January 2019 – An Economic and Market Update

Executive Summary

- Stock markets posted their worst December since the Great Depression turning the markets negative on the year.

- The global economy is taking a bit of a hit with indications of slowing in multiple advanced and developing economies across the globe.

- The government shutdown, now in its 6th week, will slow or wipe out growth completely in the 1st Quarter of 2019 if current estimates hold true.

- How to plan for emergencies and effectively hold your cash reserves.

Looking Back

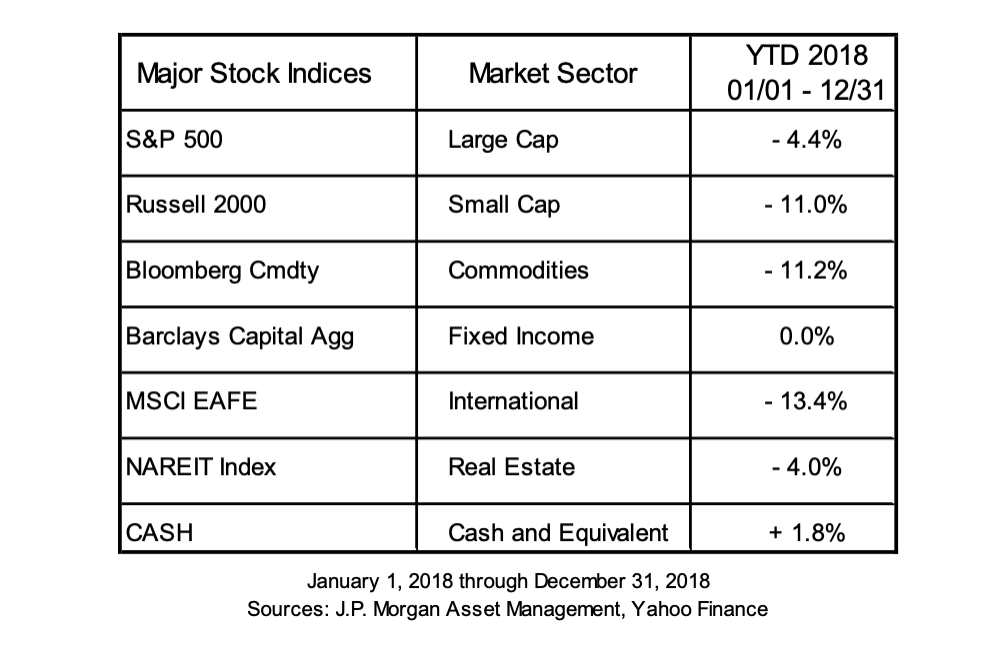

For the first time in a decade cash has been the best performer of the year. December had a lot to do with this as the S&P 500 posted its worst December with a -10.2% return since 1931 when it fell -14.5%. Traditionally, this is a good month on the markets carrying the moniker, “The Santa Claus Rally”. A variety of explanations have been suggested for the crash in prices such as computer driven trading in thin markets, economic slowdown in China, closure of the Federal Government, interest rate increases by the Fed, amongst other things.

It is possible to find a scientific explanation for many things. In fact, you can find a very in-depth study done on the limits of skipping stones across the water. The current world record is 88; scientific models project a 300 to 350 skip possibility. Unfortunately, trying to figure out why the market moves is a bit more challenging than modeling rock skipping possibilities.

