October 2016 – An Economic and Market Update

AN ECONOMIC AND MARKET UPDATE

Quarterly Market Update – October 2016

![]()

- The markets have performed well since the “Brexit”, but we still have a long way to go until we hear the final words on the United Kingdom leaving the European Union.

- Though past performance does not guarantee future results, growth in the stock market has historically continued on an upward and onward trek despite the political leanings of the person sitting in the Oval Office.

- Infrastructure spending is a campaign trail talking point, but how those dollars get allocated is more important.

- The Federal Reserve continues their low interest rate policy while registering concern about the persistently low-inflation environment.

LOOKING BACK

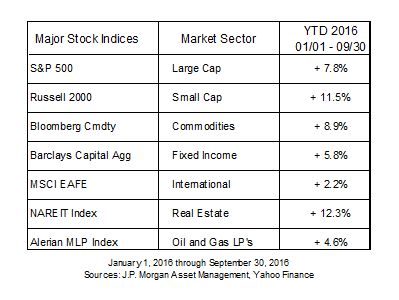

The great news is that the markets have performed well and have performed steadily. In fact, since the British vote to leave the EU, global markets have moved significantly higher. Initial panic over the “Brexit” has subsided and it seems the world has turned its attention to the Presidential election in the United States and the continuing global refugee crisis.

TO MARMITE OR NOT TO MARMITE

For the United Kingdom the clock is ticking. Prime Minister Theresa May has indicated she will invoke Article 50 of the Lisbon Treaty by the end of March 2017. The question of the day is not, “When?”, but rather, “How?”. The most commonly heard descriptor for the method of Brexit, Hard or Soft, is an oversimplification of the process and more commonly associated with cooking eggs than navigating a complicated set of international agreements and accords.[i]

At the end of the day the debate is about integration within the European Union. The integration will either be significant (Soft) or limited (Hard). The Prime Minister recently gave a speech discussing the ongoing process and made the following comment: “If you believe you’re a citizen of the world, you’re a citizen of nowhere. You don’t understand what the very word citizenship means.” If you view the referendum vote primarily as a pushback against globalization, the nationalistic tone of her speech should serve as an indicator that she will be pushing for an exit leaning towards the “Hard” side of the aisle with less control of United Kingdom policies being ceded to the European Union. The players are known, the clock has been set and early observers are skeptical the situation will resolve nicely with one commentator describing the situation as, “Britain is hurtling towards the worst of all worlds – a swift, hard Brexit on unfavorable trade terms.” As a reference to our section header, the first major victim of a hard Brexit and a falling Pound appears to be Marmite, an obscure sandwich spread beloved by Brits but made by a global conglomerate currently losing money due to currency fluctuations. Boiling eggs is surprisingly complicated after all.[ii]’[iii]’[iv]

SPEAKING OF HALF-BAKED

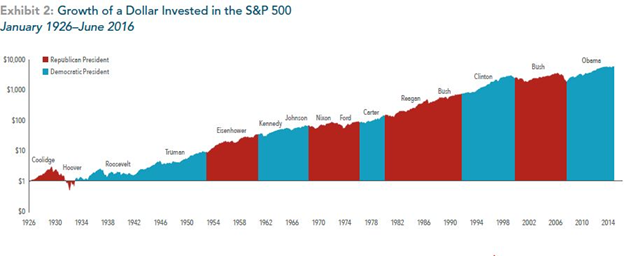

The election in the United States carries on with one month until we officially cast ballots on Nov. 8th to determine the lucky recipient of the hardest job in the world. The good news for investors: historically, it has not made a difference to the stock markets whether or not Republicans or Democrats are in power.

Past performance is not a guarantee of future results. Indices are not available for direct investment; therefore, their performance does not reflect the expenses associated with the management of an actual portfolio. The S&P data is provided by Standard & Poor’s Index Services Group.

The graph above covers every Presidency since 1926, with the most easily determinable pattern being one of steady, upward growth. If anything, this should help us see that every President has bourne the political brunt of at least one market downturn during their time in office, but generally the market has trended up over time.[v]

INFRASTRUCTURE: BRIDGES TO NOWHERE

In the current political climate it is easy to turn on the television, listen to the radio, open your email, or answer a phone call and hear how different the two candidates are and how one is going to save the country while the other is going to destroy it. Based on prior history, the rhetoric does not really match up to reality. In fact, we would like to take this opportunity to look at one issue both candidates believe strongly in, and which we believe is integral to the future growth of our country when approached intelligently: increased spending on infrastructure

