October 2018 – An Economic and Market Update

Executive Summary

- Domestic stock markets and particularly tech stocks have performed well in 2018, but more traditional companies, bonds, and international assets have not kept pace.

- Addressing uncertainty requires time spent identifying how a market downturn or recession will impact your financial plan.

- The Federal Reserve is optimistic for continued strength in the economy although their business contacts are expressing concern about tariffs and the cost of materials.

Looking Back

In the last quarter our current bull market, which officially started on March 9, 2009, surpassed the old record of 3,453 days without a recession. This is a big deal only in so far as it is a marker in an arbitrary timeline. More significant is whether the good times are going to continue. Unfortunately, diverse investors have had spotty returns as interest rate increases have impacted bonds and global growth has stalled so far in 2019i.

F.A.A.N.G. stocks have been a driving force on the S&P 500 this year. Two of these tech companies posted incredible achievements in the last quarter alone. Apple, and then Amazon, became the first publicly traded companies with a market cap over $1,000,000,000,000. This achievement has been concurrent with the struggles of more traditional companies such as General Electric and major auto manufacturers.ii

Source: Bloomberg

As incredible as it is that a public company could be worth $1 trillion dollars, the most significant event of the last quarter is that the United States, Canada, and Mexico came to terms on a new trade deal. This ends, to an extent, a very challenging period for Canadian and US relationsiii. It appears Japan has also recently agreed to open bi-lateral discussions and abandoned an earlier preference for multi-state negotiations only.iv This continues a pattern of traditional allies of the United States engaging with the Trump Administration while attention and pressure on China grow.v

Wisdome From Reserve Chairman Jerome Powell

A common question of the last three months has been some variant on the following: When are we going to have a recession and significant market correction?

The answer to this question is easy as we are all aware that markets are cyclical; we will have a recession and correction sometime in the future. The motivation behind the question is often uncertainty over how a recession and correction will affect an individual’s personal financial circumstances.

We all know that markets go up and down, we just want to experience a little of the down as possible. There was a lot to like in the transcript of Chairman Powell’s Press Conference on September 26th. Our favorite statement, however, summarizes what we believe is the way to approach organizing your finances under perceived higher risks of uncertainty. We have edited his spoken statement for easier reading:vi

“So I think those are the really important lessons, and we’re determined not to forget them. And that’s, I think, a risk now – is to – is to forget things that we learned. That’s just human nature over time.”

The pain of a learning experience subsides over time in addition to our brains developing neural pathways when we do something the wrong way. This phenomenon increases the likelihood of making the same mistake again.vii How aggravating! Now is a great time to intentionally do things different from 2008/09. The following is a list of common ways we can tackle uncertainty and be comfortable with a given level of market exposure.

- Review your current risk tolerance and make sure it is still the same. Your risk tolerance today, 10 years on in a bull market, may be different due to changing priorities and age.

- Review your strategy for access to cash. Is it time to strategically put a line of credit in place?

- Create a Sustainable Income Solution. Future proofing your income is an important step to making your retirement years less stressful.

- Insurance coverage is only as good as your gaps in coverage. There is never a better time to review insurance policies and make sure you have full coverage to meet all your needs.

- Finally, protect against future catastrophic risks, such as Long-Term Care (LTC) needs, when market performance is helping. There are more products to deal with LTC than people realize. It is easier to set aside assets to cover a future need when markets are up versus down.

We do not have a reason to expect a recession is just around the corner. We are, however, receiving a high volume of questions and concerns on which direction the next market move will be. If this is a concern for you lets have a conversation where we discuss the potential risks a recession or major market downturn will have on your planning.

4TH Quarter Volatility and the Federal Reserve

In his public address on September 26th, Chairman Jerome Powell of the Federal Reserve made one of the most optimistic statements we have ever heard out of the Fed.

“Our economy is strong. Growth is running at a healthy clip. Unemployment is low, the number of people working is rising steadily, and wages are up. Inflation is low and stable. All of these are very good signs…Both household spending and business investment are expanding briskly, and the overall growth outlook remains favorable. And several factors support this assessment: Fiscal policy is boosting the economy, ongoing job gains are raising incomes and confidence, and overall financial conditions remain accommodative.”

