January 2016 – An Economic and Market Update

EXECUTIVE SUMMARY

- The domestically produced Oil Export Ban in force since 1975 was recently lifted allowing for U.S. oil to be sold and shipped internationally.[i]

- The Federal Reserve raised interest rates for the first time in nearly a decade with a symbolic move “off the bottom” by a quarter point. [ii]

- US dollar strength continues as the rest of the world struggles to find solid footing and sustainable growth.

- The Housing Industry is coming back (finally), aided in large part by low interest rates keeping the affordability index at attractive levels.

LOOKING BACK

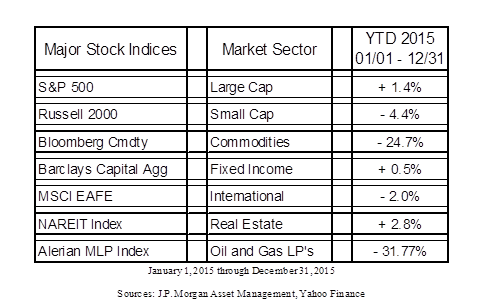

Looking back at 2015, the broad market and its various component indices saw their fair share of disruption and volatility. While three sectors, US Large Cap Stocks, Fixed Income and Real Estate, provided slightly positive returns, Commodities and International stocks bore the brunt of the downdraft. Following are some of the events which served to make the last year so challenging:

• ISIS moves global with a major terror event in Paris resulting in 130 dead and 368 wounded and a lone wolf style attack in San Bernardino resulting in 14 dead and 21 wounded. [iii],[iv]

• Russian warplane shot down in Turkish airspace while ostensibly providing air support against ISIS forces in Syria. [v]

• Greece missed a payment to the International Monetary Fund becoming the first developed country to miss a payment and joining the ranks of other countries who have defaulted such as Iraq, Afghanistan and Bosnia. [vi]

• The price of oil plummeted amidst a backdrop of slowing demand and quickly growing supply surplus.

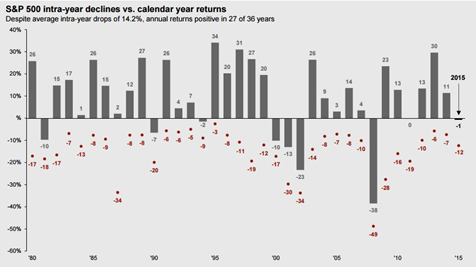

The last time we experienced such a challenge in the markets was 2011, as evidenced below, which also happens to be the last time holding cash proved more successful than an asset allocation strategy.

Source: Standard & Poor’s, FactSet, J.P. Morgan Asset Management

Guide to the Markets – U.S. Data are as of 12/31/2015

DOMESTIC OIL EXPORTS AUTHORIZED

A major disruption event of 2015 (and the forseeable future) continues to be the energy renaissance occurring in the the United States. The majority of entities in the energy space experienced downward price pressure as a direct result of the supply of oil and gas far outstripping current demand. This has caused signifcant stock market volatility as the Energy Sector represents 12.7% of the S&P 500. We have said it before, but it bears saying again: the energy boom is a double edged sword – savings at the pump come at the expense of those working in the oil & gas industry and impact investors in the form of stock market volatility.

In the face of these challenges Congress removed the 40-year-old ban on domestic crude oil exports despite the political and strategic risks. The hope is the policy change will serve to stabilize prices in the intermediate term as the dislocation in global and domestic oil markets are allowed to adjust against one another.

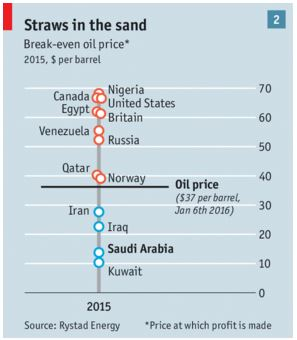

Source: Rystad Energy, Economist.com

Oil production costs vary across the globe with the lowest production costs existing in the Middle East. OPEC, led by Saudi Arabia, has maintained production in the face of plummeting oil prices in an attempt to force the United States to decrease production. The success of this strategy remains to be seen. However, with the removal of the export ban, Congress is placing the world on notice that the U.S. will not go away. Fracking and shale drilling are here to stay and the sooner prices stabilize the better it will be for the economy.[vii]

