Three considerations to make before turning on Social Security

Three Consideration to make before turning on Social Security

Planning Intelligence by Steve Pollock

![]()

Retirement planning is financial planning intelligence at its highest level. It requires the balance of understanding your unique vision of retirement, making rational assumptions about the future, and applying analytics to make informed decisions.

During this process one of the most frequent questions we face, usually just after “Can I retire?”, revolves around claiming Social Security benefits at the most opportune time.

Here are the three primary factors we take into consideration when determining the best strategy for a client to maximize their social security benefit.

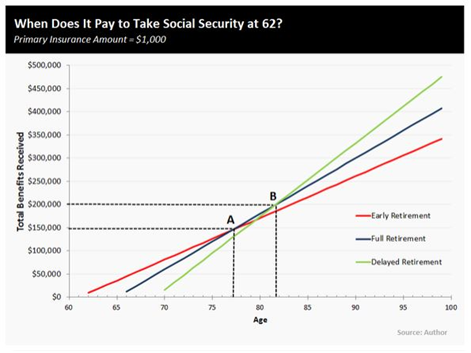

1. Identify your Social Security Break-Even Age.

We recognize that our time is limited and need to consider how long we reasonably anticipate being alive. The less morbid way to approach life expectancy is as a statistical number. According to data compiled by the Social Security Administration, a 65-year-old male can expect to live on average until age 84.3. An average woman turning age 65 can expect to live to age 86.6. However, averages only take us so far and the data points out that 25% of those age 65 today will live past the age of 90. 1

In reality, life expectancy is unique to every individual and their set of circumstances. A simple search of Web M.D. provides numerous publications for what enhances and detracts from one’s life expectancy. We therefore need to take into consideration your unique circumstances, mainly focused on your overall health and family history. This allows you to make an educated assumption to how long you think you may live.

Armed with your life expectancy assumption we can identify the break-even point to compare claiming your benefit at age 62, full retirement age, or age 70.

A basic break-even analysis can help illustrate your optimal filing age based on your life expectancy. From figure 1 below, point “A” shows that if you were to live past age 77, then waiting to claim your benefit until age 66 would begin to be more advantageous. If you project your life expectancy past age 82, then you would have the greatest lifetime benefit by waiting until age 70 to claim your social security benefit.

Source: Social Security: Why Taking Benefits at 62 Is Smarter Than You Think, John Maxfield, May 2014

From a very quantitative standpoint and using the average mortality tables, our Social Security analysis always leans toward waiting until age 70 to claim your Social Security Benefit.

2. Marital status and planning for the Survivor Benefit.

Your marital status complicates the Social Security equation. We now take into consideration both partners’ life expectancy along with their available survivor’s benefit. The survivor’s benefit is an important consideration and it provides the surviving spouse with the greater of the couple’s social security benefits at the passing of their spouse.

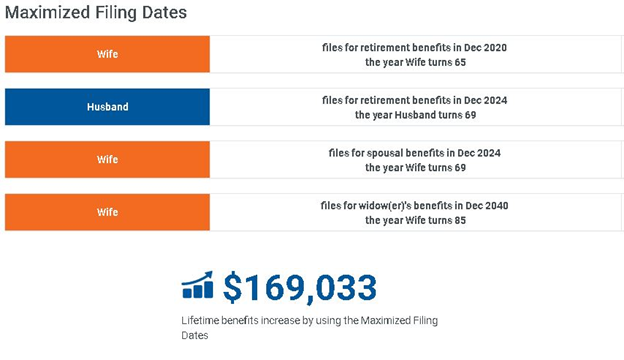

The following married couple’s set of circumstances helps illustrates that its not always about life expectancy as shown above.

Example: Same Age, Different Life Expectancy and SS Benefit

Husband Age: 62

Husband SS Benefit: $2,500/month

Life Expectancy: 85

Wife Age: 62

Wife Social SS Benefit $1,500/month

Life Expectancy: 95

In the example above the husband and wife are the same age; the husband has a higher benefit and average life expectancy. The analysis shows the family will have received a $169,000 greater benefit over their joint lifetime if the Wife begins to claim benefits at full retirement age and switches to their survivor benefit at the passing of her spouse.

This example shows the nuances of planning for a married couple’s social security benefit. The analysis disagreed with our longevity break-even data and suggests one spouse turn on social security before age 70.

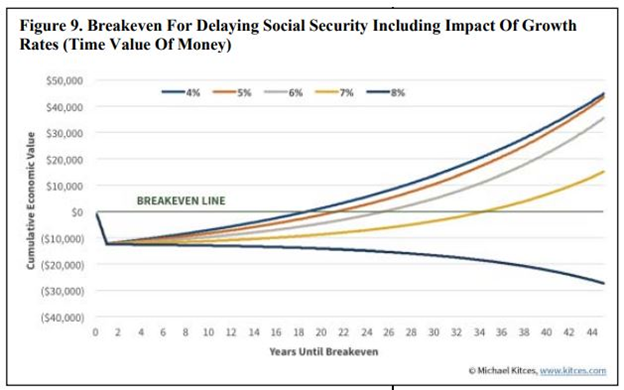

3. Time value of money and entitlement risk.

Our third consideration is the most compelling reason why many do not wait until age 70 to claim social security. There is economic benefit in not having to supplement your retirement with your own assets early in retirement. The economic benefit, coupled with an unknown state of the Social Security System, provide a well-reasoned contrary to our first consideration and the break-even analysis.

