July 2022 – Economic and Market Update

EXECUTIVE SUMMARY

- It will likely be months before a recession is officially called, but it is certainly feeling like data coming out of the 2nd quarter will not provide much solace.

- Economic indicators are divergent with both encouraging and discouraging data points. Remember that missing the best days in the market is a recipe for disaster and make sure your current allocation is appropriate for your time horizon and needs.

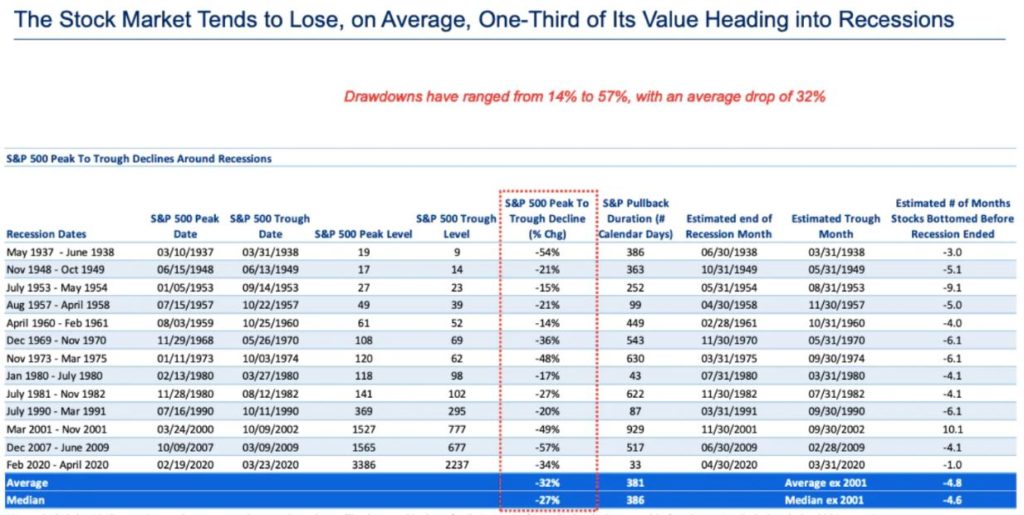

- If we are in a recession, history suggests we are not out of the woods yet with average market drawdowns of 32% over an average of 381 days.

Macro-economic analysis is a prolonged exercise in hedging, prevarication, and generally avoiding saying anything that can be directly refuted at a later date. On the plus side, for anyone who attempts to make a call, memories are short, the real world is complex, and you can always explain after the fact why your original call was wrong. Why does that matter? It matters because everyone wants to know if we are in a recession and, if so, what that means for markets. Is Reason Financial calling a recession? We

are not, but we won’t be surprised if we are. The NBER (National Bureau of Economic Research) is the official recession calling entity in the United States. Here is some verbiage from their FAQs that will provide some context on why it is so hard to say whether we are in a recession:

Q: Typically, how long after the beginning of a recession does the committee declare that a recession has started? After the end of the recession?

A: Our determination of the trough date in April 2020 occurred 15 months after that date, in July 2021. Earlier determinations took between 4 and 21 months. There is no fixed timing rule. We wait long enough so that the existence of a peak or trough is not in doubt, and until we can assign an accurate peak or trough date.i

For context, the 1st quarter 2022 GDP (Gross Domestic Product) figure, officially a -1.6% decline in GDP, was revised down from the initial estimate and finalized after three revisions on June 29, 2022, a full three months after the close of the quarter. It would not be shocking if the following occurred: GDP estimate for the 2nd quarter comes in at a +.1% growth rate, is subsequently revised down to -.2% three months down the road, and officially recognized as a recession sometime later this year or next.ii