The Dwight D. Eisenhower Interstate Highway System is the second longest Interstate system in the world, behind China of course. As all infrastructure projects go, it was dramatically over budget – the original estimate of $25 billion over 12 years became a $114 billion cost over 35 years (non-inflation adjusted dollars). The value of the Interstate System, despite the cost overruns, is indisputable and probably incalculable. Transportation, transit, strategic defense, and myriad other benefits are provided by the system. In the memoir of his first term, President Eisenhower stated that, “Its impact on the American economy – the jobs it would produce in manufacturing and construction, the rural areas it would open up – was beyond calculation.” With the benefit of hindsight, he was right.[vi]

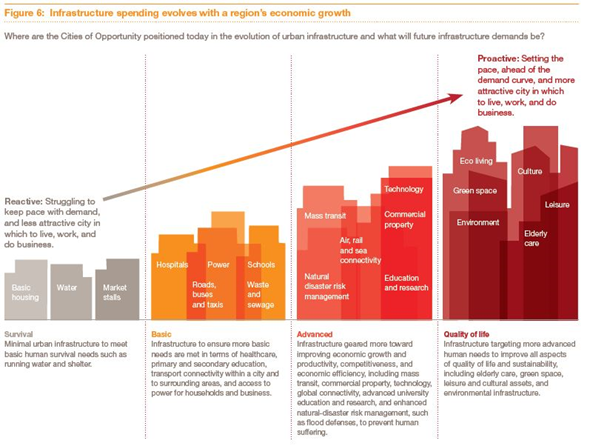

Source: PWC, Cities of Opportunity: Building the Future, November 2013

The Interstate System is a great example of a mix between Basic and Advanced infrastructure combining elements of roads with mass transit and connectivity. The United States is at an inflection point where most new building will be a mix of Advanced/Quality of Life. In fact, if you look at the most ambitious public infrastructure projects going on right now, you will see that they are mostly focused on urban areas. For example:[vii]

1. Second Avenue Subway Line in New York City (self-explanatory)

2. Chicago’s Loop Link BRT (more efficient bus route)

3. Gateway Project (intercity rail line connecting New Jersey and New York)

4. Cleveland’s Public Square (project prioritizing pedestrians over vehicles)

5. Seattle’s Alaskan Way Viaduct (moving a freeway underground opening up coastal development and connectivity similar to the Big Dig in Boston)

The big problem with infrastructure spending is two-fold: vast dollars floating around combined with a lack of accountability to oversee those projects. Harvard based economist Edward Glaeser recently said that his, ‘biggest fear is that we’re not actually going to fix the biggest problems we have. Instead we’ll just end up with more highways in North Dakota or more white elephant projects that deliver little value.” With one Presidential hopeful proposing to spend $275 billion over 5 years, the other candidate vowing to “at least double” that, and President Obama being on record for $478 billion over six years as being the right amount, our hope is that the dollars are spent wisely. In a best case scenario we end up with funds being spent to maintain the crumbling and aging infrastructure we have, such as the Interstates, and a wise mix of high value investments targeted to reach domestic goals. What we don’t need is “too much spending on new roads, and not enough maintenance for existing roads.”[viii]’[ix]

Just in case you were wondering, the final tally for the Interstate Highway System was $511 billion in 2015 inflation adjusted dollars. It is unlikely that any system of projects recommended by our future President will be as productive as the InterState System, however, with the right mix of projects and oversight it could be a boon for the country, setting the stage for years to come.[x]

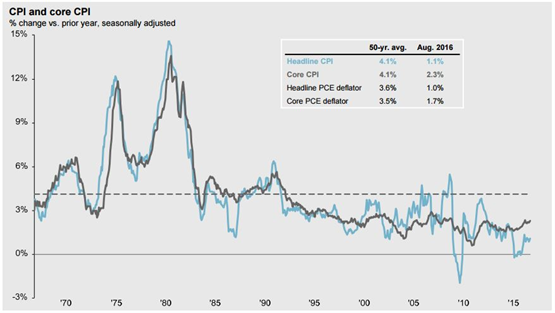

THE FED WATCH

The Federal Reserve is sticking to their current target of interest rates being maintained between a quarter-point and a half-point. While borrowers may rejoice, this indicates that inflation continues to struggle to reach healthy levels. As we have mentioned before, the Federal Reserve has two important mandates: maintain full employment and keep inflation stable. The good news is that Unemployment, currently at 4.9%, is low relative to the 50-year average of 6.2%. The not-so-encouraging news, inflation is stubbornly stuck beneath the Fed target of 2%. Lack of growth has a cascading effect across the economy with repercussions in wage growth, Cost-of-Living-Adjustments (COLAs), heightened risk of slipping into deflation, increase cost in debt payments, lack of tools available to combat future recessions, etc.[xi]’[xii]

Source, BLS, FactSet, J.P. Morgan Asset Management

In the most recent meeting minutes of the Federal Reserve from September 21, 2016 it was noted that, “consistent with its statutory mandate, the committee seeks to foster maximum employment and price stability.” Also noted was that, “near term risks to the economic outlook appear roughly balanced.” These two statements serve as circumstantial evidence to support the current status of our economy being static. If our economy was a movie, it would be the most boring movie ever.