Reading The Tea Leaves

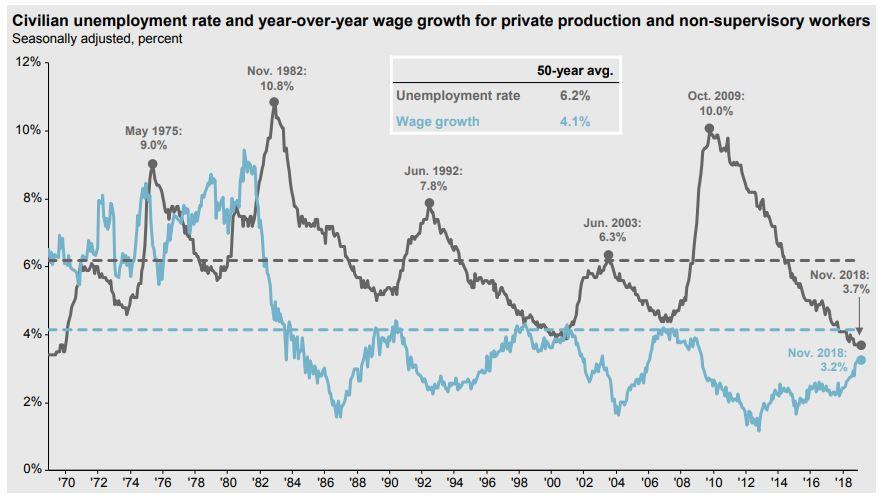

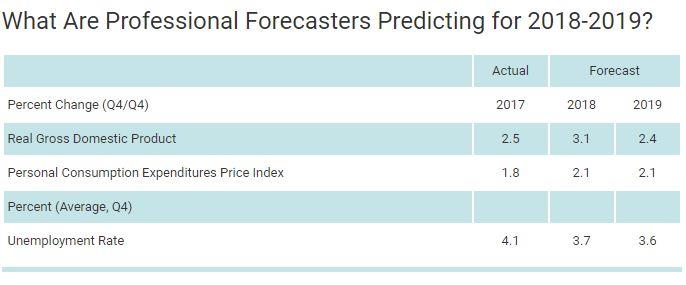

We are halfhearted in our optimism for 2019 market growth. The good news is that we have very low unemployment coupled with increasing wage growth, as seen below. Also notable from the graph, is that over the last thirty years convergence lasts for a year or two before a recession occurs and there is a corresponding spike in unemployment and slowdown in wage growth.

Guide to the Markets – U.S. Data are as of December 31, 2018

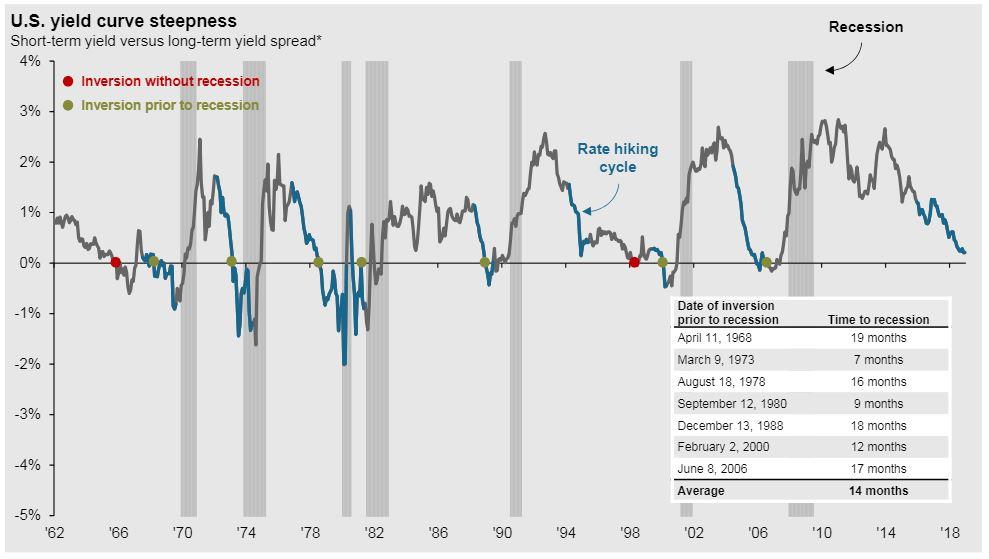

A notable event of 2018 was the short-term partial inversion of the yield curve. This lasted only briefly but sparked concerns of an imminent recession.

Guide to the Markets – U.S. Data are as of December 31, 2018

Recession periods in the graph above are marked in gray. The line on the graph represents the yield spread between short and long-term rates. Any time the line drops below zero a full inversion of the yield curve has occurred, short-term rates are higher than long-term. There have been multiple instances of this occurring over the last 50 years with most of those instances being followed by recession within 7 to 19 months. Inversion is a symptom of a weakening economy not the cause of recession. Tightening yields provides a hint that we are in the later stages of the business cycle. The good news is that a slowing expansion is still an expansion.

Globally, economic growth is slowing. This reality was confirmed when China released their 2018 Gross Domestic Product (GDP) figure of 6.6%. This is the lowest measurement in almost 30 years and has furthered speculation that China is facing an economic crisis. Responding to fears over a slowdown in his country, Vice-President Wang Qishan recently stated in Davos, Switzerland, “there will be a lot of uncertainties in 2019, but one certainty is that China’s economic growth will continue and be sustainable.”