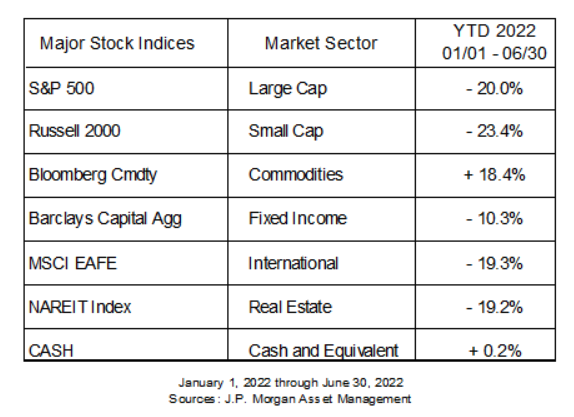

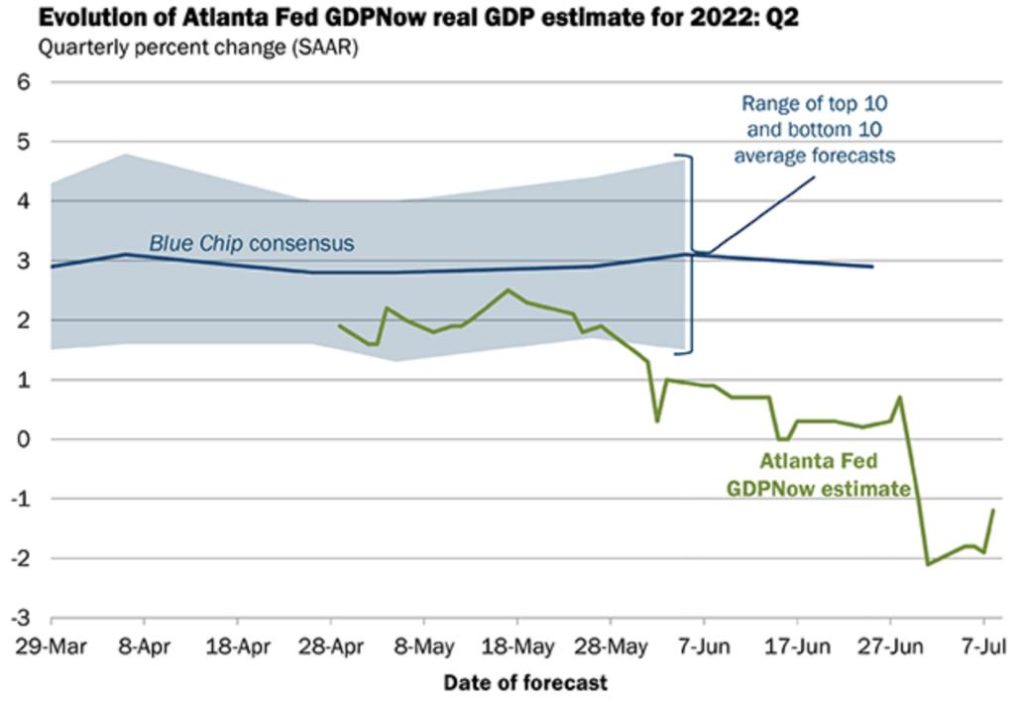

Based on the forward estimate of GDP from the Atlanta Fed (above) we have a high likelihood of sinking into a recession when the 1st estimate of Q2 is released later this month. Their estimate has ranged as low as -2% in the last two weeks. Regardless, we are in the midst of one of the most painful drawdowns in memory. The only positive performer on the year is commodities. Bonds have been crushed, something we anticipated and worked to hedge against. Equities across the board have been wiped out. It feels like we are in a recession, and feelings may be what matters most when it comes down to it. Expectations are powerful drivers of consumer sentiment and behavior.

THE JOB MARKET IS CRUSHING IT, LOTS OF CASH, REASONABLE VALUATIONS

We track 11 primary indicators on a rolling 12-month basis. Of those data points, 6 are doing well, 2 are in good shape, 1 is flashing danger, and 2 make you want to bury your head in the sand and put cash under your mattress. We track forward looking as well as lagging data points. For example, unemployment is a lagging indicator while credit spread is a leading indicator.