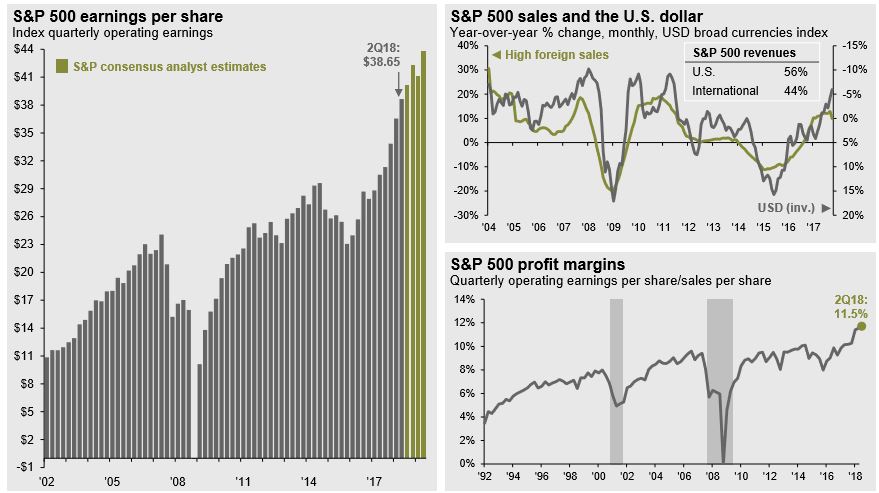

We view current market performance and the statement by the Fed as illustrating two separate points. First, the economy is strong, and things are good. In fact, things are so good the Fed is comfortable with continuing to raise rates and decrease the size of their balance sheet. The Federal Reserve is making public something which you probably already know by looking around. There is a lot of building going on right now. New roofs, parking lot improvements, transportation system expansion, condo, and housing developments; these things are happening all over the place. When you drive around San Diego County you see it. When you travel to other metropolitan areas in the country you see it.

Source: Compustat, FactSet, Standard & Poor’s, J.P. Morgan Asset Management; (Top Right) Federal Reserve

The Federal Reserve’s network of businesses across the country which they track and have regular dialogue with confirming what local observations tell you. This group provides valuable insight to business sentiment. Business is strong, and profits are at all-time highs as you can see in the prior graph. There are still concerns about the effect of tariffs on future investments and profits as we noted in our last Economic Update, but generally speaking, businesses are upbeat.

