October 2022 – Economic and Market Update

EXECUTIVE SUMMARY

- A strong dollar is making foreign travel cheap and exports expensive. This will likely continue to weaken our economy by exacerbating the current trade deficit.

- Housing is expensive and the real estate market is slowing down.

- Our current investment thesis is a focus on domestic value equities and high quality short-duration fixed income

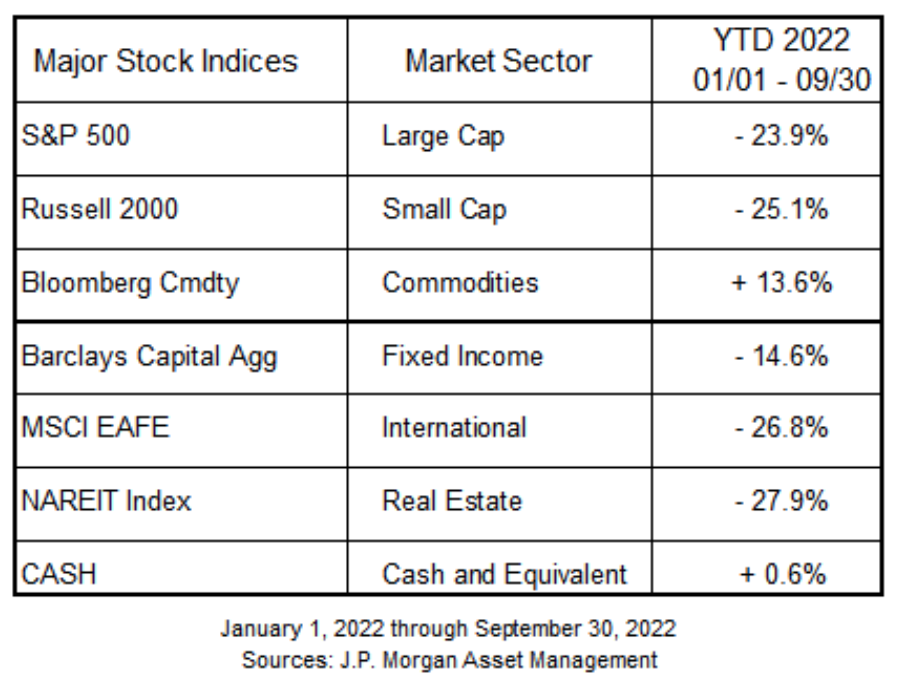

We are in a cycle of lower lows. Bear market buyers are not being rewarded and sticking to the strategy is painful. The only positive performer year to date are commodities. However, all of their gains were made in the early part of the year with significant downturns occurring since early summer. High quality bonds have had an awful year as interest rate increases have hammered the fixed income space. Long-term inflation expectations have continued to rise indicating a turn towards taking the Federal Reserve at their word in continuing aggressive interest rate hikes. We believe that much of the pain has been felt in domestic markets, however, calling a bottom is a fool’s errand.

THE STRONG DOLLAR

From a financial perspective, it is a great time to take a trip overseas. The dollar, on an inflation adjusted basis, is stronger than it has been since the early 80’s. The British Pound is as cheap to buy with dollars as you could ever want. The exchange rate is a drag, however, on economic productivity. As the dollar strengthens, U.S. exports get more expensive and our trade imbalance increases. This should further exacerbate the economic slowdown in the U.S. as cheaper alternatives to our goods are sought in other countries. To the extent that demand for U.S. goods and services are inelastic, this will cause inflation in other countries, undermining global economic conditions.i

Our top exports are petroleum/petroleum products, cars/auto-parts, integrated circuits, food/feed, and services. All told the US exports of goods and services are $2.5 trillion dollars as of 2021. Roughly 10% of our GDP is becoming more expensive to buy as the dollar marches upwards. Federal Reserve policy to combat inflation by raising interest rates makes it more expensive to borrow and consume in the U.S. But it also makes it more expensive to buy U.S. exports in other countries. This trend does not appear to be slowing down with the Federal Reserve being the most aggressive central bank in terms of stamping down inflation. This will undercut our economy as alternatives to our exports make financial sense. Falling exports will be one more punch to the gut of a slowing economy.ii

INTEREST RATES

Cash is king and holding it is becoming more attractive from a return standpoint. In a mostly cashless society, particularly post-pandemic, this maxim seems lost on recent generations. In a discussion with a young person they seemed confused by the phrase and responded with a rather snooty, “I’m only 21”. It was a good reminder of age in action, although a bit sad that such a helfpul financial maxim is not known to the younger crowd. For some context, the conversation took place at a trendy cookie shop where they only take credit. Interest rate increases are making cash equivalent holdings, such as brokerage CDs, more attractive in the short-to-intermediate term ranging from 9 months to 2 years.