Guide to the Markets – U.S. Data are as of December 31, 2018

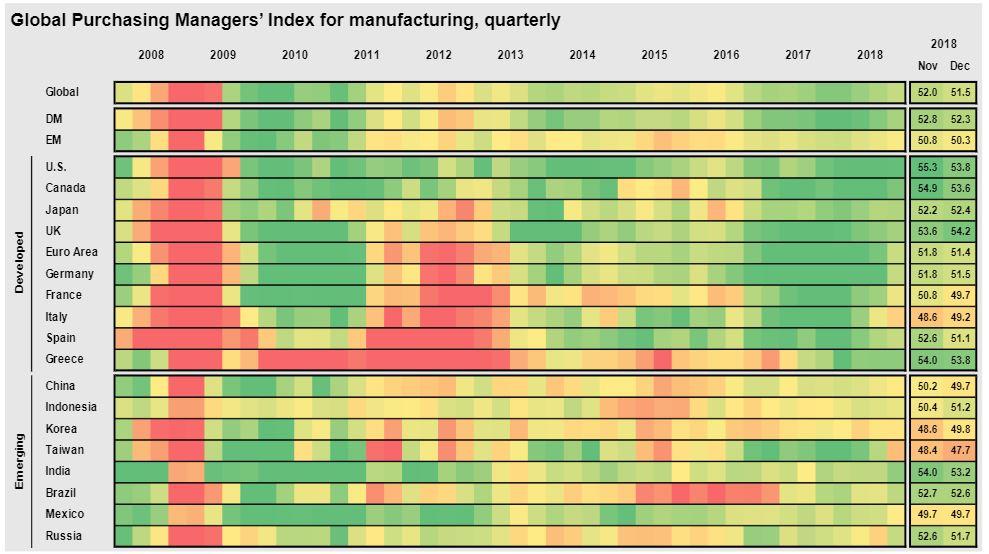

The Global Purchasing Managers’ Index, or PMI, is a measure of a variety of data such as inventory and production levels, supplier deliveries, employment and new orders. A measure above 50 represents improving markets and the reverse is true for measures under 50. Additionally, the further away the reading is from 50 the more powerful the improvement or deterioration. Recent data show that Chinese economic conditions are deteriorating, albeit slowly, along with other major developing nations such as Mexico and Korea. The top bar in the graph represents the aggregate of all major economies in the world. The consensus is that global growth is still here, but it is slower than a month ago and significantly slower than a year ago.

Domestic and global economic conditions right now are like taking a lukewarm shower with low water pressure. You really wish it could be hotter and stronger, but you are glad it is not ice cold.

The Economics of It All

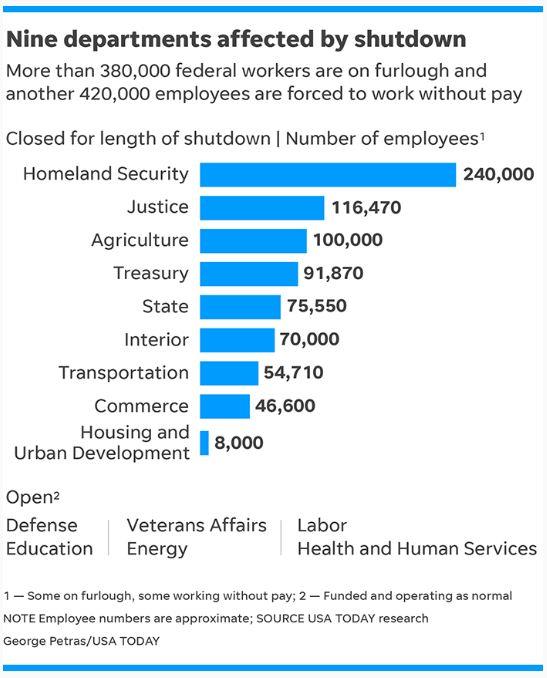

The partial shutdown of the Federal Government is having an economic effect, even the White House says so. Only in retrospect will we see just how big the economic hit is, but with 800,000 workers and additional sub-contractors not getting paid, there will be a ripple through our economy. Government spending has a fiscal multiplier effect where money spent by the government will enter the economic system and continue to be spent in diminishing increments repeatedly. The wages paid to Federal workers are a part of this process.