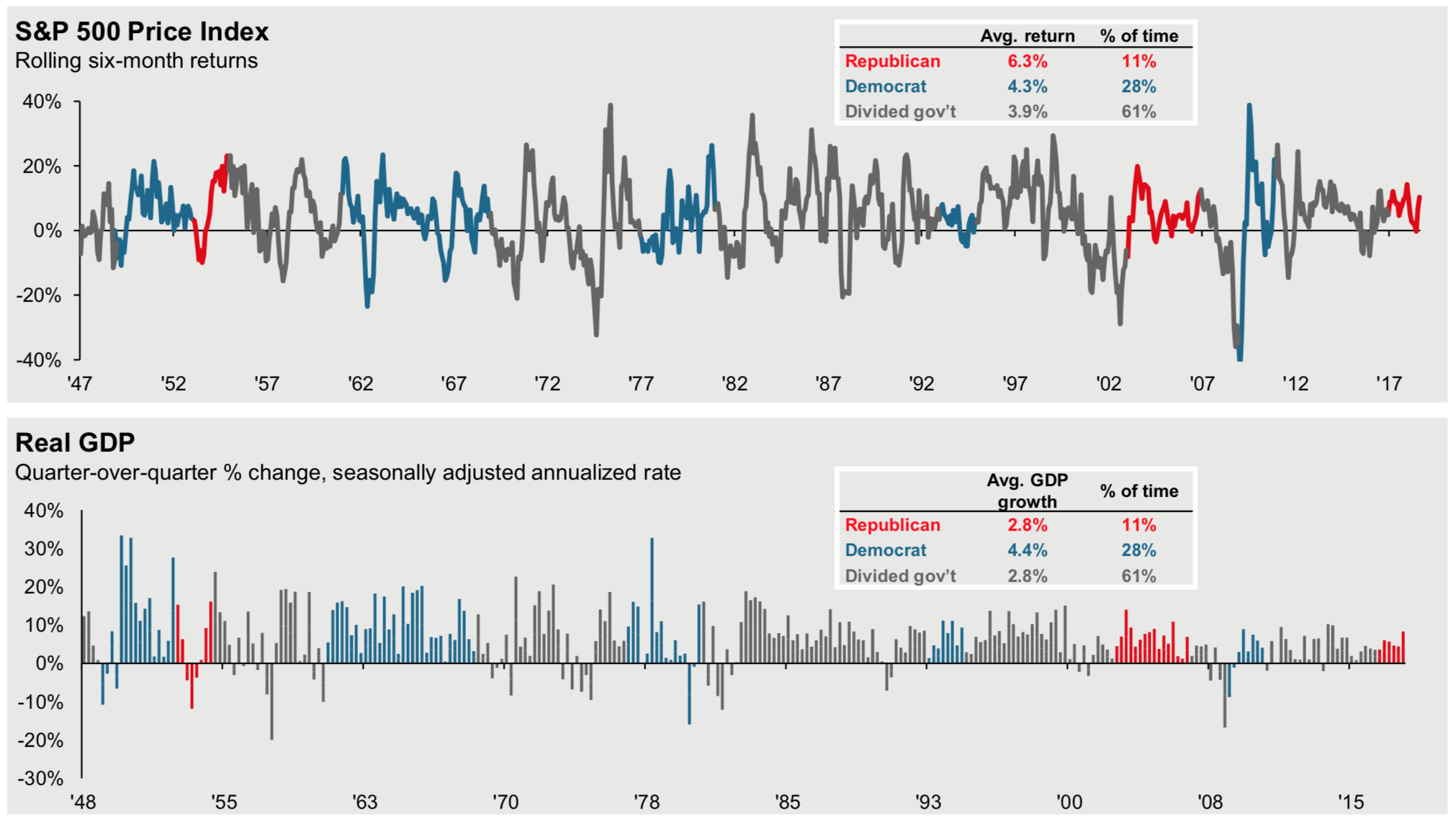

Second, fiscal policy is linked to politics and the party in power. President Trump seems predisposed to focus on stock market performance. Fiscal stimulus in the form of direct spending and tax cuts have boosted growth and profitability which are reflected in market performance. The mid-term elections may prove to be more consequential to stock performance than prior elections because there is the high possibility of a party change causing reversals in policy changing the business paradigm, particularly with taxes. Senator Kamala Harris (D) of California has already proposed a reversal of the Trump tax cuts with increased revenues serving, essentially, as a massive expansion of the Earned Income Tax Credit where qualifying families can receive up to $6,000 per year in additional transfer payments from the government. Market participants generally like stability and this mid-term election is not providing much of that right now.viii

Source: FactSet, Office of the President, J.P. Morgan Asset Management; (Top) Standard & Poor’s; (Bottom) Bureau of Economic Analysis

Guide to the Markets – U.S. Data are as of September 30, 2018

Our recommendation is and has been for months now, to wait out any market volatility through the mid-terms. As the Federal Reserve has indicated, the fundamentals are strong, occasionally we are going to have some turbulence but that does not mean we are not going to make it to our destination. Although it is in very small data sets, markets appear to like Republicans and the economy, as measured by Gross Domestic Product (GDP), tends to favor Democrats based on the graph above. Time will tell where we end up, but for right now the best advice is to cast your vote as your politics dictate but do not let your politics dictate your financial strategy. Good financial planning is performed by making decisions which have ramifications decades into the future, not just up to the next election two years away.

