Act 2.0 (Securing a Strong Retirement Act).

- The American Jobs Plan (Infrastructure Bill) – currently a $2 Trillion proposal.

- Tax Reform – lots of speculation at this time, not a lot of meat.

As always, our desire is to help you make rational, informed and well-reasoned decisions, and we thank you for your continued trust and support. Your input is always welcome, and we ask that you contact us with any questions or concerns.

DISCLOSURE

All information is believed to be from reliable sources; however we make no representation as to its completeness or accuracy. All economic and performance data is historical and not indicative of future results. Market indices discussed are unmanaged. Investors cannot invest in unmanaged indices. Additional risks are associated with international investing, such as currency fluctuations, political and economic instability and differences in accounting standards.

Investing in securities in emerging markets involves special risks due to specific factors such as increased volatility, currency fluctuations and differences in auditing and other financial standards. Securities in emerging markets are volatile and can decline significantly in response to adverse issuer, political, regulatory, market, or economic developments.

An index is a statistical measure of change in an economy or a securities market. In the case of financial markets, an index is an imaginary portfolio of securities representing a particular market or a portion of it. Each index has its own calculation methodology and is usually expressed in terms of a change from a base value. Thus, the percentage change is more important than the actual numeric value. An investment cannot be made directly into an index.

Investing in fixed income securities involves credit and interest rate risk. When interest rates rise, bond prices generally fall. Investing in commodities may involve greater volatility and is not suitable for all investors. Investing in a non-diversified fund that concentrates holdings into fewer securities or industries involves greater risk than investing in a more diversified fund. The equity securities of small companies may not be traded as often as equity securities of large companies so they may be difficult or impossible to sell. Neither diversification nor asset allocation assure a profit or protect against a loss in declining markets. Past performance is not an indicator of future results.

Sean P. Storck and Steven W. Pollock are registered representatives with and securities and Retirement Plan Consulting Program advisory services offered through LPL Financial, a Registered Investment Advisor. Member FINRA/SIPC. Financial Planning offered through Reason Financial, a state Registered Investment Advisor. Investment advice offered through Merit Financial Group, LLC an SEC Registered Investment Advisor. Merit Financial Group and Reason Financial are separate entities from LPL Financial. Tax related services offered through Reason Tax Group. Reason Tax Group is a separate legal entity and not affiliated with LPL Financial. LPL Financial does not offer tax advice or tax related services. Sean P. Storck CA Insurance Lic#OF25995 and Steven W. Pollock CA Insurance Lic#OE98073

1 “Transcript of Chair Powell’s Press Conference.” Www.federalreserve.gov, The Federal Reserve, 17 Mar. 2021, www.federalreserve.gov/mediacenter/files/FOMCpresconf20210317.pdf.

2 “Transcript of Chair Powell’s Press Conference.” Www.federalreserve.gov, The Federal Reserve, 17 Mar. 2021, www.federalreserve.gov/mediacenter/files/FOMCpresconf20210317.pdf.

3 “Hyperinflation in the Weimar Republic.” Wikipedia, Wikimedia Foundation, 6 Apr. 2021, en.wikipedia.org/wiki/Hyperinflation_in_the_Weimar_Republic#:~:text=Hyperinflation%20affected%20the%20German%20Papiermark,misery%20for%20the%20general%20populace.

4 “Hyperinflation in Yugoslavia.” Wikipedia, Wikimedia Foundation, 11 Jan. 2021, en.wikipedia.org/wiki/Hyperinflation_in_Yugoslavia.

5 Hyperinflation in Zimbabwe.” Wikipedia, Wikimedia Foundation, 25 Mar. 2021, en.wikipedia.org/wiki/Hyperinflation_in_Zimbabwe#:~:text=Hyperinflation%20in%20Zimbabwe%20was%20a,hyperinflation%2C%20began%20in%20February%202007.&text=However%2C%20Zimbabwe’s%20peak%20month%20of,year%20in%20mid%2DNovember%202008.

6 Hanke, Steve H. “North Korea: From Hyperinflation to Dollarization?” Cato Institute, 22 Jan. 2021, www.cato.org/commentary/north-korea-hyperinflation-dollarization.