LOOKING FORWARD

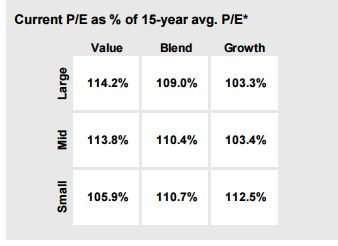

Earnings reporting season for publicly traded companies has started and P/E (Price to Earnings) ratios for most sectors of the market are high as represented by the following chart. With high prices come high expectations. When expectations aren’t met the potential for volatility increases.

Source: FactSet, Russell Investment Group, Standard & Poor’s, J.P. Morgan Asset Management.

We believe we are in a period of heightened risk to the markets at this time. We will be rebalancing as our criteria are met and using market volatility as an opportunity to put cash to work.

We thank you for your continued trust and support. Your input is always welcome and we ask that you contact us with any questions or concerns.

DISCLOSURE

All information is believed to be from reliable sources; however we make no representation as to its completeness or accuracy. All economic and performance data is historical and not indicative of future results. Market indices discussed are unmanaged. Investors cannot invest in unmanaged indices. Additional risks are associated with international investing, such as currency fluctuations, political and economic instability and differences in accounting standards.

Investing in securities in emerging markets involves special risks due to specific factors such as increased volatility, currency fluctuations and differences in auditing and other financial standards. Securities in emerging markets are volatile and can decline significantly in response to adverse issuer, political, regulatory, market, or economic developments.

An index is a statistical measure of change in an economy or a securities market. In the case of financial markets, an index is an imaginary portfolio of securities representing a particular market or a portion of it. Each index has its own calculation methodology and is usually expressed in terms of a change from a base value. Thus, the percentage change is more important than the actual numeric value. An investment cannot be made directly into an index.

Investing in fixed income securities involves credit and interest rate risk. When interest rates rise, bond prices generally fall. Investing in commodities may involve greater volatility and is not suitable for all investors. Investing in a non-diversified fund that concentrates holdings into fewer securities or industries involves greater risk than investing in a more diversified fund. The equity securities of small companies may not be traded as often as equity securities of large companies so they may be difficult or impossible to sell. Neither diversification nor asset allocation assure a profit or protect against a loss in declining markets. Past performance is not an indicator of future results.

Securities offered through 1st Global Capital Corp., Member FINRA and SIPC. Bruce Rawdin-Baron, Steven W. Pollock, Sean P. Storck, Matthew J. Anderson and Nicole Albrecht are Registered Representatives of 1st Global Capital Corp. Investment advisory services, including RBFI portfolios offered through Reason Financial. IMS platform accounts offered through 1st Global Advisors, Inc. Reason Financial. and 1st Global Capital Corp. are unaffiliated entities. Reason Financial is a Registered Investment Adviser. Placing business through 1st Global Insurance Services. Registration does not imply a certain level of skill or training. We currently have individuals licensed to offer securities in the states of Arizona, California, Illinois, Indiana, Kansas, Massachusetts, Michigan, New York, Oregon and Washington. This is not an offer to sell securities in any other state or jurisdiction. CA Department of Insurance License: Bruce Rawdin-Baron #0736631, Steven W. Pollock #OE98073, Sean P. Storck #0F25995, Matthew J. Anderson #0F21959 and Nicole Albrecht #0F99962.

Copyright © 2016 Reason Financial all rights reserved.

Reason Financial

4747 Morena Blvd, Suite 102, San Diego, CA 92117

ENDNOTES

[i] “Theresa May Kicks Off Brexit.” The Economist, 2 Oct. 2016, http://www.economist.com/node/21708078

[ii] May, Theresa. “A Country That Works For Everyone.” Tory Party Conference, 5 Oct 2016, Birmingham, England, Keynote Address. http://www.telegraph.co.uk/news/2016/10/05/theresa-mays-conference-speech-in-full/

[iii] De Freytas-Tamura, Kimiko. “Marmite Survives After ‘Brexit’ Spurs Tesco-Unilever Price Dispute.” NYTimes, 13 Oct 2016, http://www.nytimes.com/2016/10/14/business/international/marmite-brexit-britain.html