Looking Forward

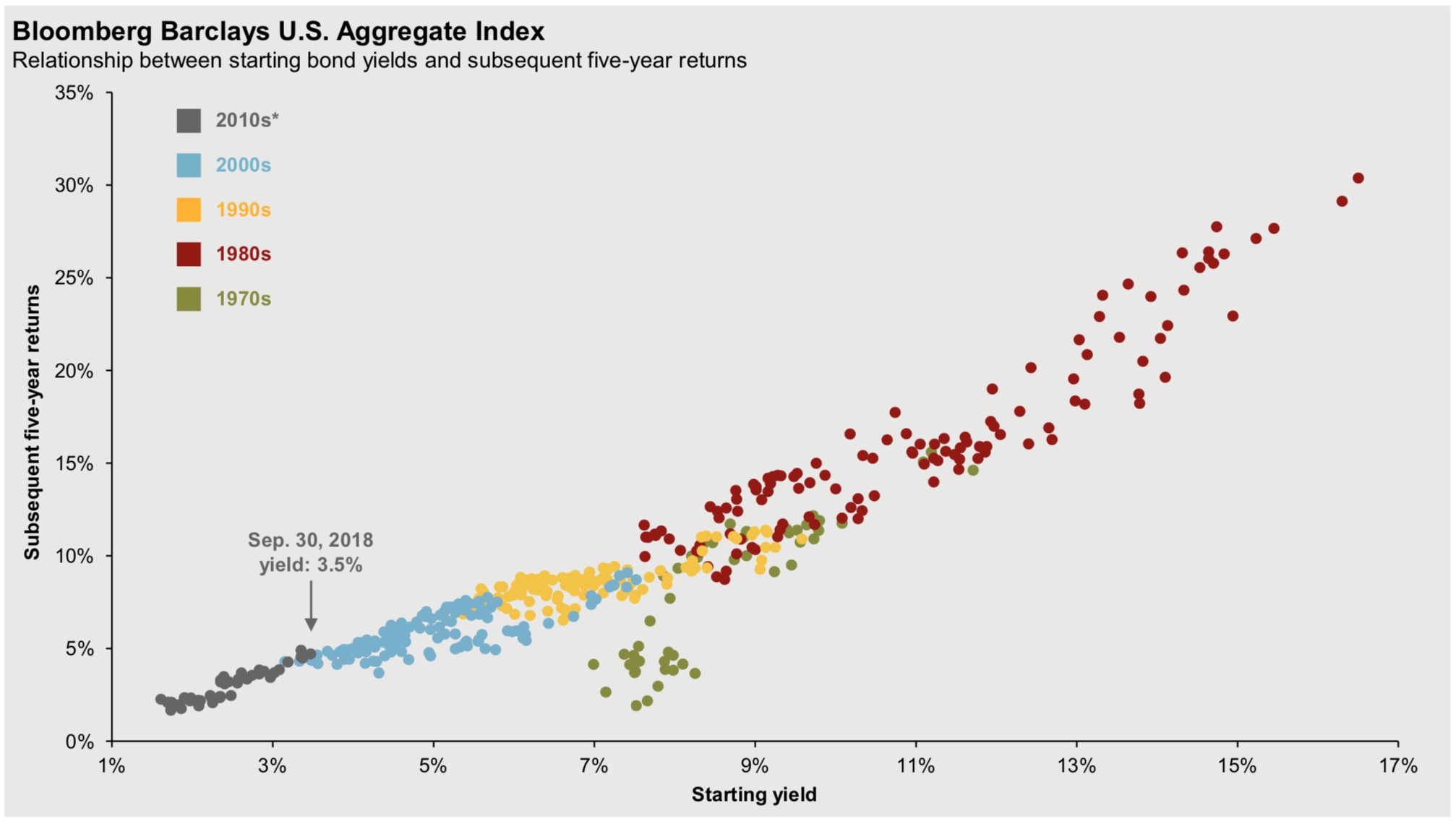

Interest rates are our biggest concern as they represent the largest single holding for so many retirees and near-retirees. The data is not looking great at this particular time and our concern was echoed recently by Charlie Ripley of Allianz Investment Management in the Financial Times, “Higher interest rates typically bring on tighter financial conditions which could dampen growth going forward and equity markets are reacting to that.” ix

Source: Bloomberg Barclays, FactSet, J.P. Morgan Asset Management. *2010’s are from January 2010 to September 2013. R2 for bond yields and subsequent five-year returns is 86%. Past performance is not indicative of comparable future results. Guide to the Markets – U.S. Data are as of Sept. 30, 2018

We are in uncharted territory coming out of the low-interest-rate environment of the last decade without the benefit of prior history to make us feel better. The data suggests we should temper our forward-looking return expectations. This is something we are monitoring and our goal is to minimize the impact of interest rate risk on your portfolios.