Various estimates of the impact to GDP of the government shutdown are out there, but a recently released number by a White House official is that the cost is .13% of GDP for each week the shutdown continues. By comparison, Superstorm Sandy, which left significant flood damage in the New York City region and forced the closure of the stock markets, had an estimated .1% to .15% negative impact to GDP. It is not a perfect example, but for every week the government is shutdown the economic effect is like having a hurricane strike a vital economic zone of our country.

Recent quotes by two prominent financial personages illustrate the dangerous predicament we are in. Fed Chairman Powell has said that, “if we had an extended shutdown then I do think that would show up in the data pretty clearly.” Likewise, Jamie Dimon, CEO and Chairman of JP Morgan Bank, believes that if the “impasses persisted it could push growth down to zero” and that “we just have to deal with that – it is more of a political issue than anything else.”,

The predicted GDP growth for 2019 according to the Federal Reserve Bank of Philadelphia is 2.4%. Split in to quarters this would be .6% in GDP growth per quarter. The estimated negative impact to U.S. GDP, currently -.65% (-.13% x 5 weeks), is effectively wiping out all forecast growth in the 1st Quarter of 2019. Even if the government reopens tomorrow, people get paid, and spending resumes, the fact remains that spending will not completely recover. Discretionary spending activities such as lunch out during the workday or a date night are not going to be made up. Bills will get paid but lost consumption is still lost consumption. There are reasons to be tepidly optimistic for 2019 as we discussed earlier, but the economic impact of this shutdown is making it challenging to keep the faith.

The Planning Corner: Goverment Shutdown Edition

Now entering its 6th week, the current government shutdown is the longest in history topping the 21-day closure during former President Clinton’s time in office. Federal employees and sub-contractors are missing paychecks, and with more missed paydays looking likely, this political logjam is putting financial pressure on those affected (We have family and friends impacted as most people likely do).

Surveys may not be spot-on accurate, but they paint a picture of things, nonetheless. That picture as it relates to preparedness for an emergency (such as your employer not paying you) is stark. According to Bankrate’s financial security index survey only 39% of respondents would be able to cover a $1,000 emergency, and 36% of people would have to finance the cost of an emergency.

With so many people facing a politically created household budget crisis this is an appropriate time to discuss some planning techniques for dealing with the unexpected. It is impossible to predict when the cruelty of an emergency will strike, but we can be prepared financially as best as possible. In buildings we have “Emergency Exits” to help get out in case of fire or some other catastrophic event. Just as buildings have “Emergency Exits”, so too should our finances.

The following are some of the rules we believe people should follow.

- Bank account buffer – one (1) paycheck.

- Emergency fund – three (3) to six (6) months’ worth of living expenses.

- Household budget – define your expenses, differentiating necessary from discretionary.

It is never fun to spend money from emergency funds. Usually something has happened like a leaky roof or a late-night emergency room visit. However, having your emergency fund ready will give you peace of mind when disaster does strike so you can focus on responding, instead of on how you are going to pay the bills. Once the funds are saved, the question becomes, where are they kept?

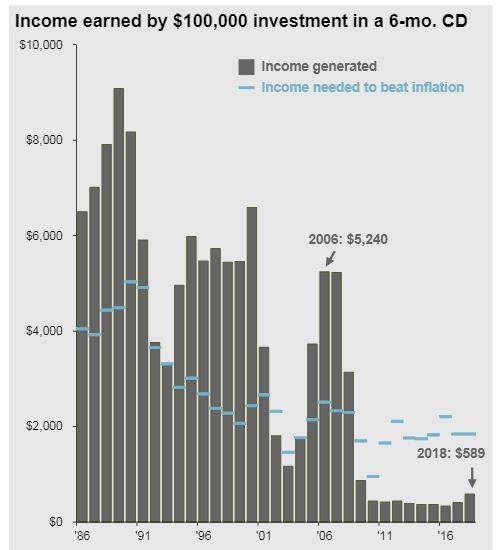

A review of the last 20 years of CD interest returns on a $100,000 investment provides an illustration of the meager returns available on cash right now.

Good planning on how you are going to access your emergency funds is critical. After all, do you hold some of it in cash form? Is it in your normal checking/savings account? Do you use CD’s? Or some form of online high yield savings? There are a lot of options, most of which do not pay very well as illustrated. If you are unsure of the right balance to have between cash/savings/cd’s we will be pleased to assist you in finding the right mix. We can also help identify the best way to maximize your yield on cash equivalents at a time when yield is hard to find.

Being prepared to miss a few paychecks is not fun, but good planning can sure go a long way towards making it less painful.

