August 2015 – A Mid-Quarter Update

A MID-QUARTER UPDATE

Global markets have extended the selloff from last week into the current. The pullback in the U.S., while not as pronounced as in emerging and international markets, has been significant and sharp causing a degree of uncertainty among investors. We want to provide you with our insights to the current market conditions.

The current correction in equities does not appear to be a function of systemic risk as experienced during the financial crisis of 2008/09. In a recent quarterly statement released by FDIC Chairman Martin Gruenberg he reported the number of banks and the $ amount of assets on the “Problem List” is at its lowest level in six years and down 70% from their respective peaks. We are still in recovery mode andthe overall improvement and health of the financial system remains encouraging.

The Federal Reserve remains unfazed in their long-term strategy to raise interest rates. As of the market opening on Monday the general consensus was that the probability of a Federal Reserve rate hike for September had been significantly decreased due to volatility. However, late in the day Federal Reserve Bank of Atlanta President Dennis Lockhart publically communicated a different sentiment stating that, “from my perspective September remains a live possibility”. It is an unknown if this will serve as a hurdle for markets to overcome, or will quell anxiety over future growth.

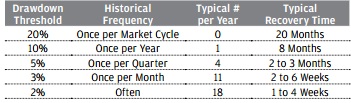

CURRENT EXPANSION

The current bull market has gone almost 4 years or 1,418 calendar days without experiencing an official “correction” as defined by a 10% decrease in market value. A decline of 10% has occurred on average once per year with a typical market recovery time of about 8 months. Moderate pullbacks happen frequently even in healthy economic environments.

Source: Standard & Poor’s, FactSet, J.P. Morgan Asset Management. Returns are based on price index only and do not include dividends. For illustrative purposes only. Data are as of 1/31/15.

The result of such an extended period of time without a market correction combined with tension over China’s currency devaluations has lead us into the rapid downward movement which we are currently experiencing. Periods of market decline are normal and inevitable in a long-term investing strategy.

CATALYST

The devaluation of the Yuan (¥) by China has largely been cited as the triggering event. With the devaluation came concerns of a significant slowdown in the world’s second-largest economy and potential ripple effects on the global economy. China’s government is not as transparent in reporting economic data as most would like and the action by the government to jump-start the economy has caused the investing community to question if things are worse than had been previously reported.

It is worthwhileto take note of the year-to-date movement of the Shanghai Composite Index we hear so much of today. Previously up almost 63% for the year as of early June 2015, it has since then experienced a rapid loss. While the percentage fluctuations on the year are large, the net effect has been pretty lackluster with a year-to-date negative return of 4.05% as of the market close on August 24, 2015. Giving back gains obtained over the short term is a different scenario than is generally being reported.

Source: http://money.cnn.com/data/world_markets/se_composite/

MOVING FORWARD

We remain committed to the protection of your assets and the growth of your investment portfolio. Our focus is to protect value on a risk adjusted basis. One way we accomplish this is to include an appropriate amount of fixed income based on risk tolerance in each portfolio. As of the writing of this update fixed income is serving as a counter-balance against the volatility of the equity markets. The most appropriate action to take at this time is to maintain the risk adjusted allocations of your portfolio, which we continue to review and rebalance as necessary.

Periods of normal market volatility provide an opportunity and reminder to review your long-term objectives and ensure they fall in line with the level of risk exposure in your portfolio.

We continue to focus on protecting value, providing you with trusted advice, and assisting you and your family in making good decisions over your lifetime.

We thank you for your continued trust and support. Your input is always welcome and we ask that you contact us with any questions or concerns.

DISCLOSURE

All information is believed to be from reliable sources; however we make no representation as to its completeness or accuracy. All economic and performance data is historical and not indicative of future results. Market indices discussed are unmanaged. Investors cannot invest in unmanaged indices. Additional risks are associated with international investing, such as currency fluctuations, political and economic instability and differences in accounting standards.

Investing in securities in emerging markets involves special risks due to specific factors such as increased volatility, currency fluctuations and differences in auditing and other financial standards. Securities in emerging markets are volatile and can decline significantly in response to adverse issuer, political, regulatory, market, or economic developments.

An index is a statistical measure of change in an economy or a securities market. In the case of financial markets, an index is an imaginary portfolio of securities representing a particular market or a portion of it. Each index has its own calculation methodology and is usually expressed in terms of a change from a base value. Thus, the percentage change is more important than the actual numeric value. An investment cannot be made directly into an index.

Investing in fixed income securities involves credit and interest rate risk. When interest rates rise, bond prices generally fall. Investing in commodities may involve greater volatility and is not suitable for all investors. Investing in a non-diversified fund that concentrates holdings into fewer securities or industries involves greater risk than investing in a more diversified fund. The equity securities of small companies may not be traded as often as equity securities of large companies so they may be difficult or impossible to sell. Neither diversification nor asset allocation assure a profit or protect against a loss in declining markets.

Past performance is not an indicator of future results.

Securities offered through 1st Global Capital Corp., Member FINRA and SIPC. Bruce Rawdin-Baron, Steven W. Pollock, Sean Storck and Nicole Albrecht are Registered Representatives of 1st Global Capital Corp. Investment advisory services, including RBFI portfolios offered through Rawdin-Baron Financial, Inc. IMS platform accounts offered through 1st Global Advisors, Inc. Rawdin-Baron Financial, Inc. and 1st Global Capital Corp. are unaffiliated entities. Rawdin-Baron Financial, Inc. is a Registered Investment Adviser. Placing business through 1st Global Insurance Services. Registration does not imply a certain level of skill or training. We currently have individuals licensed to offer securities in the states of Arizona, California, Illinois, Indiana, Kansas, Massachusetts, Michigan, New York, Oregon and Washington. This is not an offer to sell securities in any other state or jurisdiction. CA Department of Insurance License: Bruce Rawdin-Baron #0736631, Steven W. Pollock #OE98073, Sean Storck #0F25995 and Nicole Albrecht #0F99962.