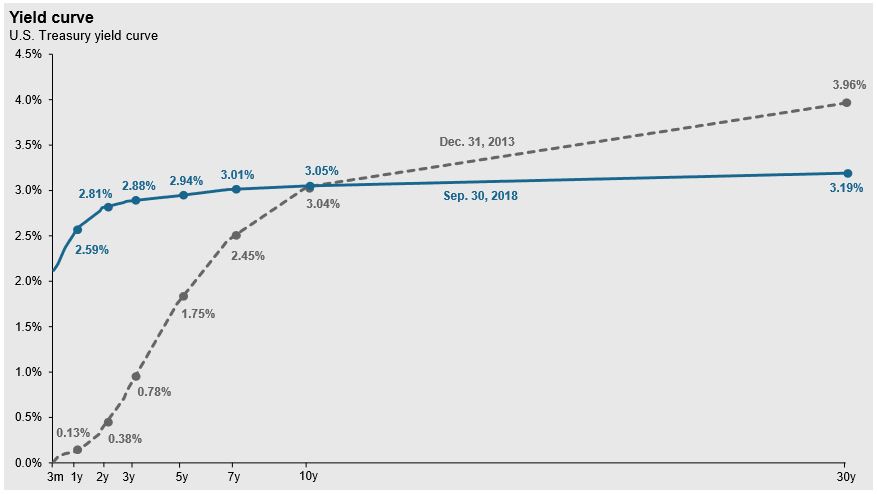

As an update to our 3rd Quarter Economic Update, the yield curve has continued to flatten. The gap between short-term and long-term bonds has narrowed from 70 basis points last quarter to 60 basis points. A basis point is equivalent to 1/100th of a percent. An inverting yield curve, short-term rates higher than long-term rates, is a strong indicator of a recession. A flat yield curve tells us that short-term risks are viewed on par with long-term risks contrary to the idea that investors should be paid for the higher risk associated with tying money up for an extended duration. A more normal spread between short and long-term bonds is illustrated in the dotted line below from 2013.

Source: FactSet, Federal Reserve, J.P. Morgan Asset Management

Guide to the Markets – U.S. Data are as of September 30, 2018

We are here to help you make rational, informed and well-reasoned decisions. We thank you for your continued trust and support. Your input is always welcome, and we ask that you contact us with any questions or concerns.

Disclosure

All information is believed to be from reliable sources; however, we make no representation as to its completeness or accuracy. All economic and performance data is historical and not indicative of future results. Market indices discussed are unmanaged. Investors cannot invest in unmanaged indices. Additional risks are associated with international investing, such as currency fluctuations, political and economic instability and differences in accounting standards.

Investing in securities in emerging markets involves special risks due to specific factors such as increased volatility, currency fluctuations and differences in auditing and other financial standards. Securities in emerging markets are volatile and can decline significantly in response to adverse issuer, political, regulatory, market, or economic developments.

An index is a statistical measure of change in an economy or a securities market. In the case of financial markets, an index is an imaginary portfolio of securities representing a particular market or a portion of it. Each index has its own calculation methodology and is usually expressed in terms of a change from a base value. Thus, the percentage change is more important than the actual numeric value. An investment cannot be made directly into an index.

Investing in fixed income securities involves credit and interest rate risk. When interest rates rise, bond prices generally fall. Investing in commodities may involve greater volatility and is not suitable for all investors. Investing in a non-diversified fund that concentrates holdings into fewer securities or industries involves greater risk than investing in a more diversified fund. The equity securities of small companies may not be traded as often as equity securities of large companies so they may be difficult or impossible to sell. Neither diversification nor asset allocation assure a profit or protect against a loss in declining markets. Past performance is not an indicator of future results.

Securities offered through 1st Global Capital Corp., Member FINRA and SIPC. Steven W. Pollock, Sean P. Storck, Matthew J. Anderson, and Nicole Albrecht are Registered Representatives of 1st Global Capital Corp. Investment advisory services, including RBFI portfolios offered through Reason Financial. IMS platform accounts offered through 1st Global Advisors, Inc. Reason Financial. and 1st Global Capital Corp. is unaffiliated entities. Reason Financial is a Registered Investment Adviser. Placing business through 1st Global Insurance Services. Registration does not imply a certain level of skill or training. We currently have individuals licensed to offer securities in the states of Arizona, California, Illinois, Indiana, Kansas, Massachusetts, Michigan, New York, Oregon, and Washington. This is not an offer to sell securities in any other state or jurisdiction. CA Department of Insurance License: Steven W. Pollock #OE98073, Sean P. Storck #0F25995, Matthew J. Anderson #0F21959 and Nicole Albrecht #0F99962.

ENDNOTES

1 Kim, Tae. “3,453 Days Later, the US Bull Market Becomes the Longest on Record.” CNBC, CNBC, 22 Aug. 2018, www.cnbc.com/2018/08/22/longest-bull-market-since-world-war-ii-likely-to-go-on-because-us-is-best-game-in-town.html.

2 Gurman, Mark. “Apple Becomes First U.S. Company to Hit $1 Trillion Value.” Bloomberg.com, Bloomberg, 2 Aug. 2018, www.bloomberg.com/news/articles/2018-08-02/apple-becomes-first-u-s-company-to-hit-1-trillion-market-value.

3 “US and Canada Reach New Trade Deal to Replace Nafta.” BBC News, BBC, 1 Oct. 2018, www.bbc.com/news/business-45702609.

