October 2017 – An Economic and Market Update

AN ECONOMIC AND MARKET UPDATE

Quarterly Market Update – October 2017

![]()

- Harvey is now the most expensive weather event in US history. With continued development in coastal areas this is unlikely to remain the case.

- Economic modeling of storms in the Pacific shows long-term negative impacts on income providing insight to what may happen in the US if extreme weather becomes more frequent.

- The Federal Reserve is having a hard time reaching their target for inflation. The recent acquisition of Whole Foods by Amazon provides us with clues as to why.

- President Trump has proposed significant changes to the tax code. The proposal generates more questions than it provides answers.

LOOKING BACK

From a human perspective the last quarter was a sad one. The various storms, fires, earthquakes and tragedies like Las Vegas impacted millions and millions of lives. For those living within range of North Korea it was/is a time of uncertainty as world leaders debate how to respond in light of North Korean advances in ballistic missile and nuclear weapon technologies.

This is in stark contrast to stock market advancement amid a brightening global economic outlook. In the most recent Federal Reserve meeting minutes, board members stated, “that their business contacts appeared to have become more confident about the economic outlook, and it was noted that the National Federation of Independent Business reported that greater optimism among small businesses had contributed to a sharp increase in the proportion of small firms planning increases in their capital expenditures.” This is great news as increasing capital expenditures are strong drivers of long term growth.[i]

THE ECONOMIC IMPACT OF MAJOR STORMS ON THE US

Acts of god did their best to slow things down. Harvey, Irma, and Maria will have an economic impact on the United States. In particular, Hurricane Harvey will (has) caused a measurable ripple effect across the country. Houston is a large part of the domestic economy as seen below. The Employment Situation – September 2017, update from the Bureau of Labor Statistics was clear on this point. “A sharp employment decline in food services and drinking places and below-trend growth in some other industries likely reflected the impact of Hurricanes Irma and Harvey.”[ii] . Citi Investment Bank has estimated the negative impact of Harvey at .2-.3% of GDP.[iii]

Source: Quarts Media and Citi[iv]

On a positive note, the Federal Reserve believes the slowdown will be absorbed and pass through with little impact. “Storm related disruptions and rebuilding will affect economic activity in the near term, but past experience suggests that the storms are unlikely to materially alter the course of the national economy over the medium term.”[v]

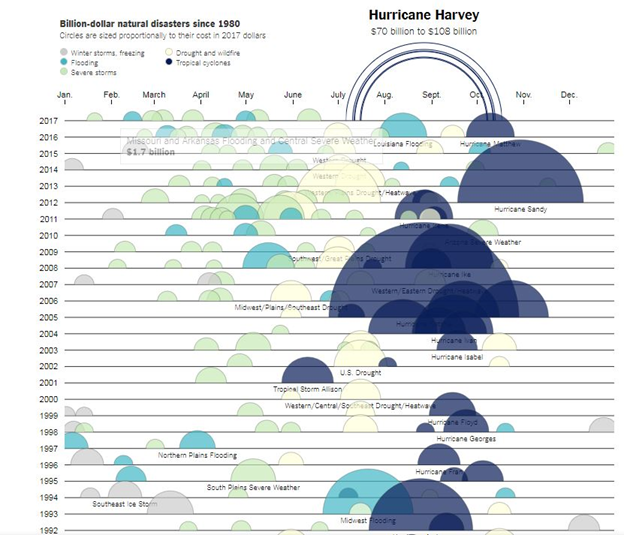

That said, Houston could be a turning point in our collective conscious. On September 1st early estimates for the cost of Hurricane Harvey were $108 billion. The NY Times created an interactive graph on major storm events in recent US history. It is worth a look if you have time, a non-interactive version is captured below:[vi]

The Cost of Hurricane Harvey: Only One Recent Storm Comes Close by Kevin Quealy, Sept. 1, 2017[vii]