As you can see above, we have an inverted yield curve and there is not much gain found in the longer term. Short-to-intermediate term treasuries and brokerage CDs operate differently relative to the standard bank CD, but the rates are better. If you have cash this is a great way to obtain a higher yield than the standard bank is offering as we are seeing rates about a full percentage point higher for similar duration. We are happy to discuss the differences as it is important to understand them before purchasing.iii

The downside of higher rates is the cost of borrowing. Average mortgage rates are now around 6.7%, up from 3.25% less than 2 years ago. This is making the acquisition of real estate harder, particularly in San Diego where the median home price is about $900,000. The mortgage payment associated with the purchase of a $900,000 home with 20% down in 2020 is now equivalent to the purchase of a $600,000 home with 20% down today. We are over-simplifying this for illustrative purposes and not taking into account the size of down-payment, etc.iv

Real estate prices are moderating across the United States, particularly in those areas which experienced the highest growth, such as Boise, ID. The rosy prediction of transitory inflation and a return to ultra-low rates is not coming to fruition. This matters because if a new buyer thought they could refinance in a year to a cheaper payment, they might be willing to continue propping up high prices. The higher long-term inflation expectations rise, the less likely it will be to refinance quickly. Affordability then becomes more of an issue and will be reflected in the prices buyers are willing to pay.v

Real estate prices are looking like they are in for a downturn with high mortgage rates and declining demand.

CURRENT CONVICTIONS

The U.S. is ahead of the curve when it comes to tightening monetary policy and working at getting ahead of inflation. There is a lot of arm-chair quarterbacking that can be done on this topic, but the Federal Reserve is out in front of other central banks even if they are late to the game. From our perspective, this provides the U.S. several advantages not afforded to the rest of the world. For this reason we have allocated less to International Equities relative to our normal market allocation.

International equities appear to be a value at this time as evidenced in the graph above. Appearing cheap does not make them cheap. The state of being “undervalued” could be an instance of the market mispricing growth potential. It could also be that markets are driving down the price to where future earnings will indicate what the price should be. With the economic and geopolitical risks facing international equities at this time we are allocating assets elsewhere.

Global slowdowns have a historical habit of not making much of a splash when they hit our shores. Part of this is, believe it or not, a lack of connectedness to the rest of the world. Our GDP is made up of several components, the largest of which is personal consumption making up 70% of our GDP. For comparison, Germany (51.9%), France (53%), Japan (56%), China (38.5%), all have significantly lower levels of internal GDP generation. With the various challenges manifesting globally, countries reliant on interconnectedness with the rest of the world will likely suffer economically.vi

We are also choosing to limit exposure to China. This is a pragmatic investment strategy more than anything else. First, China has continued in their zero-Covid strategy. Every time they take tens of millions of people out of the mix via strict lockdowns, the economy will suffer. The slowdown in Chinese growth is evident in the most recent quarter GDP measurement in the graph above; the far right column.

Second, China is not that cheap anymore. They have done an incredible job taking hundreds of millions of people out of poverty into what is their version of a middle-class. This will have impacts on how non-Chinese companies choose to use their labor force and supply-chain. There are cheaper labor

alternatives, even in a world where globalization appears to be waning. On the political side, President Biden has continued President Trump’s tariffs. Business with China is not business as usual.The process of industrialization that took other countries a hundred years or more, China has squeezed into a couple generations.vii

If we are underweight international equities, that means we are overweight domestic equities. We are taking a diverse approach to U.S. equity with an emphasis on value/blend companies and away from growth. Higher interest rates serve as a continued hindrance for growth-oriented companies. We have moved more value-centric over the last year and will continue to hold that posture for the foreseeable future. As the quote below suggests, don’t expect a slackening in interest rate increases anytime soon.

“If we don’t see progress in underlying inflation or core inflation, I don’t see why I would advocate stopping at 4.5%, or 4.75% on something like that. We need to see actual progress in core inflation and services inflation and we are not seeing it yet.” Neel Kashkari, President Minneapolis Fed, 10/19/2022viii

Higher inflation and higher interest rates for longer are a very relevant risk. We believe risks are high enough for us to continue the trend we started in late 2021 towards shorter-duration fixed income investments. Whether we return to pre-Covid dynamics or not, we believe risk is high enough that remaining short-duration in fixed income is necessary.

THE PLANNING CORNER

SECURE ACT 2.0 has not passed yet and we are running out of time. It looked like Congress would manage to get their act together and pass the second version of the SECURE Act, but alas, it has not happened. If you are turning 72 prior to April 2023, now is the time to address your first RMD (Required Minimum Distribution). We should work together to put in place the plans necessary to ensure the distribution occurs if the law does not pass by December 21, 2022. This includes a look at the tax ramifications of the distribution being taken in 2022 or doubled up in 2023.

Roth conversions are best done when markets are down. We have said this before and we will keep saying it during market drawdowns. Roth conversions in down markets can reduce the tax burden of said conversion while amplifying the value over time when markets return to growth mode. Here is a simple way to think about it: a conversion of $100,000 at the market peak would be about $75,000 to $85,000

in a conversion today depending on your asset allocation strategy. A recovery to $100,000 post-conversion would represent tax free growth of the difference.