Guide to the Markets – U.S. Data are as of June 30, 2022

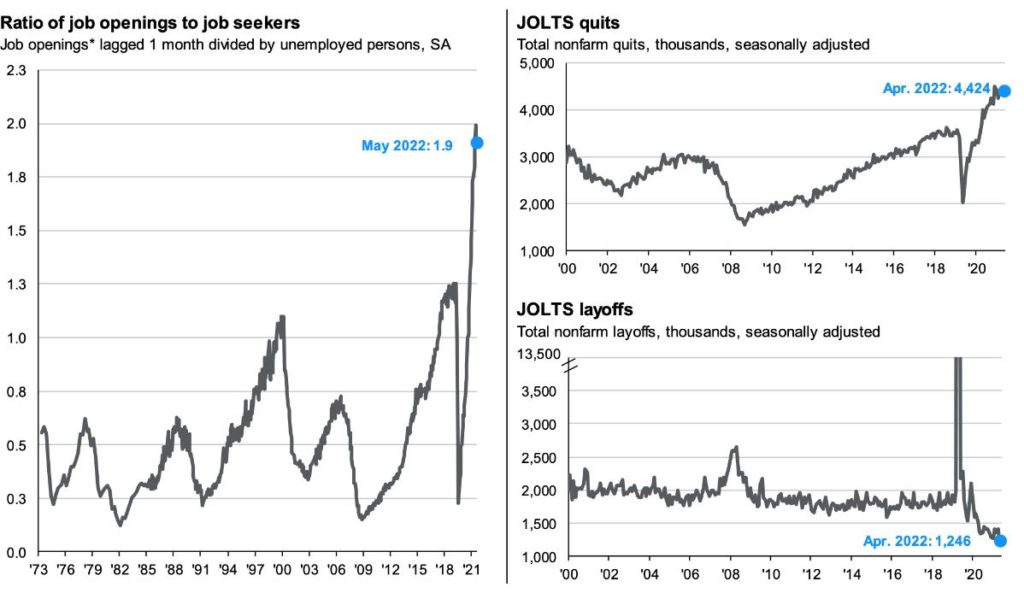

If you haven’t heard, it is a great time to get a job. Looking at the data above starting with the JOLTS Quits graph, you can quit and be in good company, without worrying about being laid-off, and have a high likelihood of finding work that suits you without a whole lot of competition. There are 1.9 job openings per unemployed person and an incredibly low unemployment rate, providing ample encouragement for

people to get out of their current job and make a change. Some will quibble about the unemployment rate being artificially low for not counting those have who pulled themselves out of the labor market, but there is no denying that now is a good time to be looking for work.

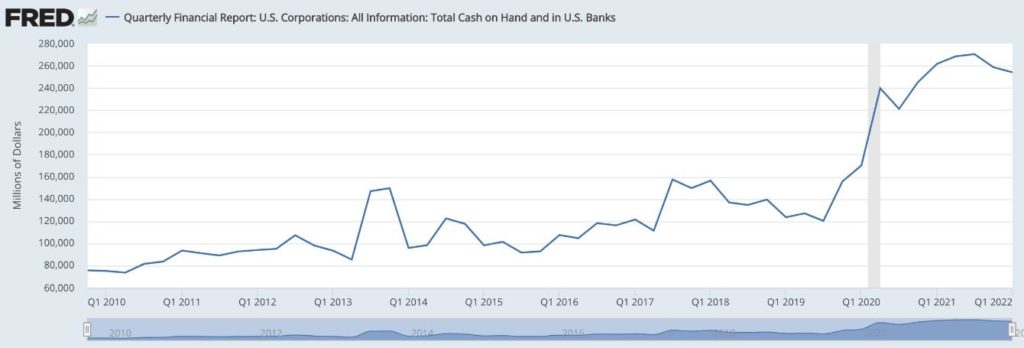

Credit markets are holding up well with a low rate of defaults and a below average rate spread. There is a lot of debt out there, but there is also a lot of cash. While corporate debt accelerated over the last decade of low interest rates, cash on hand also increased, particularly during the pandemic stimulus extravaganza as you can see above. Cheap debt and lots of cash provides a cushion for both households and businesses to tighten up during challenging times. If nothing else, this may provide a longer runway for the Federal Reserve to raise interest rates before economic conditions really begin to deteriorate.