Harvey has become the costliest storm in US history as damage estimates have been revised upwards to $190 billion. Political views on climate change notwithstanding, the cost of storm damage will continue to rise. For example, Florida today is far more developed than ever before with 9 of its cities in the top 25 fastest growing cities of 2017. Storms will cost more in damage because there is more to destroy. If climate science estimates prove true, stronger and more consistent storms will magnify that damage accelerating costs faster.[viii]

Unknown are the long-term effects of increasing storm frequency and ever higher costs of damage. It will become economically inefficient to re-invest in an area where the likelihood of destruction runs high. The US has managed to come out of most recent disasters well because of our infrastructure, building codes, quality of response and resilience. The question is, when will the frequency of storms begin to have a long-term negative impact rather than just a short to mid-term effect?

THE ECONOMIC IMPACT OF MAJOR STORMS GLOBALLY

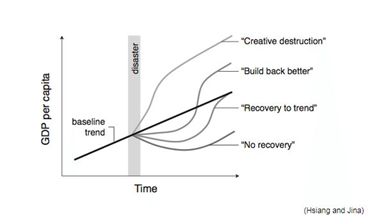

This is concerning because a comprehensive study of storms in the South and West Pacific offers rather depressing conclusions to the economic impact of storms should they become more consistent. In, The Causal Effect of Environmental Catastrophe On Long-Run Economic Growth: Evidence From 6,700 Cyclones, the economists Hsiang and Jina strive to get to the bottom of whether or not acts of God have long-term impacts on an economy. There are four prevailing economic views of growth out of a catastrophe:

Figure 1: Four hypotheses, proposed in the literature, that describe the long-term evolution of GDPpc following a natural disaster.

Creative Destruction is the idea that there will be a stimulus to the economy as the demand for goods and services increase due to the replacement of lost capital and an influx of aid.

Build Back Better is the idea that there will be a loss in productive capital but there will be a net positive effect in the long run as old capital is replaced with new and better capital.

Recovery to Trend is merely a return to business as usual via accelerated recovery in the beginning.

No Recovery is the argument that disasters slow growth for a long time due to the recovery not being sufficient to outweigh the costs.

If the long run view is that we will experience more extreme weather events, finding the most relevant of these four models is an important undertaking. The South Pacific provides us with some answers. They have been getting seasonal powerful storms for a long time and with consistent frequency to measure the economic impact over time.

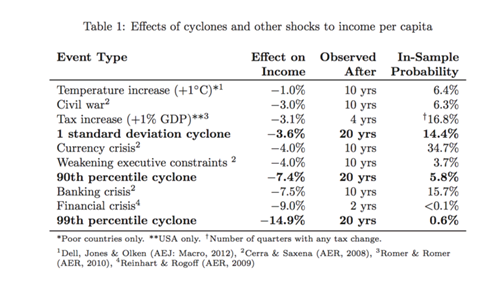

The table above documents the results. As it turns out, storms are just as damaging, if not more, than other economic events with their effects being felt as far out as 20 years in to the future. The bolded data represent storm events. A 99th percentile event being the most catastrophic and akin to what Puerto Rico is dealing with right now after Hurricanes Irma and Maria. Other economic crises are represented in the table with their impact as well. The study is explicit in communicating that these effects are, “’globally valid’ in the sense that it holds around the world, appearing in each region independently and for countries of different income and geographic size.” Rich country, poor country, large country and small country; it does not matter, there are measurable long term negative effects to income.

From a global perspective this increases the long-term dollar cost of climate change dramatically with an estimate of $9.7 trillion dollars. From a US only point of view, it is rational to expect we would begin to see long-term effects here if these events begin to take place more frequently. The impact of a storm event today might have mid-term consequences as communicated by the Federal Reserve. This data should tell us that may not always be the case.[x]

THE CONFOUNDED FEDERAL RESERVE

The Federal Reserve has taken a break from increasing interest rates. At the meeting on September 20, 2017, the Board of Governors decided to maintain an accomodative stance by maintaining the Fed Funds Rate target range of 1-1.25%. The 2% target for inflation remains, however, with an August measurement of 1.9%, it is proving hard to reach. Former adviser to Chair Janet Yellen, John Faust, recently stated in the Financial Times, “It is a puzzle and raises a real question what the Fed should do next: I would have thought we would have been seeing more inflation pressures by now.”[xi]