4 Rich, Motoko. “Japan Caved to Trump on Trade Talks. Now the Real Haggling Begins.” The New York Times, The New York Times, 19 Oct. 2018, www.nytimes.com/2018/10/19/world/asia/trump-japan-trade.html.

5 Tankersley, Jim, and Keith Bradsher. “Trump Hits China With Tariffs on $200 Billion in Goods, Escalating Trade War.” The New York Times, The New York Times, 17 Sept. 2018, www.nytimes.com/2018/09/17/us/politics/trump-china-tariffs-trade.html.

6 Jerome Powell’s September 26, 2018, Press Conference …These comments are excerpted from the “Transcript of Chairman Powell’s Press Conference“ (preliminary)(pdf) of September 26, 2018, with the accompanying “FOMC Statement” and “Economic Projections of Federal Reserve Board Members and Federal Reserve Bank Presidents, September 2018“ (pdf).

7 Khazan, Olga. “Why We Often Repeat the Same Mistakes.” The Atlantic, Atlantic Media Company, 28 Feb. 2016, www.theatlantic.com/science/archive/2016/02/why-mistakes-are-often-repeated/470778/.

8 Weissmann, Jordan. “Kamala Harris Wants to Give Middle-Class Families $500 Every Month. Her Plan Is Bold, Generous, and Maybe Ill-Conceived.” Slate Magazine, Slate, 22 Oct. 2018, slate.com/business/2018/10/kamala-harris-middle-class-tax-plan.html.

9 Wigglesworth, Robin. “What Is behind the Global Stock Market Sell-off?” Financial Times, Financial Times, 11 Oct. 2018, www.ft.com/content/af34550e-cd01-11e8-b276-b9069bde0956.

Disclosure

This material is for general information only and is not intended to provide specific advice or recommendations for any individual. There is no assurance the views or strategies discussed are suitable for all investors or will yield positive outcomes. Investing involves risks including possible loss of principal. Any company names noted herein are for educational purposes only.

All information is believed to be from reliable sources; however we make no representation as to its completeness or accuracy. All economic and performance data is historical and not indicative of future results. Market indices discussed are unmanaged. Investors cannot invest in unmanaged indices. Additional risks are associated with international investing, such as currency fluctuations, political and economic instability and differences in accounting standards.

Investing in securities in emerging markets involves special risks due to specific factors such as increased volatility, currency fluctuations and differences in auditing and other financial standards. Securities in emerging markets are volatile and can decline significantly in response to adverse issuer, political, regulatory, market, or economic developments.

An index is a statistical measure of change in an economy or a securities market. In the case of financial markets, an index is an imaginary portfolio of securities representing a particular market or a portion of it. Each index has its own calculation methodology and is usually expressed in terms of a change from a base value. Thus, the percentage change is more important than the actual numeric value. An investment cannot be made directly into an index.

Investing in fixed income securities involves credit and interest rate risk. When interest rates rise, bond prices generally fall. Investing in commodities may involve greater volatility and is not suitable for all investors. Investing in a non-diversified fund that concentrates holdings into fewer securities or industries involves greater risk than investing in a more diversified fund. The equity securities of small companies may not be traded as often as equity securities of large companies so they may be difficult or impossible to sell. Neither diversification nor asset allocation assure a profit or protect against a loss in declining markets. Past performance is not an indicator of future results.

Financial Planning offered through Reason Financial, a state Registered Investment Advisor. Investment advice offered through Merit Financial Group, LLC an SEC Registered Investment Advisor. Merit Financial Group and Reason Financial are separate entities. Tax related services offered through Reason Tax Group. Reason Tax Group is a separate legal entity and not affiliated with Merit Financial Group, LLC. Sean P. Storck CA Insurance Lic#OF25995 and Steven W. Pollock CA Insurance Lic#OE98073

Copyright © 2026 Reason Financial all rights reserved.

Continue Reading

2nd Quarter 2026 – Economic and Market Update

Q1 2026 in review: oil shock, S&P 500 down 4.3%, commodities up 24.4%, the cease-fire that became a blockade — and the planning moves that matter most coming out of a quarter like this one.

It’s Now More Common To Have A Baby In Your Thirties Than In Your Twenties

DisclosureThis material is for general information only and is not intended to provide specific advice or recommendations for any individual.…

When Does Refinancing Actually Make Sense? A 2026 Reality Check

If you locked in a mortgage at 7% or higher in 2023 or 2024, you’ve probably been watching rates with…