Looking Forward

We do our best to refrain from allowing politics to enter our professional realm. Good planning and strong investing strategy should span administrations and eras of political influence. For that reason, we avoid being swayed by the political atmosphere of today in order to focus on where each of our clients is trying to get tomorrow, 5 years from now, and 20+ years in the future.

That said, the President of the United States criticizing the Federal Reserve is a cause for concern. President Trump told the Washington Post he’s “not even a little bit happy with my selection of Jay.” Jay is a reference to Jerome Powell, the Chairman of the Federal Reserve. On what threatens the U.S. economy, Trump added, “I think the Fed is a much bigger problem than China.”

The Fed is an autonomous and non-partisan committee focused on maintaining stability in our economy through monetary policy. The executive and legislative branches of government set fiscal policy (government spending), and the Federal Reserve sets monetary policy (interest rates and money supply). This is an important check and balance in our system as one set of policies may create problems which the other is able to address.

We see attempts to break the autonomy of the Federal Reserve as a potential economic issue as it could reduce confidence in the committee and in the motivations behind their actions. Additionally, Brexit (the British attempt to leave the European Union), Italian debt concerns, U.S. company earnings growth, and a global oversupply of energy are problems facing us in 2019.

If you are concerned that the projected slowdown may impact your current financial plan please bring this to our attention. We are here to help you make rational, informed and well-reasoned decisions, and thank you for your continued trust and support. Your input is always welcome, and we ask that you contact us with any questions or concerns.

Disclosure

All information is believed to be from reliable sources; however we make no representation as to its completeness or accuracy. All economic and performance data is historical and not indicative of future results. Market indices discussed are unmanaged. Investors cannot invest in unmanaged indices. Additional risks are associated with international investing, such as currency fluctuations, political and economic instability and differences in accounting standards.

Investing in securities in emerging markets involves special risks due to specific factors such as increased volatility, currency fluctuations and differences in auditing and other financial standards. Securities in emerging markets are volatile and can decline significantly in response to adverse issuer, political, regulatory, market, or economic developments.

An index is a statistical measure of change in an economy or a securities market. In the case of financial markets, an index is an imaginary portfolio of securities representing a particular market or a portion of it. Each index has its own calculation methodology and is usually expressed in terms of a change from a base value. Thus, the percentage change is more important than the actual numeric value. An investment cannot be made directly into an index.

Investing in fixed income securities involves credit and interest rate risk. When interest rates rise, bond prices generally fall. Investing in commodities may involve greater volatility and is not suitable for all investors. Investing in a non-diversified fund that concentrates holdings into fewer securities or industries involves greater risk than investing in a more diversified fund. The equity securities of small companies may not be traded as often as equity securities of large companies so they may be difficult or impossible to sell. Neither diversification nor asset allocation assure a profit or protect against a loss in declining markets. Past performance is not an indicator of future results.

Securities offered through 1st Global Capital Corp., Member FINRA and SIPC. Steven W. Pollock, Sean P. Storck, Matthew J. Anderson and Nicole Albrecht are Registered Representatives of 1st Global Capital Corp. Investment advisory services, including RBFI portfolios offered through Reason Financial. IMS platform accounts offered through 1st Global Advisors, Inc. Reason Financial. and 1st Global Capital Corp. are unaffiliated entities. Reason Financial is a Registered Investment Adviser. Placing business through 1st Global Insurance Services. Registration does not imply a certain level of skill or training. We currently have individuals licensed to offer securities in the states of Arizona, California, Illinois, Indiana, Kansas, Massachusetts, Michigan, New York, Oregon and Washington. This is not an offer to sell securities in any other state or jurisdiction. CA Department of Insurance License: Steven W. Pollock #OE98073, Sean P. Storck #0F25995, Matthew J. Anderson #0F21959 and Nicole Albrecht #0F99962.

Copyright © 2018 Reason Financial all rights reserved.

Reason Financial

4747 Morena Blvd, Suite 102, San Diego, CA 92117

ENDNOTES

1 Sheetz, Michael. “The Stock Market Is on Pace for Its Worst December since the Great Depression.” CNBC, CNBC, 18 Dec. 2018, www.cnbc.com/2018/12/17/worst-start-to-december-for-the-stock-market-since-great-depression.html.

2 Gonzalez, Robbie. “Swift Stone Skippers Could in Theory Skip 100s of Skips.” Wired, Conde Nast, 31 Oct. 2018, www.wired.com/story/swift-stone-skippers-could-in-theory-skip-100s-of-skips/.