The recent acquisition of Whole Foods by Amazon provides an example of the quandary facing policy makers. Immediately after acquiring Whole Foods, significant price decreases across the board were announced. As has been their propensity, Amazon has begun to disrupt a new industry which has been mired in mediocrity for a long time, grocers. These changes are really just one more example of how there are two worlds colliding: Brick and Mortar vs Digital.

It appears at least part of the frustration in goosing inflation may be continued disruption from the online world. The collective conscious of the internet created changes which are still confounding and unknown. The Fed might be fighting against a battle they do not actually know how to win with the current tools in their tool chest.

As the chart above indicates, deflation in the online world is much more significant than in the brick and mortar world. If you are not taking advantage of lower prices online, there is no better time than the present to jump in. Consumer gain in purchasing power online may be a large contributor to the challenges facing the Fed in reaching their 2% inflation target.

LOOKING FORWARD

The extension deadline for filing personal income tax returns is now in our rear view mirror. This demarcation point in the calendar serves as a proxy for the biggest unknown we have looming right now. If President Trump has anything to say about it, the future of taxes will look very different. His current proposal is a 9 page document called the Unified Framework For Fixing Our Broken Tax Code. He is proposing the most sweeping changes to the tax code in decades. In all honesty, it is really hard to make any claim for or against the proposal at this time due to the ambiguity of the language.

Some of it sounds good

1. Doubling the standard deduction – this is a BOON for most of the country as only 29% of filers actually itemize at this time.[xii]

2. Postcard tax filing – simplifying the tax code is a noble goal most people can get behind.

3. Reduction in C Corporation tax rates – this brings the US in line with the rest of the developed world.

Some of it sounds like a nod to the wealthy

1. Repeal of the Estate Tax and Generation Skipping Transfer Tax – 99.8% of all estates pay no estate tax. It is hard to argue that this benefits anyone other than the most wealthy.

Most of it is too ambiguous to tell

“The framework contemplates that the committees…”, this is a statement made often in the proposal. It means that the President is painting with really broad strokes and the details are to be worked out by legislators in committee. Tax reform could be a benefit for the country if done thoughtfully. It could also be a destructive force if not implemented well.[xiii]

The unfortunate experience of Kansas serves as an example for what can go wrong when tax reform is done poorly. In 2012 the Republican led state passed massive tax cuts and tax reform. Unfortunately, they managed to open up significant loopholes gutting the revenue base leading to massive budget cuts impacting essential services. Earlier this year the Republican legislature revolted against the governor and raised taxes in order to get the budget back on track.[xiv]

Tax reform is a big picture issue. We will be watching carefully to see which direction this goes as it will have serious planning consequences to our clients.

We are here to help you make rational, informed and well-reasoned decisions. We thank you for your continued trust and support. Your input is always welcome and we ask that you contact us with any questions or concerns.

DISCLOSURE

All information is believed to be from reliable sources; however we make no representation as to its completeness or accuracy. All economic and performance data is historical and not indicative of future results. Market indices discussed are unmanaged. Investors cannot invest in unmanaged indices. Additional risks are associated with international investing, such as currency fluctuations, political and economic instability and differences in accounting standards.

Investing in securities in emerging markets involves special risks due to specific factors such as increased volatility, currency fluctuations and differences in auditing and other financial standards. Securities in emerging markets are volatile and can decline significantly in response to adverse issuer, political, regulatory, market, or economic developments.

An index is a statistical measure of change in an economy or a securities market. In the case of financial markets, an index is an imaginary portfolio of securities representing a particular market or a portion of it. Each index has its own calculation methodology and is usually expressed in terms of a change from a base value. Thus, the percentage change is more important than the actual numeric value. An investment cannot be made directly into an index.