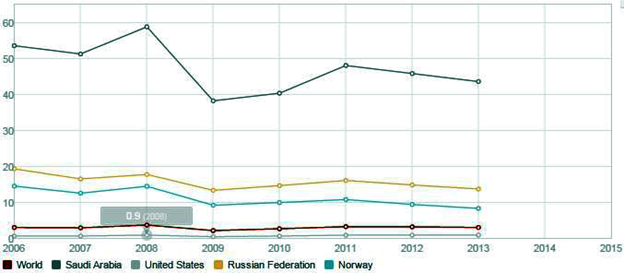

Oil Rents (% of GDP)

Source: The World Bank

When the production costs of oil are compared against the % of GDP made up of oil revenue, traditionally called “Oil Rents”, it becomes clearer why Saudi Arabia would choose to keep production up. Saudi Arabia and other Middle Eastern countries are heavily reliant upon Oil Rents to keep the economy moving and have very low production costs. The U.S. has a very low percentage of GDP tied in to Oil Rents and significantly higher production costs. We expect continued volatility in this space while various factors work themselves out. There is a major Supply/Demand issue going on which will take time to figure out, as will the politics of oil in the various countries significantly impacted by oil prices.[viii]

THE FEDERAL RESERVE

For the first time since June 29, 2006 the Federal Reserve raised the target interest rate. The increase “off the bottom” of 25 basis points, or .25%, fell within the range anticipated by the markets and did not surprise anyone. Whether or not an increase was warranted continues to be a matter of debate. Many market commentators are expressing concerns that an increase in the face of a slowing global economy may serve to advance elements of stagflation. The Federal Reserve made clear that, “The stance of monetary policy remains accommodative after

this increase, thereby supporting further improvement in labor market conditions and a return to 2% inflation.” [ix],[x]

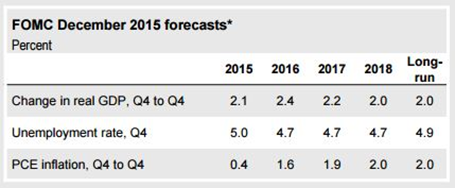

Source: FactSet, Federal Reserve, J. P. Morgan Asset Management, Forecasts of 17 FOMC Participants, midpoints of central tendency except for federal funds rate, which is a median estimate. Guide to the Markets – U.S. Data are as of December 31, 2015

The chart above aggregates the Federal Open Market Committee (FOMC) forecast of three significant economic data points: Change in Real GDP, Unemployment, and Personal Consumption Expenditure (PCE) Inflation. With current inflation measuring substantially below the target set by the Federal Reserve of 2%, it appears we will see a long series of slow rate increases.

What this means for the average person is undefined at this time. The quarter-point adjustment does not necessarily mean banks will pass that increase along to holders of savings and money market accounts in the form of higher earnings. Fixed rate mortgages are based on longer term rates, such as the 10-year treasury, and are unlikely to be moved. In fact, mortgage rates recently ticked down in light of economic data.

A quote commonly attributed to Mark Twain comes to mind when trying to find some direction for where interest rates may be moving, “History doesn’t repeat itself, but it does rhyme.” For several years now, a parallel has been drawn between the economic environment of Japan over the last 25 years with that of where the U.S. might be headed. Our experience will not be exactly the same; however we appear to be another stanza in a poem being written about developed countries with an ageing population base and growing debt.

STRENGTH IN THE GREENBACK

The U.S. Dollar saw an increase of nearly 10% in 2015, further closing the gap with the Euro. Though we may not see an exact 1:1 ratio anytime soon, the strengthening dollar is significant. The performance of the U.S. Dollar over the past three years has kept inflation low. With unemployment down to 5% levels, and consumer spending/confidence improving, the current economic environment in the U.S. serves as justification for the Fed to make future rate hikes.[xi]

A stronger dollar impacts trade as well as the profits of large U.S. companies that derive a majority of their earnings from international sources. American goods become more expensive abroad thus becoming less competitive and incentivizing foreign market countries to buy their own goods. The reduction in demand has a direct correlation to a reduction in U.S. manufacturing which has put additional downward pressure on the S&P 500.[xii]