Time Value of Money

We take our break-even analysis one step further when considering the time value of money. When you collect Social Security early and therefore reduce your need of withdrawing money from your investments, the money you keep invested continues to grow. The impact of growth on the assets has the potential to stretch the break-even age further and is dependent on the growth rate you experience on your investments.

Provided in the figure below is an example of how different growth rates impact the years until you break even. For instance, if you claimed social security at age 62 and allow your invested dollars to continue to grow at a 6% rate of return each year, you would have stretched the break-even point from 13.5 years to almost 25 years.

Source: Kitces, Michael. The Kitces Report Volume 1, 2016, “The New World of Social Security Planning”

Entitlement Risk

Deferring your Social Security benefit for as long as possible creates a heightened entitlement risk. Entitlement risk is the risk that a social program which you have paid into for the duration of your career will not deliver expected or promised benefits.

It is no secret that Social Security projections show that it is grossly underfunded. Projections provided by the Treasury Department continue to indicate that the Social Security fund will be depleted by 2035. While some recent legislation has been enacted to reduce abuse to the Social Security System, it will require more attention. 2,3

Claiming your benefit early reduces the risk related to the unknown state of the Social Security System and how it could impact your future benefit.

Your Reason

The timing of when to claim Social Security is different for everyone. Reason Financial is your team of highly specialized professionals in retirement planning to help you navigate and plan the best strategy for you.

Enabling you and your family to make a lifetime of rational, informed and well-reasoned financial decisions gives us purpose in what we do. Thank you for your continued trust.

Your Truly,

Endnotes

1. Social Security Administration. “Calculators: Life Expectancy” https://www.ssa.gov/planners/lifeexpectancy.html

2. Ted Knutson. “Social Security, Medicare Trust Funds Get Extra Year Of Breathing Room.” http://www.fa-mag.com/news/social-security–medicare-trust-funds-get-extra-year-of-breathing-room-33690.html?utm_content=buffer215c5&utm_medium=social&utm_source=twitter.com&utm_campaign=buffer

3. Social Security Administration. “Retirement Planner: Recent Social Security Claiming Changes.” https://www.ssa.gov/planners/retire/claiming.html

Disclosure

This material is for general information only and is not intended to provide specific advice or recommendations for any individual. There is no assurance the views or strategies discussed are suitable for all investors or will yield positive outcomes. Investing involves risks including possible loss of principal. Any company names noted herein are for educational purposes only.

All information is believed to be from reliable sources; however we make no representation as to its completeness or accuracy. All economic and performance data is historical and not indicative of future results. Market indices discussed are unmanaged. Investors cannot invest in unmanaged indices. Additional risks are associated with international investing, such as currency fluctuations, political and economic instability and differences in accounting standards.

Investing in securities in emerging markets involves special risks due to specific factors such as increased volatility, currency fluctuations and differences in auditing and other financial standards. Securities in emerging markets are volatile and can decline significantly in response to adverse issuer, political, regulatory, market, or economic developments.

An index is a statistical measure of change in an economy or a securities market. In the case of financial markets, an index is an imaginary portfolio of securities representing a particular market or a portion of it. Each index has its own calculation methodology and is usually expressed in terms of a change from a base value. Thus, the percentage change is more important than the actual numeric value. An investment cannot be made directly into an index.

Investing in fixed income securities involves credit and interest rate risk. When interest rates rise, bond prices generally fall. Investing in commodities may involve greater volatility and is not suitable for all investors. Investing in a non-diversified fund that concentrates holdings into fewer securities or industries involves greater risk than investing in a more diversified fund. The equity securities of small companies may not be traded as often as equity securities of large companies so they may be difficult or impossible to sell. Neither diversification nor asset allocation assure a profit or protect against a loss in declining markets. Past performance is not an indicator of future results.

Financial Planning offered through Reason Financial, a state Registered Investment Advisor. Investment advice offered through Merit Financial Group, LLC an SEC Registered Investment Advisor. Merit Financial Group and Reason Financial are separate entities. Tax related services offered through Reason Tax Group. Reason Tax Group is a separate legal entity and not affiliated with Merit Financial Group, LLC. Sean P. Storck CA Insurance Lic#OF25995 and Steven W. Pollock CA Insurance Lic#OE98073

Copyright © 2026 Reason Financial all rights reserved.

Continue Reading

2nd Quarter 2026 – Economic and Market Update

Q1 2026 in review: oil shock, S&P 500 down 4.3%, commodities up 24.4%, the cease-fire that became a blockade — and the planning moves that matter most coming out of a quarter like this one.

It’s Now More Common To Have A Baby In Your Thirties Than In Your Twenties

DisclosureThis material is for general information only and is not intended to provide specific advice or recommendations for any individual.…

When Does Refinancing Actually Make Sense? A 2026 Reality Check

If you locked in a mortgage at 7% or higher in 2023 or 2024, you’ve probably been watching rates with…