What is a fiduciary?

If you’re getting financial advice, fiduciary is one of the most important words for you to know… but it may not be as important as the word trust. By the end of this article, we hope you understand why.

At Reason Financial we’re held to the fiduciary standard on multiple levels. That means we look out for your best interests, not ours. More specifically:

A fiduciary has a legal responsibility to put your financial well-being ahead of their own.

Why is this important?

A number of financial products — let’s say a variable annuity — are packaged and marketed just like anything else. The firms who design these products offer financial professionals commissions if they sell the products to their clients.

Often, advisors market this as a good deal for clients: Because the advisor is paid by the firm making the product, clients may not be asked to pay that advisor a fee. This can sound great on the surface: No fee means free financial advice, right? Wrong.

As you might expect, there is no free lunch. The products aren’t always the best deal for clients. They might have lower returns than competing products, higher fees, or they might not match the client’s goals or risk tolerance.

A fiduciary, on the other hand, is legally obligated to recommend the best product for you, regardless of compensation. Some advisors take it a step further and refuse any product commissions, choosing to work on a fee-only basis.

Fiduciaries and fees

While we work primarily on a fee-only basis at Reason Financial, we don’t always. While we always choose the solution we believe is in your best interest, sometimes it works out to be a better deal if we use transaction- or commission-based pricing, versus a fee-only model.

We believe the key, when it comes to compensation, is transparency. Most of the current skepticism around commissions-based pricing started during the financial crisis, when advisors recommended faulty products in order to pocket the commissions.

But if your advisor is interested in what’s best for you, he or she probably wouldn’t recommend those types of products anyway, regardless of the payment structure. Plus, fee-only advisors can offer bad advice, too. Which is why we try to emphasize transparency and trust, not fee structure, when we talk about financial advice.

How can you tell if your advisor is held to a fiduciary standard?

To figure out if your advisor is legally obligated to act in your best interests, the easiest way is often to ask. You may also be able to tell based on their credentials. Here are some common designations and the standards they are held to:

Certified Financial Planners® (CFPs) are bound to a fiduciary standard by the CFP Board of Standards. The board insists CFPs act in their clients’ best interests on a wide variety of advice, beyond just investments. At Your Reason, Sean and Steve are both CFPs. That means we act as fiduciaries regardless of what products we’re talking about with our clients.

For example, while tax and insurance professionals aren’t typically fiduciaries, when we talk about tax planning or insurance products, we’re acting as CFPs, so we’re still bound by this fiduciary standard.

Registered investment advisor (RIA) firms are registered with the Securities and Exchange Commission (SEC) and are legally required to put client needs ahead of their own. For an advisor to register a firm, they must pass a specific test (known as a Series 65) demonstrating their knowledge of financial and investment products, as well as ethics and fiduciary responsibility.

Registered representative of a broker-dealer — or anyone selling you an investment via a broker-dealer affiliation — is not required to be a fiduciary by regulators. Instead, they’re held to a standard known asregulation best interest. Whatever product they recommend to you must be in your best interest at the time of the recommendation, but conflicts of interest are allowed, so long as they are disclosed.

Some firms work as a hybrid between an RIA and a broker-dealer, which is how Reason Financial operates. The broker-dealer affiliation allows us to serve clients more efficiently when there are more transactional requests.

However, we’re still required to act as a fiduciary based on our CPF status, even on brokered transactions. We will always put your needs first. This is about more than regulations for us; it’s a mindset. We believe this job requires a certain amount of innate goodness. (We even made innate goodness one of our values as a company.)

And that’s why we started this article saying that while fiduciary is one of the most important words in financial advice, it’s not as important as the word trust. We build trust through transparency and education. Which is why we wanted to walk you through the different designations and affiliations we hold, and what they mean.

If you have any questions about what’s included in this article, how it applies to our operating model, or what it means for the advice offer, just ask. We’re happy to answer questions and promise transparent answers.

Content in this material is for general information only and not intended to provide specific advice or recommendations for any individual.

Disclosure

This material is for general information only and is not intended to provide specific advice or recommendations for any individual. There is no assurance the views or strategies discussed are suitable for all investors or will yield positive outcomes. Investing involves risks including possible loss of principal. Any company names noted herein are for educational purposes only.

All information is believed to be from reliable sources; however we make no representation as to its completeness or accuracy. All economic and performance data is historical and not indicative of future results. Market indices discussed are unmanaged. Investors cannot invest in unmanaged indices. Additional risks are associated with international investing, such as currency fluctuations, political and economic instability and differences in accounting standards.

Investing in securities in emerging markets involves special risks due to specific factors such as increased volatility, currency fluctuations and differences in auditing and other financial standards. Securities in emerging markets are volatile and can decline significantly in response to adverse issuer, political, regulatory, market, or economic developments.

An index is a statistical measure of change in an economy or a securities market. In the case of financial markets, an index is an imaginary portfolio of securities representing a particular market or a portion of it. Each index has its own calculation methodology and is usually expressed in terms of a change from a base value. Thus, the percentage change is more important than the actual numeric value. An investment cannot be made directly into an index.

Investing in fixed income securities involves credit and interest rate risk. When interest rates rise, bond prices generally fall. Investing in commodities may involve greater volatility and is not suitable for all investors. Investing in a non-diversified fund that concentrates holdings into fewer securities or industries involves greater risk than investing in a more diversified fund. The equity securities of small companies may not be traded as often as equity securities of large companies so they may be difficult or impossible to sell. Neither diversification nor asset allocation assure a profit or protect against a loss in declining markets. Past performance is not an indicator of future results.

Financial Planning offered through Reason Financial, a state Registered Investment Advisor. Investment advice offered through Merit Financial Group, LLC an SEC Registered Investment Advisor. Merit Financial Group and Reason Financial are separate entities. Tax related services offered through Reason Tax Group. Reason Tax Group is a separate legal entity and not affiliated with Merit Financial Group, LLC. Sean P. Storck CA Insurance Lic#OF25995 and Steven W. Pollock CA Insurance Lic#OE98073

Copyright © 2026 Reason Financial all rights reserved.

Continue Reading

3rd Quarter 2026 – Economic and Market Update

Q2 2026 in review: the S&P 500’s best quarter since 2020, oil’s round trip from $114 back to $70, a 4.2% CPI print that would not quit, and a new Fed chair who took 2026 rate cuts off the table — plus what a 15% quarter means for the allocation you actually own.

America at 250: A Birthday Worth Sitting With for a Moment

The United States just turned 250 — and the story reads surprisingly well as a series of 50-year check-ins. Founding-era population the size of San Diego County, two presidents with impeccable dramatic timing, a telephone demo in Philadelphia, quarters you’re still finding in your change — and one compounding machine that started counting in 1926.

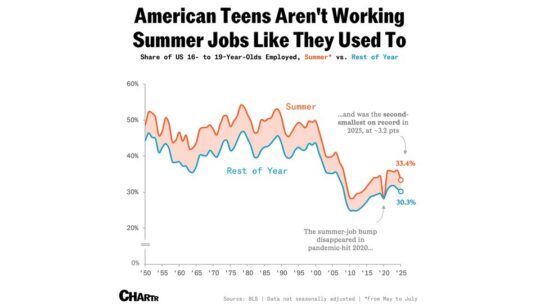

American Teens Aren’t Working Summer Jobs Like They Used To

DisclosureThis material is for general information only and is not intended to provide specific advice or recommendations for any individual.…