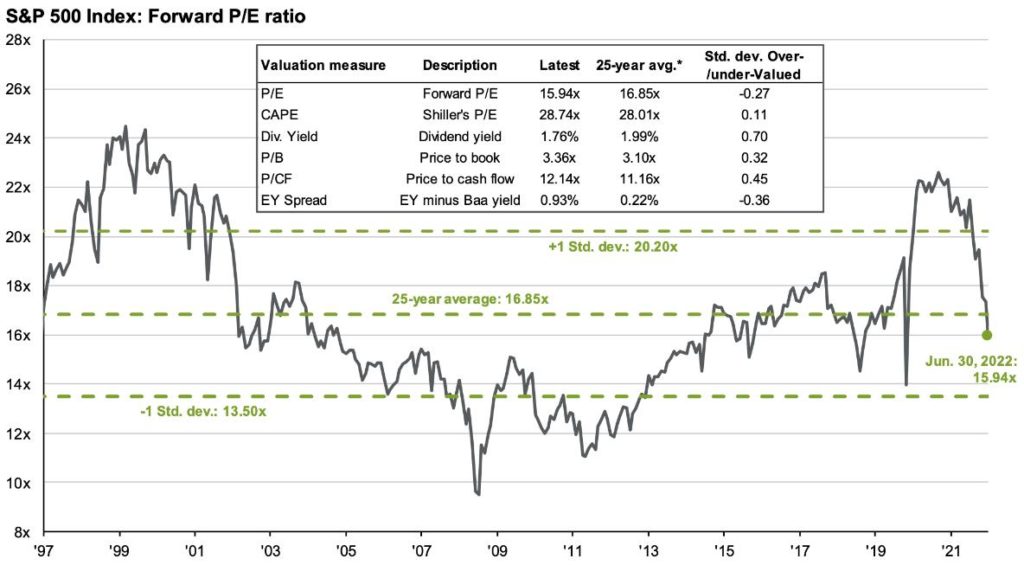

Finally, stock valuations appear reasonable. As you can see above, they have come down below historic averages. Average pricing is not cheap pricing, however, it does help provide a rational basis for arguing against a “sky is falling” mentality. Unless you are Professor Nouriel Roubini, in which case you would think that “the next recession will be both stagflationary and accompanied by a financial crisis, the crash in equity markets could be closer to 50%”. This would be one of the worst downturns in history if his prognostication comes true. We are not anticipating anything along this magnitude with the level of good news we are seeing in the economy.iii

THE BAD NEWS

Leading into recessions the average S&P market drawdown is 32% and the average duration from peak to trough is 381 days, with four data points pulling the average duration down significantly. If those 4 data points are pulled out, the 9 major recessions since the Great Depression have averaged 521 days in length from peak to trough. The data table below provides useful context in putting numbers to what is an otherwise emotional event: the loss of value in our collective portfolios.

The current S&P drawdown is -20%. If we revert to the average recessionary downturn, we still have a ways to drop for an average downturn of -32%. Such a drop would represent an additional 600 points down from where we are currently, hitting 3,235 points on the S&P. History might not repeat, but it does

rhyme. We are roughly 190 days and a 20% drop into a correction. If this becomes a full-blown recession it is not unreasonable to think we are looking at another 12% or greater drawdown spread out over another 6 months, or longer.

An important reminder is that markets tend to recover in a hurry when they hit a trough and if the best days are missed portfolio growth is significantly handicapped. In a recent U.S. News & World Report article Professor Robert Johnson, finance at Creighton University, noted that during “20-year period from Jan.2, 2001, to Dec. 31, 2020, if you missed the top 10 best days in the stock market, your overall return was cut by more than half”. Time in the market is more important than timing the market.iv

INFLATION – NOT LOOKING GOOD

Inflation is high and all signs are pointing to an even worse June measurement. The official pronouncement of June inflation has not been reported as of this writing. However, Press Secretary Jean-Pierre seems to be hedging that the data will be bad. In a recent White House press briefing, she stated that, “June CPI data is already out of date because energy prices have come down substantially this month and are expected to fall further”. This sounds a lot like the White House knows what is coming, higher inflation.