Investing in fixed income securities involves credit and interest rate risk. When interest rates rise, bond prices generally fall. Investing in commodities may involve greater volatility and is not suitable for all investors. Investing in a non-diversified fund that concentrates holdings into fewer securities or industries involves greater risk than investing in a more diversified fund. The equity securities of small companies may not be traded as often as equity securities of large companies so they may be difficult or impossible to sell. Neither diversification nor asset allocation assure a profit or protect against a loss in declining markets. Past performance is not an indicator of future results.

Securities offered through 1st Global Capital Corp., Member FINRA and SIPC. Bruce Rawdin-Baron, Steven W. Pollock, Sean P. Storck, Matthew J. Anderson and Nicole Albrecht are Registered Representatives of 1st Global Capital Corp. Investment advisory services, including RBFI portfolios offered through Reason Financial. IMS platform accounts offered through 1st Global Advisors, Inc. Reason Financial. and 1st Global Capital Corp. are unaffiliated entities. Reason Financial is a Registered Investment Adviser. Placing business through 1st Global Insurance Services. Registration does not imply a certain level of skill or training. We currently have individuals licensed to offer securities in the states of Arizona, California, Illinois, Indiana, Kansas, Massachusetts, Michigan, New York, Oregon and Washington. This is not an offer to sell securities in any other state or jurisdiction. CA Department of Insurance License: Bruce Rawdin-Baron #0736631, Steven W. Pollock #OE98073, Sean P. Storck #0F25995, Matthew J. Anderson #0F21959 and Nicole Albrecht #0F99962.

Copyright © 2017 Reason Financial all rights reserved.

Reason Financial

4747 Morena Blvd, Suite 102, San Diego, CA 92117

ENDNOTES

-

[i] “Minutes of the Federal Open Market Committee September 19-20, 2017.” www.federalreserve.gov, 20 Sept. 2017, www.federalreserve.gov/monetarypolicy/files/fomcminutes20170920.pdf.

[ii] Bureau of Labor Statistics. Press Office. The Employment Situation – September 2017.www.bls.gov/news.release. Bureau of Labor Statistics, 6 Oct. 2017. Web. 12 Oct. 2017.

[iii] Brinded, Lianna. “Hurricane Harvey Is Hitting 3% of the US Economy.” Quartz, Quartz, 30 Aug. 2017, qz.com/1065737/hurricane-harvey-citi-research-on-harveys-impact-on-us-gdp-economy-jobs/.

[iv] Brinded, Lianna. “Hurricane Harvey Is Hitting 3% of the US Economy.” Quartz, Quartz, 30 Aug. 2017, qz.com/1065737/hurricane-harvey-citi-research-on-harveys-impact-on-us-gdp-economy-jobs/.

[v] Federal Reserve. Federal Open Market Committee. Federal Reserve Press Release. N.p., 20 Sept. 2017. Web. 12 Oct. 2017.

[vi] Rice, Doyle. “Harvey to Be Costliest Natural Disaster in U.S. History, Estimated Cost of $190 Billion.” USA Today, Gannett Satellite Information Network, 31 Aug. 2017, www.usatoday.com/story/weather/2017/08/30/harvey-costliest-natural-disaster-u-s-history-estimated-cost-160-billion/615708001/.

[vii] Quealy, Kevin. “The Cost of Hurricane Harvey: Only One Recent Storm Comes Close.” The New York Times, The New York Times, 1 Sept. 2017, www.nytimes.com/interactive/2017/09/01/upshot/cost-of-hurricane-harvey-only-one-storm-comes-close.html.

[viii] Sharf, Samantha. “America’s Fastest Growing Cities 2017.” www.Forbes.com, Forbes, 10 Feb. 2017, www.forbes.com/sites/samanthasharf/2017/02/10/americas-fastest-growing-cities-2017/#2cdfad0ec312.

[ix] Hsiang, Solomon, and Amir Jina. “The Causal Effect of Environmental Catastrophe on Long-Run Economic Growth: Evidence From 6,700 Cyclones.” NBER Working Paper Series, July 2014, doi:10.3386/w20352.