Traditional IRA account owners have considerations to make before performing a Roth IRA conversion. These primarily include income tax consequences on the converted amount in the year of conversion, withdrawal limitations from a Roth IRA, and income limitations for future contributions to a Roth IRA. In addition if you are required to take a required minimum distribution (RMD) in the year you convert, you must do so before converting to a Roth IRA.

Take advantage of higher rates by researching your options. Cash equivalents are not all the same. A bank CD paying 3.25% over 12 months is going to fall 1%, or more, short of the yield possible in other FDIC insured options. It is important to understand the differences. Please let us know if you would like to discuss other options for your cash.

As always, our desire is to help you make rational, informed and well-reasoned decisions, and we thank you for your continued trust and support. Your input is always welcome and we ask that you contact us with any questions or concerns.

DISCLOSURE

All information is believed to be from reliable sources; however we make no representation as to its completeness or accuracy. All economic and performance data is historical and not indicative of future results. Market indices discussed are unmanaged. Investors cannot invest in unmanaged indices. Additional risks are associated with international investing, such as currency fluctuations, political and economic instability and differences in accounting standards.

Investing in securities in emerging markets involves special risks due to specific factors such as increased volatility, currency fluctuations and differences in auditing and other financial standards. Securities in emerging markets are volatile and can decline significantly in response to adverse issuer, political, regulatory, market, or economic developments.

An index is a statistical measure of change in an economy or a securities market. In the case of financial markets, an index is an imaginary portfolio of securities representing a particular market or a portion of it. Each index has its own calculation methodology and is usually expressed in terms of a change from a base value. Thus, the percentage change is more important than the actual numeric value. An investment cannot be made directly into an index.

Investing in fixed income securities involves credit and interest rate risk. When interest rates rise, bond prices generally fall. Investing in commodities may involve greater volatility and is not suitable for all investors. Investing in a non-diversified fund that concentrates holdings into fewer securities or industries involves greater risk than investing in a more diversified fund. The equity securities of small companies may not be traded as often as equity securities of large companies so they may be difficult or impossible to sell. Neither diversification nor asset allocation assure a profit or protect against a loss in declining markets. Past performance is not an indicator of future results.

Sean P. Storck and Steven W. Pollock are registered representatives with and securities and Retirement Plan Consulting Program advisory services offered through LPL Financial, a Registered Investment Advisor. Member FINRA/SIPC. Financial Planning offered through Reason Financial, a state Registered Investment Advisor. Investment advice offered through Merit Financial Group, LLC an SEC Registered Investment Advisor. Merit Financial Group and Reason Financial are separate entities from LPL Financial. Tax related services offered through Reason Tax Group. Reason Tax Group is a separate legal entity and not affiliated with LPL Financial. LPL Financial does not offer tax advice or tax related services. Sean P. Storck CA Insurance Lic#OF25995 and Steven W. Pollock CA Insurance Lic#OE98073

Copyright © 2021 Reason Financial all rights reserved.

i Gilchrist, Karen. “British Pound Falls to Its Lowest Level against the Dollar since 1985.” CNBC, CNBC, 8 Sept. 2022, https://www.cnbc.com/2022/09/07/british-pound-falls-to-its-lowest-level-against-the-dollar-since-1985.html.

ii Gordon, Nicholas. “Apple, Honda, Mazda Reportedly Consider Reducing China Manufacturing.” Fortune, Fortune, 25 Aug. 2022, https://fortune.com/2022/08/25/apple-honda-mazda-china-manufacturing-supply-chain-relocation/.

iii “Online Certificates of Deposit (Cds): Marcus by Goldman Sachs®.” Online Certificates of Deposit (CDs) | Marcus by Goldman Sachs®, https://www.marcus.com/us/en/savings/high-yield-cds

iv “San Diego, CA: Realtor.com®.” Realtor.com, Realtor.com, https://www.realtor.com/realestateandhomes-search/San-Diego_CA/overview.

v Davis, Author: Abby. “Interest Rate Hikes Impacting Local Housing Market.” Ktvb.com, 12 Oct. 2022, https://www.ktvb.com/article/news/local/interest-rate-hikes-impacting-ada-countys-housing-market/277-95ff969a-73b0-44bc-afe7-9e49473fc044.

vi “Germany Private Consumption: % of GDP.” CEIC, https://www.ceicdata.com/en/indicator/germany/private-consumption–of-nominal-gdp#:~:text=Germany%20Private%20Consumption%20accounted%20for,an%20average%20share%20of%2055.4%20%25.

vii Zeihan, Peter. “China’s Rise Will Be Short-Lived.” China’s Rise Will Be Short-Lived. Here’s Why. | Barron’s, Barrons, 23 June 2022, https://www.barrons.com/articles/china-xi-jinping-economics-rise-51655929850.

viii Smith, Colby, and Kate Duguid. “Investors Now Expect Fed to Raise Rates to 5% next Year.” Subscribe to Read | Financial Times, Financial Times, 20 Oct. 2022, https://www.ft.com/content/963bc01e-c81a-462c-ac2b-ef838cb8bc39.