The Federal Reserve language has continued to get less certain which is not very encouraging. Fed Chair Jerome Powell recently said he did not want “to be the handicapper here”, when asked whether or not he thought that a soft-landing was possible. Followed up with, “I think that events of the last few months have raised the degree of difficulty” of a soft-landing. Equivocation is never a confidence boost for the public. Which leads to one of the more frightening unknowns hanging around out there.v

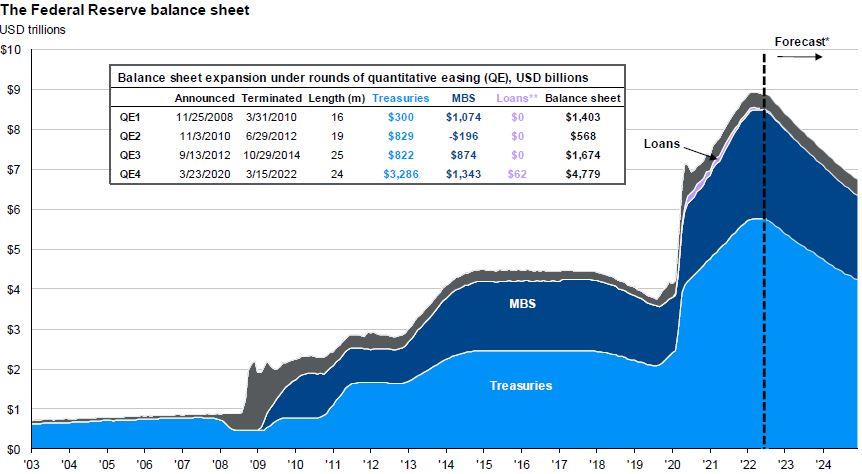

Quantitative Tightening, or QT, is coming. Whether it is innocuous, or not, is unknown. QT has never happened on the scale we are about to see. Central banks around the globe are beginning a coordinated balance sheet run-off and interest rate hiking regime. When the Federal Reserve went on a bond buying spree to shore up credit markets, they did it on a scale unprecedented in size and breadth. When the demand for these bonds and the liquidity provided flips the other direction we could see nothing or something.

Guide to the Markets – U.S. Data are as of June 30, 2022

There is at least one person out there who views QT as a problem and his name is Jamie Dimon, Chairman and Chief Executive of JP Morgan Chase. At a conference in early June he referred to the various headwinds facing the economy as a “hurricane”, with the war in Ukraine and QT by the Federal Reserve as the two most uncertain elements. If the Federal Reserve expanded their balance sheet to provide stability, it is not a stretch to assert that the removal of their support could interject instability.vii

THE PLANNING CORNER

Now is a good time for a Roth IRA conversion. We said this back in April and we are saying it again. When markets are down, and especially if your tax rates are low, look at converting from a Traditional IRA to a Roth. This is not a blanket recommendation. It requires substantial analysis to identify the best path forward. There are tax consequences as well as time horizon issues to think through. If this is something you would like to discuss please let us know.

Tax-loss harvesting is also a good strategy to implement when markets are down. We have been rebalancing through the downturn and doing our best to realize losses to offset gains when the opportunity presents itself. An important caveat is that loss harvesting and wash-sale rules are not necessarily the same for cryptocurrency as they are for stocks. If you have dabbled in cryptocurrency on your own and find yourself with substantial losses in the current crypto sell-off, make sure you understand those differences before making any hasty decisions.

Finally, a brief update on SECURE Act 2.0: there is no new news. The Senate is still working on their changes to the House bill and we hope to have updated in the next newsletter.

As always, our desire is to help you make rational, informed, and well-reasoned decisions, and we thank you for your continued trust and support. Your input is always welcome and we ask that you contact us with any questions or concerns.