[iv] Taylor, Paul. “Britain’s Brexit Delusions.” Politico, 11 Oct. 2016, http://www.politico.eu/article/theresa-may-tories-britain-uk-brexit-eu-deal-delusions-negotiations/

[v] “Presidential Elections and the Stock Market.” Dimensional Fund Advisors, October 2016

[vi] “Interstate Highway System.” Wikipedia:The Free Encyclopedia. Wikimedia Foundation, Inc. 11 Oct. 2016. Web. 13 Oct. 2016

[vii] Jaffe, Eric. “The Big U.S. Transportation Infrastructure Projects to Watch in 2016.” The Atlantic. 22 Dec. 2015. http://www.citylab.com/commute/2015/12/us-infrastructure-projects-2016-transportation/421431/

[viii] Jacobson, Louis. “Compare the Candidate: Clinto vs. Trump On the Economy.” Politifact. 22 July 2016. http://www.politifact.com/truth-o-meter/article/2016/jul/22/comparing-economic-agendas-hillary-clinton-and-don/

[ix] Plumer, Brad. “The One Thing Trump and Clinton Agree On Is Infrastructure. This Economist Thinks They’re Both Wrong.” Vox. 4 Oct. 2016. http://www.vox.com/policy-and-politics/2016/10/4/13121058/trump-clinton-infrastructure-economics-glaeser

[x] Interstate Highway System.” Wikipedia:The Free Encyclopedia. Wikimedia Foundation, Inc. 11 Oct. 2016. Web. 13 Oct. 2016

[xi] Federal Reserve Press Release. Federal Reserve. 21 Sept. 2016. https://www.federalreserve.gov/monetarypolicy/files/monetary20160921a1.pdf

[xii] “The Perils of Falling Inflation.” The Economist. 9 Nov. 2013. http://www.economist.com/news/leaders/21589424-both-america-and-europe-central-bankers-should-be-pushing-prices-upwards-perils-falling

Disclosure

This material is for general information only and is not intended to provide specific advice or recommendations for any individual. There is no assurance the views or strategies discussed are suitable for all investors or will yield positive outcomes. Investing involves risks including possible loss of principal. Any company names noted herein are for educational purposes only.

All information is believed to be from reliable sources; however we make no representation as to its completeness or accuracy. All economic and performance data is historical and not indicative of future results. Market indices discussed are unmanaged. Investors cannot invest in unmanaged indices. Additional risks are associated with international investing, such as currency fluctuations, political and economic instability and differences in accounting standards.

Investing in securities in emerging markets involves special risks due to specific factors such as increased volatility, currency fluctuations and differences in auditing and other financial standards. Securities in emerging markets are volatile and can decline significantly in response to adverse issuer, political, regulatory, market, or economic developments.

An index is a statistical measure of change in an economy or a securities market. In the case of financial markets, an index is an imaginary portfolio of securities representing a particular market or a portion of it. Each index has its own calculation methodology and is usually expressed in terms of a change from a base value. Thus, the percentage change is more important than the actual numeric value. An investment cannot be made directly into an index.

Investing in fixed income securities involves credit and interest rate risk. When interest rates rise, bond prices generally fall. Investing in commodities may involve greater volatility and is not suitable for all investors. Investing in a non-diversified fund that concentrates holdings into fewer securities or industries involves greater risk than investing in a more diversified fund. The equity securities of small companies may not be traded as often as equity securities of large companies so they may be difficult or impossible to sell. Neither diversification nor asset allocation assure a profit or protect against a loss in declining markets. Past performance is not an indicator of future results.

Financial Planning offered through Reason Financial, a state Registered Investment Advisor. Investment advice offered through Merit Financial Group, LLC an SEC Registered Investment Advisor. Merit Financial Group and Reason Financial are separate entities. Tax related services offered through Reason Tax Group. Reason Tax Group is a separate legal entity and not affiliated with Merit Financial Group, LLC. Sean P. Storck CA Insurance Lic#OF25995 and Steven W. Pollock CA Insurance Lic#OE98073

Copyright © 2026 Reason Financial all rights reserved.

Continue Reading

2nd Quarter 2026 – Economic and Market Update

Q1 2026 in review: oil shock, S&P 500 down 4.3%, commodities up 24.4%, the cease-fire that became a blockade — and the planning moves that matter most coming out of a quarter like this one.

It’s Now More Common To Have A Baby In Your Thirties Than In Your Twenties

DisclosureThis material is for general information only and is not intended to provide specific advice or recommendations for any individual.…

When Does Refinancing Actually Make Sense? A 2026 Reality Check

If you locked in a mortgage at 7% or higher in 2023 or 2024, you’ve probably been watching rates with…