[x] Hsiang, Solomon, and Amir Jina. “The Causal Effect of Environmental Catastrophe on Long-Run Economic Growth: Evidence From 6,700 Cyclones.” NBER Working Paper Series, July 2014, doi:10.3386/w20352.

[xi] Fleming, Sam. “Nobody Seems to Know Why There Is No US Inflation.” Financial Times, Financial Times, 18 Sept. 2017, www.ft.com/content/bad8bfa4-9a2f-11e7-b83c-9588e51488a0.

[xii] “Average Itemized Deductions.” www.cchgroup.com, Wolters Kluwer, www.cchgroup.com/news-and-insights/wbot2017/average-itemized-deductions.

[xiii] United States, Treasury Department, “Unified Framework For Fixing Our Broken Tax Code.” Unified Framework For Fixing Our Broken Tax Code.

[xiv] Steyer, Tom. Kansas’ Tax Cuts Are a Spectacular Failure. Meanwhile, In California… 22 June 2017, www.latimes.com/opinion/op-ed/la-oe-steyer-kansas-tax-cuts-brownback-california-20170622-story.html

Disclosure

This material is for general information only and is not intended to provide specific advice or recommendations for any individual. There is no assurance the views or strategies discussed are suitable for all investors or will yield positive outcomes. Investing involves risks including possible loss of principal. Any company names noted herein are for educational purposes only.

All information is believed to be from reliable sources; however we make no representation as to its completeness or accuracy. All economic and performance data is historical and not indicative of future results. Market indices discussed are unmanaged. Investors cannot invest in unmanaged indices. Additional risks are associated with international investing, such as currency fluctuations, political and economic instability and differences in accounting standards.

Investing in securities in emerging markets involves special risks due to specific factors such as increased volatility, currency fluctuations and differences in auditing and other financial standards. Securities in emerging markets are volatile and can decline significantly in response to adverse issuer, political, regulatory, market, or economic developments.

An index is a statistical measure of change in an economy or a securities market. In the case of financial markets, an index is an imaginary portfolio of securities representing a particular market or a portion of it. Each index has its own calculation methodology and is usually expressed in terms of a change from a base value. Thus, the percentage change is more important than the actual numeric value. An investment cannot be made directly into an index.

Investing in fixed income securities involves credit and interest rate risk. When interest rates rise, bond prices generally fall. Investing in commodities may involve greater volatility and is not suitable for all investors. Investing in a non-diversified fund that concentrates holdings into fewer securities or industries involves greater risk than investing in a more diversified fund. The equity securities of small companies may not be traded as often as equity securities of large companies so they may be difficult or impossible to sell. Neither diversification nor asset allocation assure a profit or protect against a loss in declining markets. Past performance is not an indicator of future results.

Financial Planning offered through Reason Financial, a state Registered Investment Advisor. Investment advice offered through Merit Financial Group, LLC an SEC Registered Investment Advisor. Merit Financial Group and Reason Financial are separate entities. Tax related services offered through Reason Tax Group. Reason Tax Group is a separate legal entity and not affiliated with Merit Financial Group, LLC. Sean P. Storck CA Insurance Lic#OF25995 and Steven W. Pollock CA Insurance Lic#OE98073

Copyright © 2026 Reason Financial all rights reserved.

Continue Reading

2nd Quarter 2026 – Economic and Market Update

Q1 2026 in review: oil shock, S&P 500 down 4.3%, commodities up 24.4%, the cease-fire that became a blockade — and the planning moves that matter most coming out of a quarter like this one.

It’s Now More Common To Have A Baby In Your Thirties Than In Your Twenties

DisclosureThis material is for general information only and is not intended to provide specific advice or recommendations for any individual.…

When Does Refinancing Actually Make Sense? A 2026 Reality Check

If you locked in a mortgage at 7% or higher in 2023 or 2024, you’ve probably been watching rates with…