DISCLOSURE

All information is believed to be from reliable sources; however we make no representation as to its completeness or accuracy. All economic and performance data is historical and not indicative of future results. Market indices discussed are unmanaged. Investors cannot invest in unmanaged indices. Additional risks are associated with international investing, such as currency fluctuations, political and economic instability and differences in accounting standards.

Investing in securities in emerging markets involves special risks due to specific factors such as increased volatility, currency fluctuations and differences in auditing and other financial standards. Securities in emerging markets are volatile and can decline significantly in response to adverse issuer, political, regulatory, market, or economic developments.

An index is a statistical measure of change in an economy or a securities market. In the case of financial markets, an index is an imaginary portfolio of securities representing a particular market or a portion of it. Each index has its own calculation methodology and is usually expressed in terms of a change from a base value. Thus, the percentage change is more important than the actual numeric value. An investment cannot be made directly into an index.

Investing in fixed income securities involves credit and interest rate risk. When interest rates rise, bond prices generally fall. Investing in commodities may involve greater volatility and is not suitable for all investors. Investing in a non-diversified fund that concentrates holdings into fewer securities or industries involves greater risk than investing in a more diversified fund. The equity securities of small companies may not be traded as often as equity securities of large companies so they may be difficult or impossible to sell. Neither diversification nor asset allocation assure a profit or protect against a loss in declining markets. Past performance is not an indicator of future results.

Sean P. Storck and Steven W. Pollock are registered representatives with and securities and Retirement Plan Consulting Program advisory services offered through LPL Financial, a Registered Investment Advisor. Member FINRA/SIPC. Financial Planning offered through Reason Financial, a state Registered Investment Advisor. Investment advice offered through Merit Financial Group, LLC an SEC Registered Investment Advisor. Merit Financial Group and Reason Financial are separate entities from LPL Financial. Tax related services offered through Reason Tax Group. Reason Tax Group is a separate legal entity and not affiliated with LPL Financial. LPL Financial does not offer tax advice or tax related services. Sean P. Storck CA Insurance Lic#OF25995 and Steven W. Pollock CA Insurance Lic#OE98073

i “Business Cycle Dating Procedure: Frequently Asked Questions.” NBER, National Bureau of Economic Research, 19 July 2021, https://www.nber.org/business-cycle-dating-procedure-frequently-asked-questions#:~:text=Earlier%20determinations%20took%20between%204,accurate%20peak%20or%20trough%20date.

ii “News Release.” Gross Domestic Product (Third Estimate), GDP by Industry, and Corporate Profits (Revised), First Quarter 2022 | U.S. Bureau of Economic Analysis (BEA), Bureau of Economic Analysis (BEA), 29 June 2022, https://www.bea.gov/news/2022/gross-domestic-product-third-estimate-gdp-industry-and-corporate-profits-revised-first.

iii Roubini, Nouriel. “A Stagflationary Debt Crisis Looms: By Nouriel Roubini.” Project Syndicate, Project-Syndicate.org, 4 July 2022, https://www.project-syndicate.org/commentary/stagflationary-debt-crisis-by-nouriel-roubini-2022-06.

iv Dong, Tony. “How to Recover after a Loss in the Stock Market | Investing 101 | US News.” Money.usnews.com, US News & World Report, 5 July 2022, https://money.usnews.com/investing/investing-101/articles/how-to-recover-after-loss-in-the-stock-market.

v “Transcript of Chair Powell’s Press Conference — June 15, 2022.” Www.FederalReserve.gov, Federal Reserve, 15 June 2022, https://www.federalreserve.gov/mediacenter/files/FOMCpresconf20220615.pdf.

vi Daniel, Will. “The Market Is Freaking out Because of the End of Free Money.” Fortune, Fortune, 1 July 2022, https://fortune.com/2022/05/10/investing-regime-change-stock-market-fed-put-end-of-free-money/.

vii “Jamie Dimon: Brace Yourself for an Economic Hurricane | Bernstein Conference Full Interview Video.” YouTube, YouTube, 4 June 2022, https://www.youtube.com/watch?v=2Um32UeiCj0&ab_channel=WallstreetAlmanack.