7 “Hyperinflation in Venezuela.” Wikipedia, Wikimedia Foundation, 5 Apr. 2021, en.wikipedia.org/wiki/Hyperinflation_in_Venezuela.

8 “Transcript of Chair Powell’s Press Conference.” Www.federalreserve.gov, The Federal Reserve, 17 Mar. 2021, www.federalreserve.gov/mediacenter/files/FOMCpresconf20210317.pdf.

9 McMahon, Tim. “Inflation in the 1980’s.” InflationData.com, 18 June 2015, inflationdata.com/articles/inflation-cpi-consumer-price-index-1980-1989/#:~:text=Inflation%20peaked%20in%20April%201980,due%20to%20the%20poor%20economy.

10 “Transcript of Chair Powell’s Press Conference.” Www.federalreserve.gov, The Federal Reserve, 17 Mar. 2021, www.federalreserve.gov/mediacenter/files/FOMCpresconf20210317.pdf.

11 Hanke, Steve H. “North Korea: From Hyperinflation to Dollarization?” Cato Institute, 22 Jan. 2021, www.cato.org/commentary/north-korea-hyperinflation-dollarization.

Disclosure

This material is for general information only and is not intended to provide specific advice or recommendations for any individual. There is no assurance the views or strategies discussed are suitable for all investors or will yield positive outcomes. Investing involves risks including possible loss of principal. Any company names noted herein are for educational purposes only.

All information is believed to be from reliable sources; however we make no representation as to its completeness or accuracy. All economic and performance data is historical and not indicative of future results. Market indices discussed are unmanaged. Investors cannot invest in unmanaged indices. Additional risks are associated with international investing, such as currency fluctuations, political and economic instability and differences in accounting standards.

Investing in securities in emerging markets involves special risks due to specific factors such as increased volatility, currency fluctuations and differences in auditing and other financial standards. Securities in emerging markets are volatile and can decline significantly in response to adverse issuer, political, regulatory, market, or economic developments.

An index is a statistical measure of change in an economy or a securities market. In the case of financial markets, an index is an imaginary portfolio of securities representing a particular market or a portion of it. Each index has its own calculation methodology and is usually expressed in terms of a change from a base value. Thus, the percentage change is more important than the actual numeric value. An investment cannot be made directly into an index.

Investing in fixed income securities involves credit and interest rate risk. When interest rates rise, bond prices generally fall. Investing in commodities may involve greater volatility and is not suitable for all investors. Investing in a non-diversified fund that concentrates holdings into fewer securities or industries involves greater risk than investing in a more diversified fund. The equity securities of small companies may not be traded as often as equity securities of large companies so they may be difficult or impossible to sell. Neither diversification nor asset allocation assure a profit or protect against a loss in declining markets. Past performance is not an indicator of future results.

Financial Planning offered through Reason Financial, a state Registered Investment Advisor. Investment advice offered through Merit Financial Group, LLC an SEC Registered Investment Advisor. Merit Financial Group and Reason Financial are separate entities. Tax related services offered through Reason Tax Group. Reason Tax Group is a separate legal entity and not affiliated with Merit Financial Group, LLC. Sean P. Storck CA Insurance Lic#OF25995 and Steven W. Pollock CA Insurance Lic#OE98073

Copyright © 2026 Reason Financial all rights reserved.

Continue Reading

3rd Quarter 2026 – Economic and Market Update

Q2 2026 in review: the S&P 500’s best quarter since 2020, oil’s round trip from $114 back to $70, a 4.2% CPI print that would not quit, and a new Fed chair who took 2026 rate cuts off the table — plus what a 15% quarter means for the allocation you actually own.

America at 250: A Birthday Worth Sitting With for a Moment

The United States just turned 250 — and the story reads surprisingly well as a series of 50-year check-ins. Founding-era population the size of San Diego County, two presidents with impeccable dramatic timing, a telephone demo in Philadelphia, quarters you’re still finding in your change — and one compounding machine that started counting in 1926.

American Teens Aren’t Working Summer Jobs Like They Used To

DisclosureThis material is for general information only and is not intended to provide specific advice or recommendations for any individual.…