Currency strength is a direct result of economic strength and stability relative to other alternatives. While the rising value of the U.S. Dollar has put pressure on large U.S. Company profits abroad, tightened trade margins and led to the recent rate hike, it also means that the U.S. economy as a whole is prospering. Prices are down at the pump, wages are moving up (slowly), U.S. made products are more affordable and international travel is currently a bargain.[xiii]

DOMESTIC HOUSING INDUSTRY

In April of 2014 an article in the New York Times, “Why the Housing Market Is Still Stalling the Economy”, placed a significant amount of blame on the stagnant economy on the slow rebound of housing. The good news for the U.S. is that a little more than a year later, that trend appears to be turning. Building Permits and Housing Starts increased over the previous year same time frame 19.5% and 16.5% respectively. Full year data for 2015 is not yet available, but it appears as if significant ground has been made in getting the housing industry back on track.[xiv]

Source: Census Bureau, FactSet

Guide to the Markets – U.S. Data are as of December 31, 2015 unless noted

With housing affordability still reading far below average measurements, helped in large part by historically low interest rates, it is only a matter of time until housing starts make it into expansionary territory.

LOOKING FORWARD

Congress recently managed to agree and passed the Omnibus Spending Bill without having the process become a national emergency. Included in the bill were a variety of tax related items. We have enclosed a more comprehensive discussion of the tax impacts and encourage you to read through it. Congress Included in the law changes an extension of the mortgage debt cancellation forgiveness provisions through 2016, and made permanent the IRA Charitable Gift rules.[xv]

The Federal Reserve currently forecasts four consecutive rate increases in 2016. We look forward to seeing how this plays out with our expectation that any continued weak inflation numbers will likely delay this scenario. In the meantime we believe the increases will occur at a slow pace, particularly with the rest of the globe keeping rates either flat or going lower.[xvi]

We remain committed to the protection of your assets and the growth of your investment portfolio. Our focus is to protect value, provide you with trusted advice, and assist you and your family in making a lifetime of rational, informed and well-reasoned financial decisions. At this point we remain cautiously optimistic of the direction of the markets and are fully allocated across our model portfolios.

We thank you for your continued trust and support. Your input is always welcome and we ask that you contact us with any questions or concerns.

End notes

[i] Domm, Patti. “Lifting Oil Export Ban Could Be Long-Term Game Changer.” Market Insider. CNBC.com. 16 December 2015

[ii] Cox, Jeff. “Fed Raises Rates By 25 Basis Points, First Since 2006.” Economy. CNBC.com. 16 December 2015

[iii] “November 2015 Paris Attacks.” Wikipedia: The Free Encyclopedia. Wikimedia Foundation, Inc. 11 January 2016. 11 January 2016

[iv] Calamur, Krishnadev. “San Bernardino Shooting: An ISIS Link?” The Atlantic. 4 December 2015. 8 January 2016

[v] “Turkey’s Downing of Russian Warplane – What We Know.” BBC News Middle East. BBC News. 1 December 2015. 8 January 2016

[vi] Ewing, Jack and Kanter, James. “Missing I.M.F. Payment Puts Greece in Uncharted Territory.” DealB%k. NY Times. 30 June 2015. 9 January 2016

[vii] “Sale of the Century.” The Economist. The Economist, 09 January 2016. Web. 09 January 2016

[viii] The World Bank

[ix] Federal Reserve. Press Release. 16 December 2015

[x] Federal Reserve. Press Release. 16 December 2015

[xi] LaHart, Justin. “Strong Dollar Won’t Get Weak In the Knees.” The Wall Street Journal. Heard on the Street, 18 December 2015. Web.

[xii] La Monica, Paul R. “Is the Dollar Too Strong For Its Own Good.” CNN Money. Cnn Money. 09 November 2015. Web.

[xiii] Chang, Sue. “Investors Are Ignoring the Strong Dollar At Their Peril.” MarketWatch. MarketWatch.com. 08 November 2015. Web.

[xiv] U.S. Census Bureau. Joint Release U.S. Department of Housing and Urban Development. “New Residential Construction In November 2015.” 16 December 2015.

[xv]The U.S. House of Representatives Committee on Appropriations.

[xvi]Condon, Christopher. “Fed Ends Zero-Rate Era; Signals 4 Quarter-Point Increases in 2016.” BloombergBusiness. Bloomberg.com. 16 December 2015. 7 January 2016

Disclosure