3 Bryan, Bob. “The Government Shutdown Could Cause a Disaster for the US Economy If Trump Follows through on His Threat to Continue the Fight for ‘Months’.” Business Insider, Business Insider, 14 Jan. 2019, www.businessinsider.com/government-shutdown-gdp-consumer-spending-us-economic-impact-2019-1.

4 Fleming, Sam. “Trump Insists He Has Right to Invoke Emergency Powers over Wall.” Financial Times, Financial Times, 10 Jan. 2019, www.ft.com/content/144859bc-150b-11e9-a581-4ff78404524e.

5 Noonan, Laura. “Shutdown Could Drive US Growth to Zero, Warns JPMorgan Chief.” Financial Times, Financial Times, 15 Jan. 2019, www.ft.com/content/9708ff76-18d7-11e9-9e64-d150b3105d21.

6 Tepper, Taylor. “Most Americans Don’t Have Enough Savings To Cover A $1K Emergency.” Bankrate, Bankrate.com, 12 Dec. 2018, www.bankrate.com/banking/savings/financial-security-0118/.

7 Zaveri, Mihir, et al. “This Government Shutdown Is the Longest Ever. Here’s the History.” The New York Times, NY Times, 24 Jan. 2019, This Government Shutdown Is the Longest Ever. Here’s the History.

8 Condon, Christopher. “A Timeline of Trump’s Quotes on Powell and the Fed.” Bloomberg.com, Bloomberg, 18 Dec. 2018, www.bloomberg.com/news/articles/2018-12-17/all-the-trump-quotes-on-powell-as-attacks-on-fed-intensify.

Disclosure

This material is for general information only and is not intended to provide specific advice or recommendations for any individual. There is no assurance the views or strategies discussed are suitable for all investors or will yield positive outcomes. Investing involves risks including possible loss of principal. Any company names noted herein are for educational purposes only.

All information is believed to be from reliable sources; however we make no representation as to its completeness or accuracy. All economic and performance data is historical and not indicative of future results. Market indices discussed are unmanaged. Investors cannot invest in unmanaged indices. Additional risks are associated with international investing, such as currency fluctuations, political and economic instability and differences in accounting standards.

Investing in securities in emerging markets involves special risks due to specific factors such as increased volatility, currency fluctuations and differences in auditing and other financial standards. Securities in emerging markets are volatile and can decline significantly in response to adverse issuer, political, regulatory, market, or economic developments.

An index is a statistical measure of change in an economy or a securities market. In the case of financial markets, an index is an imaginary portfolio of securities representing a particular market or a portion of it. Each index has its own calculation methodology and is usually expressed in terms of a change from a base value. Thus, the percentage change is more important than the actual numeric value. An investment cannot be made directly into an index.

Investing in fixed income securities involves credit and interest rate risk. When interest rates rise, bond prices generally fall. Investing in commodities may involve greater volatility and is not suitable for all investors. Investing in a non-diversified fund that concentrates holdings into fewer securities or industries involves greater risk than investing in a more diversified fund. The equity securities of small companies may not be traded as often as equity securities of large companies so they may be difficult or impossible to sell. Neither diversification nor asset allocation assure a profit or protect against a loss in declining markets. Past performance is not an indicator of future results.

Financial Planning offered through Reason Financial, a state Registered Investment Advisor. Investment advice offered through Merit Financial Group, LLC an SEC Registered Investment Advisor. Merit Financial Group and Reason Financial are separate entities. Tax related services offered through Reason Tax Group. Reason Tax Group is a separate legal entity and not affiliated with Merit Financial Group, LLC. Sean P. Storck CA Insurance Lic#OF25995 and Steven W. Pollock CA Insurance Lic#OE98073

Copyright © 2026 Reason Financial all rights reserved.

Continue Reading

2nd Quarter 2026 – Economic and Market Update

Q1 2026 in review: oil shock, S&P 500 down 4.3%, commodities up 24.4%, the cease-fire that became a blockade — and the planning moves that matter most coming out of a quarter like this one.

It’s Now More Common To Have A Baby In Your Thirties Than In Your Twenties

DisclosureThis material is for general information only and is not intended to provide specific advice or recommendations for any individual.…

When Does Refinancing Actually Make Sense? A 2026 Reality Check

If you locked in a mortgage at 7% or higher in 2023 or 2024, you’ve probably been watching rates with…